/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

Alphabet (GOOG) (GOOGL), one of the foremost names in the tech industry and now a very consequential player in the AI race, will see its shares added to the Dow Jones Industrial Average ($DOWI) on June 29. The parent company of Google will replace telecommunications major Verizon (VZ).

After it seemed that it could do no wrong, Google has suddenly been hit from all sides, with GOOG stock having its worst day in a year. While latent fears around the capex story remained, what triggered the latest fall was the departure of two key AI researchers, Noam Shazeer and John Jumper. Shazeer, who was a co-lead of the Gemini AI models, departed to join fierce rival OpenAI. And Jumper, the creator of the AI system AlphaFold, joined the current market leader, Anthropic.

The so-called brain drain has had mixed results in the cutthroat world of AI, though, recently. Nobody can deny the success story that is Anthropic, which was started by Dario Amodei after leaving OpenAI. Yet, Meta's (META) AI efforts remain pale in comparison to others, even after a $14.2 billion investment in Scale AI.

Reputational Win for Google

But I digress. No matter the size of the company, inclusion in one of the oldest and most reputable indices in the world is certainly a positive for Google. With AI capex showing no signs of slowing down, inclusion in the Dow can have the indirect beneficial effect of low borrowing costs for the company in the future.

However, investors should curb their expectations of an immediate rebound in the company's shares solely based on this development if history is any indication.

After its inclusion in the Nasdaq ($NASX) in December 2005, shares of Google (as it was known then) took more than a year to surpass its levels seen on the day of the inclusion, with shares down more than 16% in the six months following its addition.

When it comes to the S&P 500 ($SPX), the picture gets better, but nothing noteworthy. Google's shares had a drawdown of almost 12% in three months after their inclusion in the S&P 500 in March 2006. However, shares were up 19% in one year.

Thus, Alphabet's place in the DJIA should be looked at just as a symbol of the company's credibility. Basing investment decisions on the same will just be a tactical move, not a structural one.

Financial Powerhouse

Alphabet's growth over the past decade and more bears testimony to its market-leading position in the world of consumer tech, especially through its Google Search Engine, Android operating system, and video-sharing platform, YouTube. This has led to the company's revenue and earnings reporting impressive CAGRs of 18.41% and 25.12%, respectively.

This has led to the parent company, Alphabet, becoming the third-biggest company in the world by market cap at $4.2 trillion. Its shares are up 9% on a year-to-date (YTD) basis.

Moreover, Alphabet's quarterly earnings have been surpassing Street expectations consecutively for more than two years now. Q1 2026 was no different.

Revenues increased by 22% from the previous year to $109.9 billion, with the high-margin cloud business seeing its revenues grow by 63% in the same period to $20 billion. Notably, backlog for the segment more than doubled quarter-over-quarter (QoQ) to exceed $460 billion, the majority of which is projected to accrue in the next two years. The Services segment, which includes Google Search, moved higher by 16% on a year-over-year (YoY) basis to $89.6 billion.

Growth flowed to the bottom line as well. Earnings increased by 82% from the year-ago period to $5.11 per share, handily beating the consensus estimate of $2.68 per share. Moreover, out of the past eight quarters, Alphabet has reported seven quarters of earnings growth exceeding 30% on a YoY basis, which is quite an achievement for a company of this scale.

Meanwhile, the company also increased its quarterly dividend to $0.22 per share, indicating a current dividend yield of 0.25%.

In terms of cash flow, net cash from operating activities for the quarter came in at $45.8 billion, up from $36.2 billion in the prior year. Free cash flow for the quarter was at $10.2 billion, a sequential fall from $24.5 billion in Q4 2025. Free cash flow is important here for Alphabet, considering its mammoth projected capex of $180 to $190 billion this year. Overall, the company closed the quarter with a cash balance of $38.1 billion, with no short-term debt on its books.

However, Alphabet is overvalued, even after its underwhelming performance so far this year. The GOOGL stock is trading at a forward P/E, P/S, and P/CF of 24.34, 8.66, and 20.66, compared to the sector medians of 12.43, 1.19, and 7.50, respectively.

