/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

Behind every powerful artificial intelligence (AI) model sits memory. It is what allows systems to recall context, process queries, and deliver responses in real time. But the more advanced AI becomes, the heavier its memory demands get. That means higher costs, bigger infrastructure, and more strain on hardware. So, when someone finds a way to cut that dependency, it doesn’t just improve efficiency, but also changes the equation.

That shift is starting to take shape with Google’s latest move. The company unveiled TurboQuant, a compression algorithm that reduces the memory AI systems actually need. It compresses key-value cache down to just three bits, and early results show it can shrink memory usage dramatically – up to 6x – while keeping performance intact. In effect, AI models could soon run with far less reliance on large memory pools.

That’s where things get uncomfortable for memory players. If the future needs less memory, growth assumptions take a hit. Consequently, stocks tied to memory demand, including Sandisk Corporation (SNDK), saw pressure just yesterday, with SNDK slipping 11%. Sandisk, specializing in NAND flash-based storage solutions designed for AI workloads across data centers, edge environments, and consumer devices, now finds itself at the center of this shift.

SNDK stock has already had a strong run this year, which makes it more exposed to shifts like this. So, does this new development slow the momentum, and is it time for investors to rethink holding the memory stock?

About Sandisk Stock

Milpitas, California-based Sandisk has become one of the key players powering today’s data-driven world. The company focuses on designing and manufacturing NAND flash memory solutions, everything from SSDs and memory cards to embedded storage used across consumer devices, enterprises, and large-scale data centers. With a market cap of $89 billion, Sandisk sits right at the heart of modern digital infrastructure.

A strong industry tailwind is working in its favor. As AI, cloud computing, and big data continue to scale rapidly, the need for faster, more efficient storage has surged. Hyperscalers, in particular, rely heavily on high-performance memory to handle massive workloads, placing Sandisk in a sweet spot.

The company’s spin-off from Western Digital (WDC) last year marked a turning point, giving it more room to focus and unlock value. Since then, tighter NAND supply and rising prices have further strengthened its position.

Sandisk’s vertically integrated model, from wafer fabrication to final SSD assembly, adds an edge in efficiency and innovation. With advancements in TLC and QLC NAND and increased R&D post-spin-off, the company is positioning itself for the next phase of enterprise storage growth.

SNDK stock has been on a wild ride ever since its spinoff, turning into one of the market’s biggest momentum stories. The numbers say it all. SNDK has skyrocketed 1,072% since the separation, leaving the broader benchmarks like the S&P 500 Index ($SPX) far behind and forcing analysts to keep raising their expectations.

The momentum did not slow this year either. After a strong close to 2025, the stock is up 161% in 2026, fueled by tightening supply, rising 3D NAND prices, and solid confidence that AI-driven demand is here to stay. It reflects how aggressively investors have been leaning into the AI storage theme. On March 20, the stock touched a high of $777.60.

But the story has not been one-way. Since that high, the stock has dropped about 20.5%, and the reasons are stacking up. A key trigger was the expiry of a lock-up period, which released over two million insider and Western Digital shares into the market, raising fears of heavy selling pressure. Meanwhile, broader market weakness, driven by geopolitical tensions and rising energy costs, has pushed investors toward profit booking.

The pressure has not eased. A controversial $1 billion investment in Nanya Technology has raised concerns about strategy and capital discipline, while Google’s TurboQuant announcement has added fresh uncertainty around future memory demand.

From a technical standpoint, Sandisk still looks strong, even after the recent pullback. And the broader trend has not broken. If anything, it is cooling off after a sharp run rather than reversing. The 14-day RSI has eased to 47.33, stepping out of overbought territory and giving the stock some breathing room.

Meanwhile, the MACD oscillator is still flashing strength. The MACD line is holding above the signal line and pushing higher, while the histogram stays firmly positive, clearly signaling that bullish momentum has not faded and buyers still have control.

Sandisk’s valuation feels like a split narrative. On the one hand, it looks expensive, priced at 5.71 times forward sales, above the sector. But flip the lens, and the forward price/non-GAAP EPS ratio of 29 times comes in lower than peers. That contrast tells that the market is pricing in strong growth today, but earnings expansion ahead could quietly justify, or even improve, the current valuation over time.

A Closer Look at SanDisk’s Q2 Earnings Report

SanDisk delivered a standout second-quarter fiscal 2026 performance on Jan. 29, beating projections. The company reported revenue of $3.03 billion, up 61% year-over-year (YOY) and 31% sequentially, comfortably beating the company’s guidance and consensus estimates. The growth story was broad-based, driven by strength across data center, edge, and consumer segments.

Segment-wise, data center revenue reached $440 million, up 76% annually, reflecting solid traction in enterprise storage demand. The edge segment contributed roughly $1.7 billion, growing 63% YOY, while consumer revenue of about $907 million climbed 52%, showing balanced demand across end markets.

