/A%20Tesla%20Cybertruck%20with%20visible%20bullet%20impacts_%20Image%20by%20Karolis%20Kavolelis%20via%20Shutterstock_.jpg)

The Islamic Revolutionary Guard Corps, or the IRGC, has a new target. It is not any of the bases or embassies of the U.S. or other friendly countries in the Middle East. Rather, it says that for every assassination of its top personnel, the major branch of the Iranian armed forces will hit the very lifeblood of the American economy: its tech companies.

With a total market cap of about $20 trillion and employing roughly 10 million people, needless to say, any attack on the tech sector will serve as a body blow for the United States. Among the names on the IRGC's hit list is the EV, and now increasingly becoming an AI major, Tesla (TSLA). The list also includes other “Mag 7” counterparts such as Nvidia (NVDA), Microsoft (MSFT), and Alphabet (GOOG) (GOOGL).

However, with the focus on Tesla heightened amid SpaceX's filing its papers for an IPO, how much of a setback can this recent threat be? Let's find out.

Not Much of a Material Impact

In terms of on-the-ground threats, Tesla should not be that worried, as its presence in the Middle East is limited relative to other places such as the U.S., Europe, or China.

Tesla operates a strategic but relatively modest retail and service footprint across the Middle East, with its primary hubs located in the United Arab Emirates, Israel, Jordan, Qatar, and Oman. The United Arab Emirates commands the largest share of the regional automotive electric vehicle market, which was valued at nearly $3.8 billion in 2025 and is projected to surpass $5 billion in 2026. While the company holds a dominant position within this specific geographical niche, the quantum of its direct financial exposure remains minimal. When compared to the massive volumes generated in the United States and China, the Middle Eastern region contributes only a fraction of a percent to the total annual deliveries and overall revenue stream of the automaker.

Moreover, the automaker does not operate any manufacturing plants, assembly lines, or Gigafactories within the Middle East or the broader Gulf region. Its global production capacity is strictly concentrated in regions like California, Texas, Nevada, New York, Shanghai, and Berlin. The physical infrastructure present in the targeted areas is limited entirely to consumer-facing assets, specifically retail showrooms, vehicle service centers, and an extensive network of Superchargers located at prominent destinations such as shopping malls and airports in cities like Dubai and Abu Dhabi. Consequently, the firm does not have billions of dollars tied up in heavy industrial machinery or critical supply chain components vulnerable to physical destruction in these high-risk zones.

Before this geopolitical escalation, industry analysts speculated heavily about the company establishing a dedicated Gigafactory within the Gulf, with Saudi Arabia and the United Arab Emirates emerging as prime candidates eager to diversify their economies away from fossil fuels. The firm also relies on regional data infrastructure to support its sweeping AI and autonomous driving ambitions, including the recently announced $30,000 Cybercab slated for 2026. These ambitious expansion narratives are now effectively stalled, as the direct threats from the IRGC create an untenable risk environment for heavy capital expenditure. While the automaker has not issued a formal press release regarding these specific threats, regional staff are presumably operating under the same remote work directives adopted by other targeted tech giants to ensure personnel safety.

Financials Still Decent Enough

Tesla has delivered impressive growth over the past five years, with revenue and earnings compounding at annual rates of 24.63% and 34.93%, respectively. However, repeating that level of performance in the near term appears increasingly difficult, as the latest quarterly results illustrate, as the stock is down 19% on a year-to-date (YTD) basis.

In Q4 2025, Tesla beat both revenue and earnings estimates, but the overall picture remained soft. Total revenue declined 3% year-over-year (YoY) to $24.9 billion, with automotive revenue falling 11% to $17.7 billion. Earnings per share dropped 17% to $0.50, although it still edged past the $0.45 consensus. This marked the fourth consecutive quarter of YoY EPS decline. Over the past nine quarters, the company has beaten earnings estimates only three times.

Margins also compressed to 5.7% from 6.2% a year earlier. Operating cash flow fell 21% to $3.8 billion. Tesla ended the quarter with $44.1 billion in cash, ahead of short-term debt of $31.7 billion.

Both production and deliveries declined after a temporary boost from the expiration of federal EV tax credits. Production totaled 434,358 vehicles, down 5% YoY, while deliveries dropped 16% to 418,227 units.

On a more positive note, active Full Self-Driving (FSD) subscriptions grew 38% YoY to 1.1 million. The energy business continued to show solid momentum, with revenue rising 27% to $12.8 billion. Supercharger stations increased 17% to 8,182, and connectors grew 19% to 77,682.