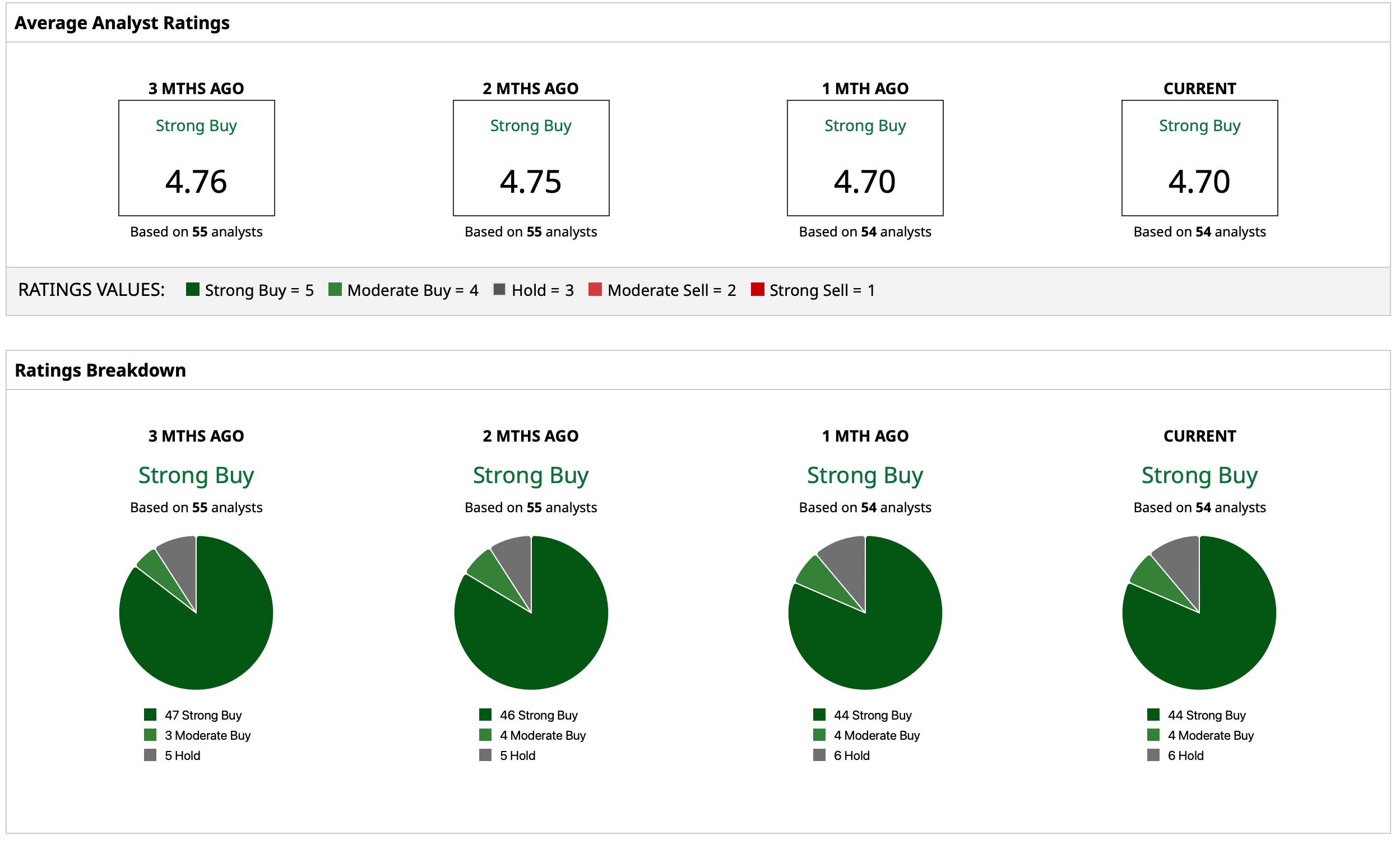

Analyst Opinion of GOOGL Stock

Considering this, analysts have deemed GOOGL stock to be a “Strong Buy,” with a mean target price of $433.63. This indicates an upside potential of about 25.6% from current levels. Out of 54 analysts covering the stock, 44 have a “Strong Buy” rating, four have a “Moderate Buy” rating, and six have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)