Alcoholic beverage giant Brown-Forman Corporation (BF.B) (BF.A), the company behind the iconic Jack Daniel's, is finding itself at a crossroads. Once seen as a steady, defensive blue-chip, the stock has come under pressure over the past year as a perfect storm of tariff headwinds, strategic recalibration, and a cooling global spirits market weighs on performance. More notably, a generational shift in consumption is emerging, with Gen Z showing less interest in alcohol, adding a longer-term challenge that has kept shares on the back foot.

Nevertheless, sentiment has recently turned more optimistic. On March 26, Brown-Forman revealed it is exploring a potential “merger of equals” with Pernod Ricard (PRNDY), a move aimed at creating a global spirits leader with greater scale, a more powerful brand portfolio, and a well-balanced geographic presence. However, the company also made it clear that a deal is not guaranteed. RBC Capital analyst Nik Modi noted that, from a strategic standpoint, the combination makes sense.

Pernod Ricard brings a highly diversified portfolio spanning whiskey, vodka, gin, rum, liqueurs, agave spirits, and champagne, while Brown-Forman is more concentrated in American whiskey, tequila, and ready-to-drink offerings. According to Modi, the potential for operational synergies could unlock meaningful value. Still, the risks are hard to ignore. Both companies are already facing headwinds, and executing a merger of this scale could prove complicated.

Differences in regional and corporate cultures, mismatched capabilities, and strong family ownership on both sides may create significant integration challenges. As Modi cautioned, large M&A deals often fall short of expectations, and this one may be no exception. So, with both the upside potential and execution risks firmly in play, should investors buy, sell, or hold Brown-Forman stock right now?

About Brown-Forman Stock

Brown-Forman Corporation is a long-established player in the global spirits industry, with a history spanning more than 155 years. Headquartered in Louisville, Kentucky, it has built a portfolio of beverage alcohol brands over time, guided by its long-standing principle, “Nothing Better in the Market.” Its lineup includes the Jack Daniel's family of brands, Woodford Reserve, Old Forester, New Mix, el Jimador, Herradura, The Glendronach, Glenglassaugh, Benriach, Diplomático Rum, Gin Mare, Fords Gin, Chambord, and Slane.

Today, with approximately 5,000 employees worldwide, Brown-Forman distributes its products in more than 170 countries, reflecting the scale and longevity of a business that has steadily expanded while remaining anchored to its original guiding principle. With a market capitalization of roughly $12.5 billion, Brown-Forman has been on a steep downward path, as its shares have plunged about 21% over the past year but up 4.32% so far in 2026.

The prolonged slump underscores the mounting pressures facing the company, from industry-wide softness to internal challenges that have kept investors cautious. Yet, sentiment has taken a sharp turn in recent sessions. Renewed optimism, fueled by merger discussions with Pernod Ricard, has sparked a powerful rebound in the stock. Over just the past five trading days, shares have surged approximately 18.56%, a striking move that stands in stark contrast to the broader S&P 500 Index ($SPX), which slipped 3% over the same period.

Like many established blue-chip names, Brown-Forman has built a long track record of returning capital to shareholders through dividends. The company is a member of the prestigious Dividend Aristocrats, having paid regular quarterly dividends for an impressive 82 years while increasing its payout for 42 consecutive years.

Most recently, in February, the company declared a quarterly dividend of $0.2310 per share on both its Class A and Class B common stock, scheduled to be paid on April 1. On an annualized basis, that translates to $0.92 per share, offering an enticing yield of about 3.37%, a steady income stream that continues to appeal to long-term investors even amid recent volatility.

Inside Brown-Forman’s Latest Financial Performance

Brown-Forman delivered its fiscal 2026 third-quarter results in early March, alongside its year-to-date (YTD) performance for the nine months ended Jan. 31, 2026, and the numbers painted a mixed, somewhat uneven picture. Quarterly net sales inched up 2% to about $1.1 billion, while organic net sales rose a modest 1%, just enough to edge past Wall Street’s $1 billion estimate.

On the bottom line, earnings came in at $0.58 per share, up 1% year-over-year (YOY) and comfortably ahead of the consensus estimate of $0.47. However, the YTD performance tells a more cautious story. For the nine-month period, reported net sales declined 2% to $3 billion, reflecting the broader pressures the company has been navigating through 2025 and into 2026. Under the surface, brand performance was notably uneven.

The whiskey portfolio showed resilience, with reported net sales rising 2%, supported by innovation, particularly the launch of the Jack Daniel’s Tennessee Blackberry. In contrast, the tequila segment struggled, as Herradura’s net sales dropped 11% amid intensifying competition. One of the standout bright spots was the Ready-to-Drink (RTD) segment, where net sales climbed 8%. This growth was largely driven by strong momentum in Mexico, with New Mix delivering an impressive 37% surge in reported net sales, underscoring shifting consumer preferences toward convenience-oriented offerings.

On the cash flow front, the liquor maker showed solid improvement. Cash flow from operations increased by $263 million to $709 million, supported by disciplined working capital management, while free cash flow rose $299 million to $628 million, reflecting both strong operating performance and lower capital expenditure requirements. Looking ahead, management struck a cautious tone.