Profitability saw an equally sharp improvement. Non-GAAP EPS came in at $6.20, a significant jump from $1.23 in the prior year and well ahead of expectations. Gross margins expanded to 51.1%, marking an increase of about 18.6 percentage points year over year, supported by better pricing and a richer product mix tilted toward higher-value SSD solutions.

Financially, the balance sheet also strengthened. As of Jan. 2, cash and equivalents stood at $1.54 billion, while long-term debt was reduced to $583 million. Free cash flow turned robust, with adjusted free cash flow of $843 million versus $91 million a year earlier and $448 million in the prior quarter.

Looking ahead, management guided Q3 fiscal 2026 revenue between $4.4 billion and $4.8 billion, with non-GAAP EPS expected in the $12 to $14 range, signaling continued acceleration in both growth and profitability if the trajectory holds.

Analysts monitoring Sandisk remain upbeat, forecasting EPS of $32.76 for fiscal 2026, a significant 1,741% YOY jump, followed by a further 125.5% annual rise to $73.86 in fiscal 2027.

What Do Analysts Expect for Sandisk Stock?

Sandisk continues to draw a positive stance from BofA Securities, which reiterates a “Buy” rating with a $900 price target. The outlook is supported by strong demand from hyperscalers and growing AI inference workloads. BofA also factors in SanDisk’s focus on supply discipline, limited capacity expansion, and a strategic shift toward higher-margin cloud and eSSD products. Meanwhile, BofA Securities anticipates earnings strength ahead, projecting significant EPS growth into fiscal 2026, while valuation is anchored to future earnings potential and improving market share in the eSSD segment.

