/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)

The emergence of Netflix's (NFLX) streaming platform in 2007 revolutionized the entertainment industry. Over the years and amidst growing competition, Netflix has created value for shareholders. If there has to be a moat that’s worth calling out, it’s Netflix’s superior content.

Leveraging on that moat, Netflix recently announced that the company will be raising its subscription prices. This is because the company plans to increase its content budget to $20 billion.

It’s worth noting that Netflix last raised its subscription fee in January 2025. Further, the current hike is a $1 raise for the standard plan with ads to $8.99 per month, a $2 raise for the standard plan with no ads to $19.99 per month, and a $2 raise for the premium plan to $26.99 per month. With that in mind, these price hikes are unlikely to have an impact on the number of subscribers. At the same time, continued content-pull is likely to remain the growth factor.

About Netflix Stock

Headquartered in Los Gatos, California, Netflix is a leading entertainment services company offering TV series, films, games and live programming. The company’s services offering is across a variety of genres and languages, which has translated into a significant market globally. As of Q4 2025, Netflix had 325 million paid memberships.

In December 2025, Netflix announced the acquisition of Warner Bros. from Warner Bros. Discovery (WBD) in a cash and stock transaction valued at $27.75 per WBD share. This implied a total enterprise value of approximately $82.7 billion.

However, Paramount Skydance (PSKY) put forward a "Superior Proposal" to acquire Warner Bros. in February 2026. Netflix declined to raise its offer. Citi recently reinitiated coverage on Netflix with a “Buy” rating and believes that walking away from the deal is a positive for the company.

Despite multiple positives, NFLX stock has corrected by 23% in the last six months. With the recent announcement of subscription rate hikes, shares will likely trend higher from oversold levels.

Strong Fundamentals Support Growth

Importantly, Netflix ended fiscal 2025 with a cash buffer of $9 billion, while operating cash flow for the period was $10.1 billion. In fiscal 2023, Netflix reported an operating margin of 20.6%, which swelled to 29.5% in fiscal 2025. For the current year, Netflix is guiding for an operating margin of 31.5%, which is in-line with the recent increase in subscription rates. It’s therefore likely that cash flows will increase in fiscal 2026 and provide the company with ample flexibility to invest in new content creation.

Netflix also mentioned in its letter to shareholders that there is “plenty of room to increase” margins and that the company intends to expand its operating margin each year. Management seems to be aiming for continued upside in cash flows.

From a geographical diversification perspective, Netflix reported that 76% of revenue in fiscal 2025 came from the United States, Canada, and Europe, the Middle East and Africa (EMEA). Therefore, Latin America (LATAM) and Asia-Pacific (APAC) are still a small part of the company's total revenue. These emerging markets have the potential to be key growth and margin drivers in the long term.

What Do Analysts Say About NFLX Stock?

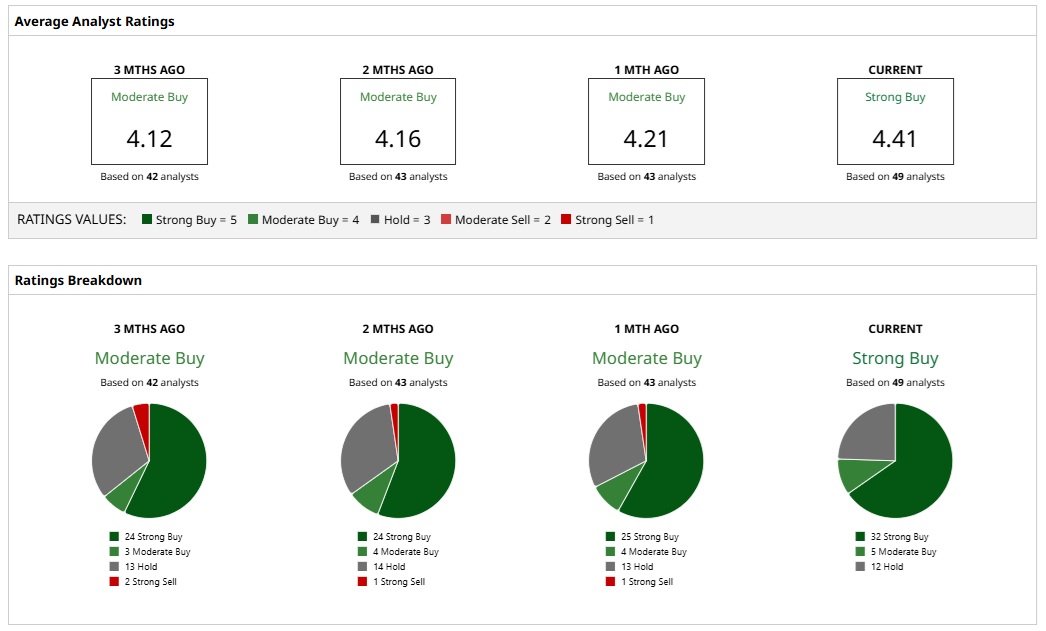

Based on 49 analysts with coverage, NFLX stock has a consensus “Strong Buy" rating. While 32 analysts have a “Strong Buy” rating for Netflix, five analysts have a “Moderate Buy” rating, and 12 analysts have a “Hold” rating. The mean price target of $114.63 represents potential upside of about 23% from current levels, while the most bullish price target of $137 suggests that NFLX could climb 47% from here.

Oppenheimer maintained a bullish view on Netflix even after the subscription price hike. The analyst firm believes Netflix will keep dominating streaming with high-engagement content being the differentiator. Currently, Oppenheimer has a price target of $135 for NFLX stock.

Analysts also expect healthy earnings growth for Netflix. For fiscal 2026 and fiscal 2027, earnings growth is anticipated to be 24% and 23%, respectively.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)