Valuation remains elevated compared with most large-cap peers. The forward P/E stands at 178.70 versus a sector median of 14.65, while forward P/S of 13.50 and P/CF of 85.54 sit well above sector medians of 0.87 and 9.59.

Analyst Opinion on TSLA Stock

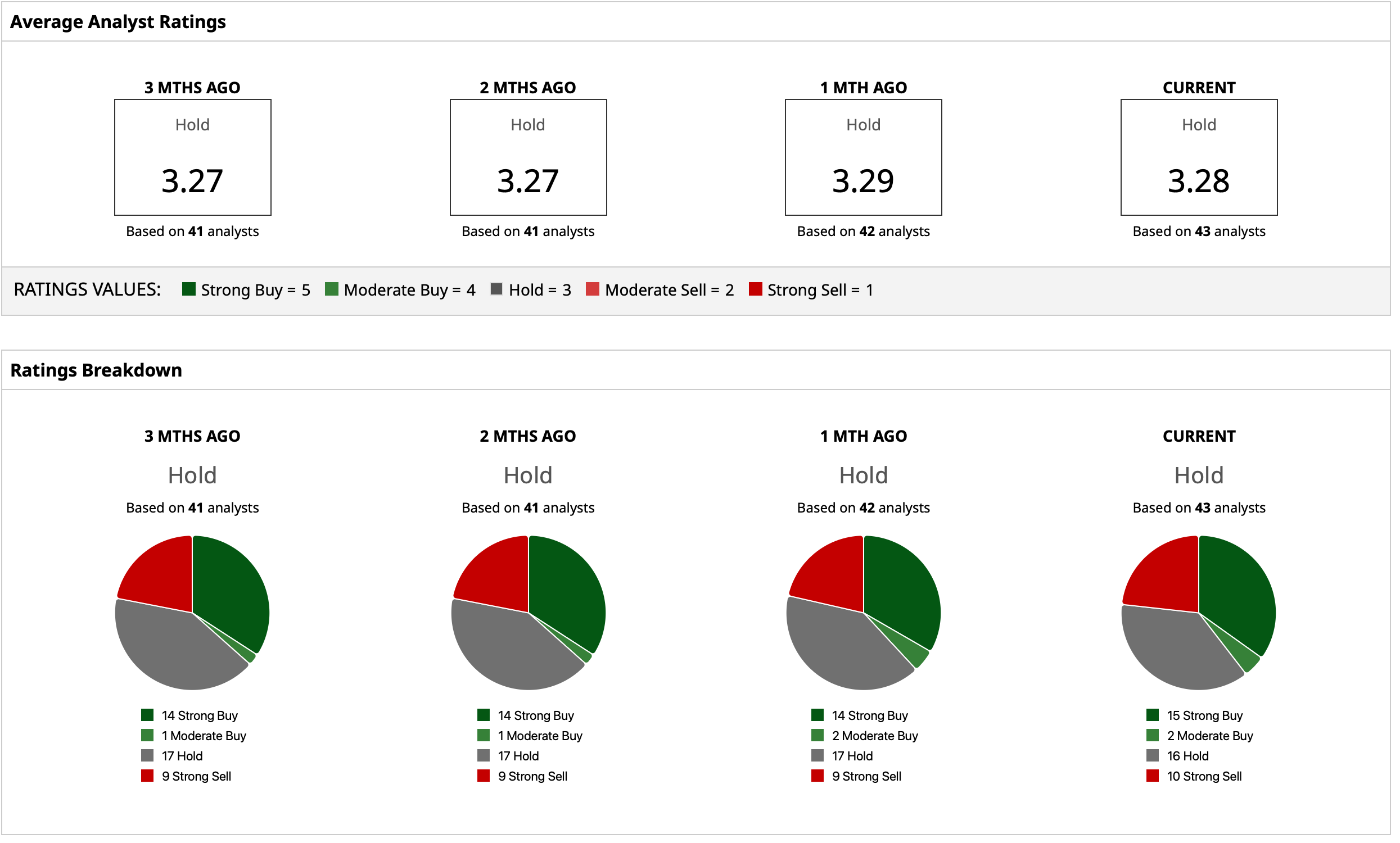

Overall, analysts have attributed a rating of “Hold” for TSLA stock, with a mean target price of $405.64. This denotes an upside potential of about 10% from current levels. Out of 43 analysts covering the stock, 15 have a “Strong Buy” rating, two have a “Moderate Buy” rating, 16 have a “Hold” rating, and 10 have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)