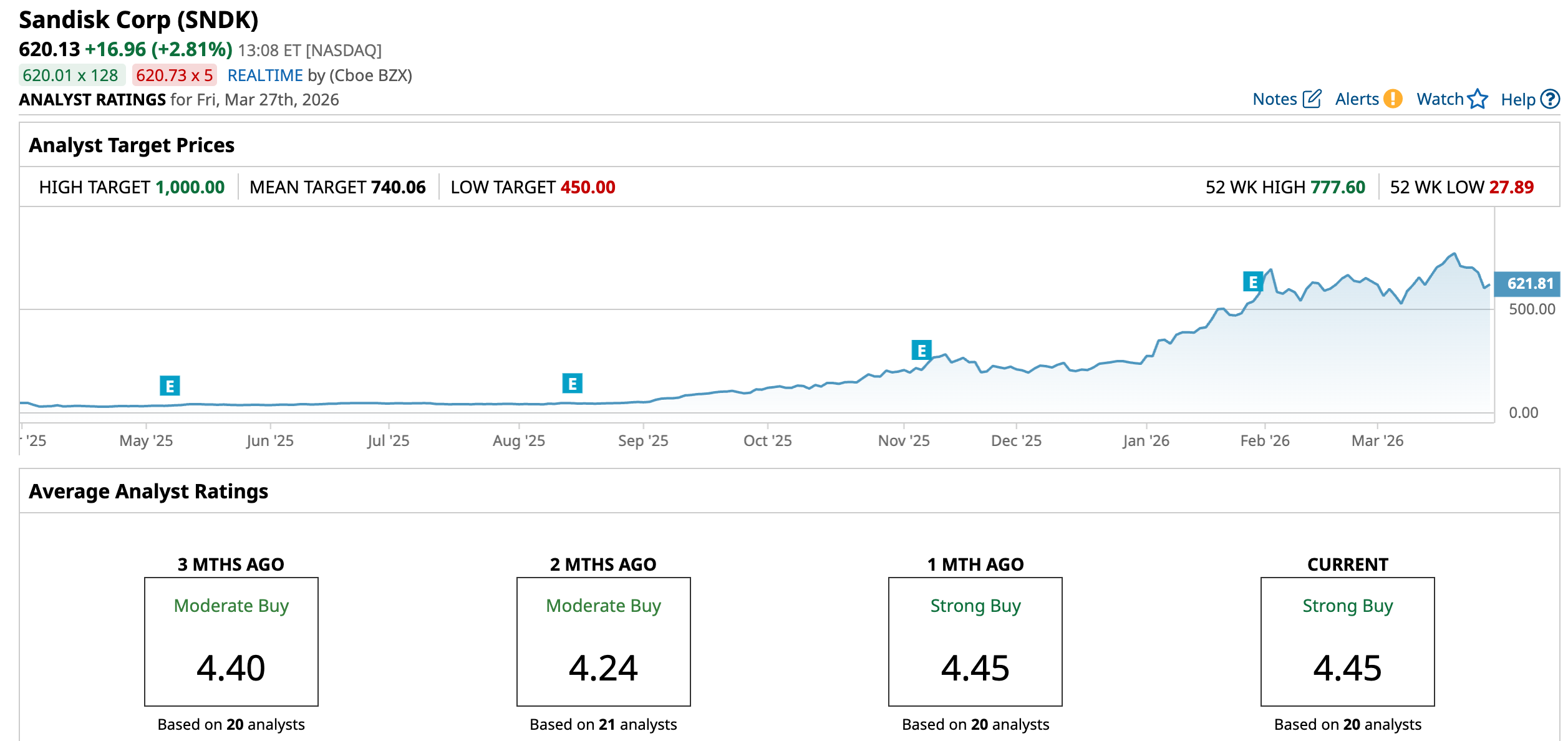

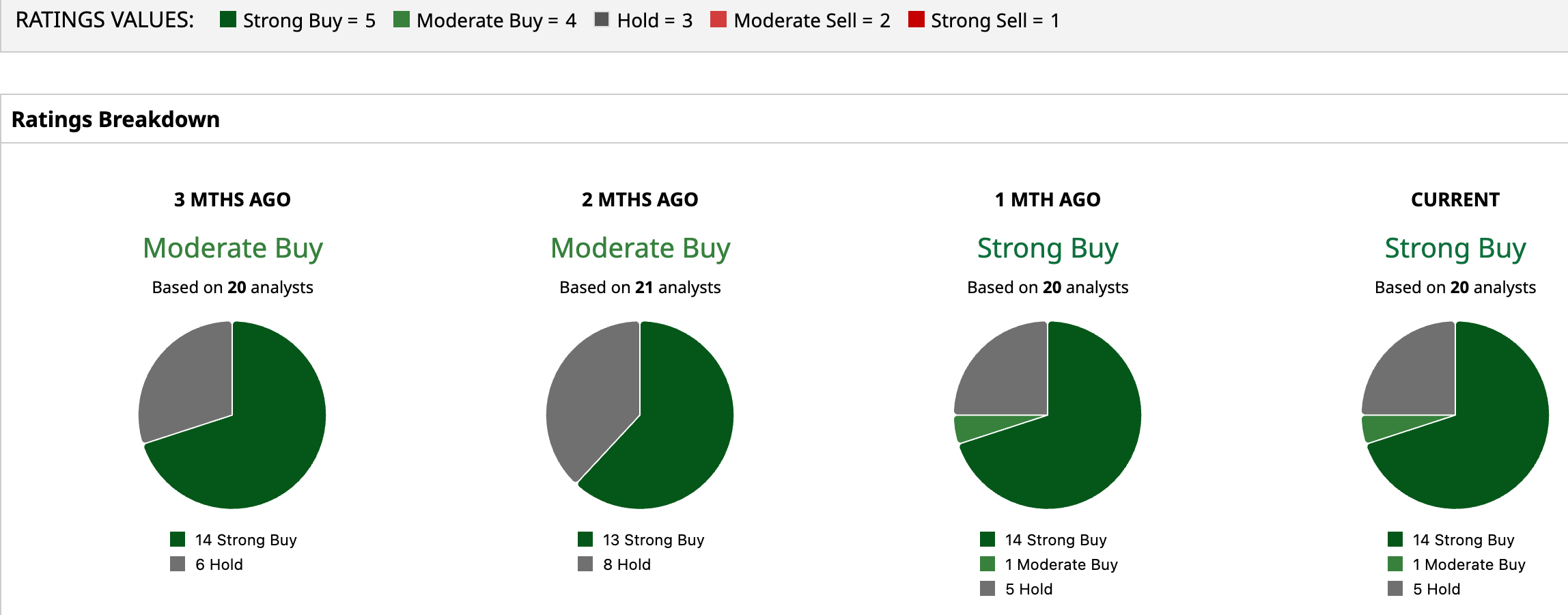

Overall, SNDK has a consensus “Moderate Buy” rating. Of the 20 analysts covering the stock, 14 advise a “Strong Buy,” one suggests a “Moderate Buy,” and the remaining five analysts are on the sidelines, giving it a “Hold” rating.

SNDK’s average analyst price target of $740.06 indicates an upside of around 19.3%, while Bernstein SocGen’s Street-high target price of $1,000 suggests that the stock could rally as much as 61.3%.

Final Thoughts on SNDK Stock

So, should investors sell SNDK at this point? It is not a straightforward answer. On one side, TurboQuant does raise concerns – if AI systems start needing less memory, it could pressure long-term demand assumptions. Pairing that with SNDK’s massive run, the stock naturally becomes more sensitive to any negative shift.

At the same time, the broader story has not cracked. AI demand is still strong, earnings are ramping up, and analysts remain bullish on the outlook. This feels more like a breather.

For investors, it is not an outright “sell” signal, but probably more a moment to stay selective, maybe book partial gains, and keep a close eye on how the AI memory demand story plays out.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)