With a market cap of $80.8 billion, Freeport-McMoRan Inc. (FCX) is an Arizona-based mining and metals company. Freeport’s core business is exploration, mining, and production of mineral resources, with a strategic emphasis on copper, a critical industrial metal used in electrical infrastructure, renewable energy, and electrification. The company is expected to announce its fiscal first-quarter earnings soon.

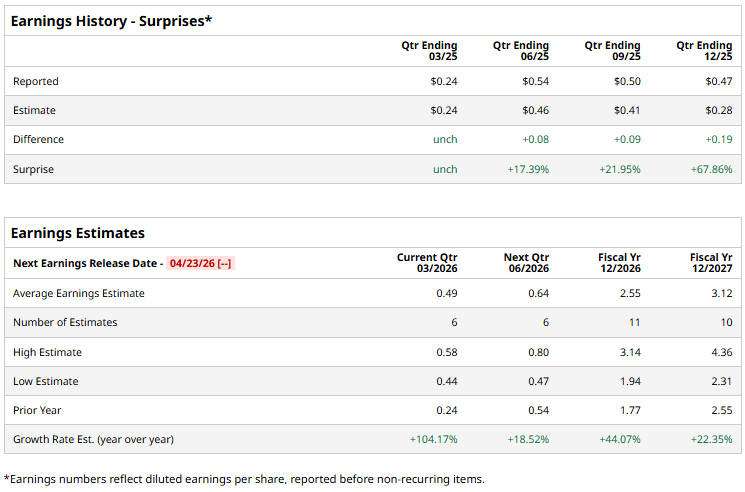

Ahead of the event, analysts expect the metal giant to report a profit of $0.49 per share on a diluted basis, up 104.2% from $0.24 per share in the year-ago quarter. The company beat or met consensus estimates in all four quarters over the past year.

For the current year, analysts expect FCX to report EPS of $2.55, up 44.1% from $1.77 in fiscal 2025. Its EPS is expected to rise 22.4% year over year to $3.12 in fiscal 2027.

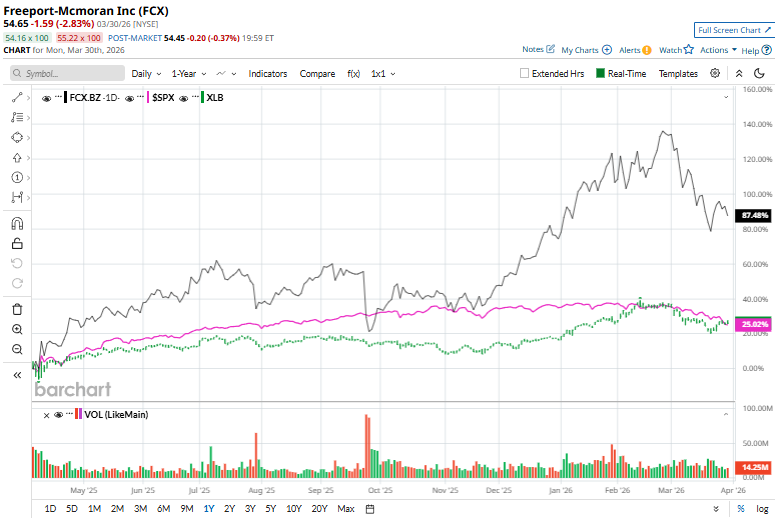

FCX stock has climbed 42.2% over the past year, outpacing the S&P 500 Index’s ($SPX) 13.7% gains and the Materials Select Sector SPDR Fund’s (XLB) 15.4% rally over the same time frame.

Freeport-McMoRan declined over 2% on Mar. 26 as mining stocks broadly weakened, pressured by a sharp drop in precious metal prices, particularly gold and silver.

Analysts’ consensus opinion on FCX stock is highly bullish, with a “Strong Buy” rating overall. Out of 21 analysts covering the stock, 15 advise a “Strong Buy” rating, three suggest a “Moderate Buy,” and three give a “Hold.” FCX’s average analyst price target is $67.95, indicating a 24.3% potential upside from the current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Delta%20Air%20Lines%2C%20Inc_%20passanger%20plane-by%20viper-zero%20via%20iStock.jpg)