The company expects the operating environment in fiscal 2026 to remain challenging, citing limited visibility due to ongoing macroeconomic and geopolitical volatility. Headwinds from consumer uncertainty and softer non-branded used barrel sales are also expected to weigh on results. As a result, Brown-Forman reiterated its outlook, projecting organic net sales and organic operating income to decline in the low-single-digit range, with capital expenditures planned between $110 million and $120 million.

How Are Analysts Viewing Brown-Forman Stock?

Like RBC Capital Markets, Wall Street is far from unified on Brown-Forman’s potential merger with Pernod Ricard, and the sentiment is clearly split. Analysts at TD Cowen, led by Robert Moskow, point out that the Brown family’s roughly 67% voting control and its historical resistance to takeovers make a deal far from certain. However, the investment firm acknowledges that the current backdrop of weak industry growth and an uncertain recovery timeline could make the family more open than in the past.

On the more optimistic side, Jefferies analyst Edward Mundy sees compelling strategic logic behind a tie-up between the Kentucky-based Brown-Forman Corporation and Pernod Ricard. He argues that with the spirits industry currently in a lull, a merger could unlock cost savings that can be reinvested to reignite growth while also delivering greater scale.

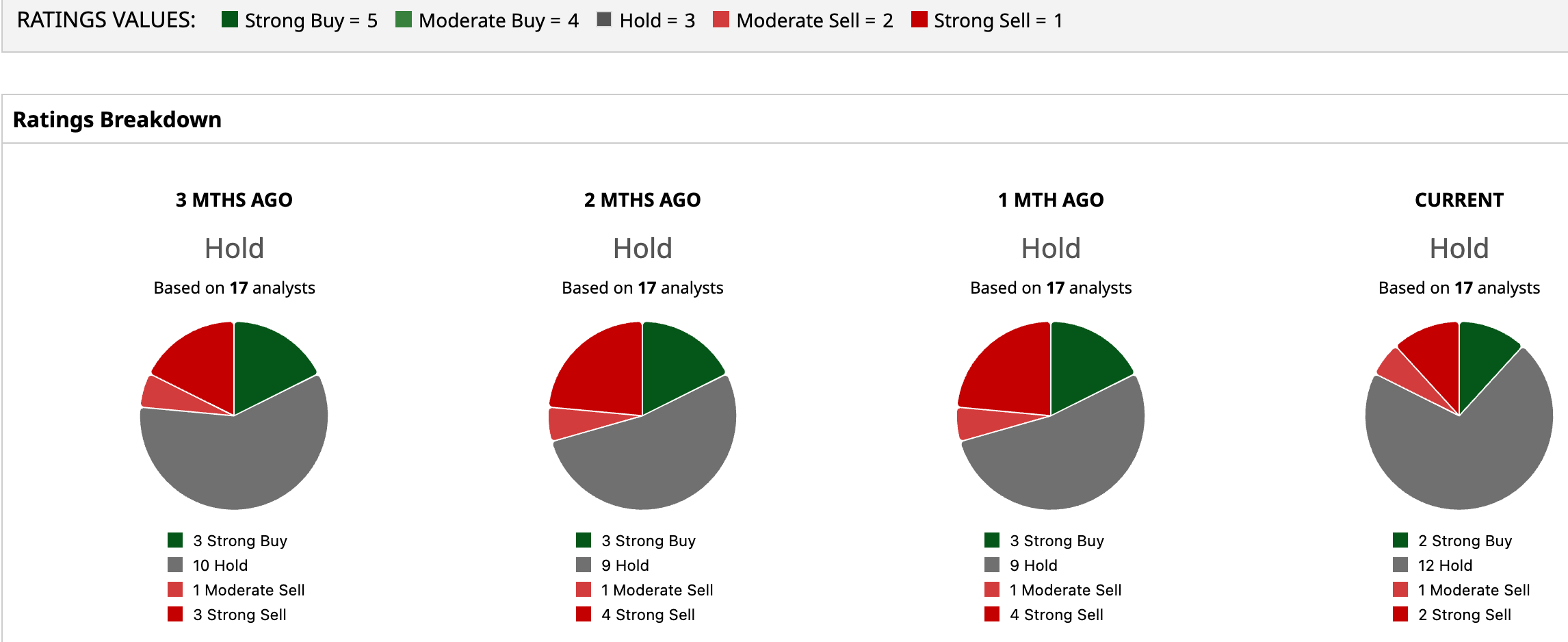

Further, Mundy highlighted potential strategic and commercial synergies, adding that culturally, both companies could align well, particularly if the structure allows the Brown family to retain control. Even so, despite pockets of optimism, Wall Street’s overall stance leans toward a cautious “Hold.” Among the 17 analysts covering the stock, only two rate it a “Strong Buy,” while 12 recommend “Hold,” one suggests a “Moderate Sell,” and two have issued “Strong Sell” ratings.

The stock is currently trading slightly below the average price target of $28.23, while the Street-high target of $35 implies a potential upside of about 29% from current levels. In short, while merger speculation has injected fresh optimism into the story, analysts remain largely on the sidelines, waiting for clearer signals before turning decisively bullish.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)