/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

Palantir Technologies (PLTR) is once again in the spotlight, and this time, it's not because of another great quarter. This time, the driver is structural in nature, as the U.S. Department of Defense has formally designated Palantir's Maven Smart System as a “program of record,” which in essence locks in the long-term use of Palantir's software within the U.S. military.

According to a DoD insider, Palantir will help the U.S. “dominate adversaries in all domains.”

If we take a step back, this also relates to a larger macro theme that investors have been keenly observing over the past year or so. Artificial intelligence, as a whole, is no longer just about productivity in the business world or even the excitement surrounding chatbots. Now, it's about becoming a core component of a nation's infrastructure, defense, and even real-time decision-making tools. As a result, Palantir Technologies isn't just another software firm; in fact, it's becoming a core component of a nation's infrastructure, and that's undoubtedly why the market is increasingly pricing in this factor.

About Palantir Stock

Palantir Technologies is a leading data analytics and artificial intelligence software firm based in Miami, Florida, with a market capitalization of approximately $350 billion. The firm primarily focuses on the intersection of government, defense, and artificial intelligence software.

If we consider the firm's performance from a price perspective, the firm's performance has undoubtedly been robust, as the firm's stock price has increased by over 110% from its 52-week low, though it is still 30% off its peak. In relative terms, Palantir's performance over the past year or so has significantly outperformed the S&P 500 ($SPX), which can be attributed to a combination of improving business fundamentals and a significant re-rating due to the excitement surrounding artificial intelligence.

However, valuation is where things get interesting. A forward price-earnings ratio for the company stands at 158x, and a price-sales ratio stands at 86x. While the high valuation is a point of concern for investors, the margins and capital efficiency of the company are extremely high. This may justify the high valuation to a certain extent.

Nevertheless, the market is factoring in perfect execution for the company.

Palantir Beats on Earnings

The recent earnings announcement by the company further cements the fact that the company’s stock is one worth paying attention to. In Q4 2025, the company announced revenue of $1.407 billion, a 70% year-over-year (YoY) increase. Moreover, the company’s earnings per share came in at $0.24 on a GAAP basis, beating analyst estimates. More importantly, the company did not compromise on profitability for growth, and operating margin came in at 41% on a GAAP basis. Moreover, the company’s free cash flow margins came in above 50%.

Moving forward, the company expects 61% revenue growth in 2026. This is a high growth rate for a company of this size. Moreover, the U.S. commercial revenue increased by 137% YoY. This further cements the fact that the company is no longer just a government contractor. Rather, the company is now a dual-engine business: defense and the other side being the increasing adoption of AI in the enterprise segment.

However, the key point to take away from the recent earnings announcement is the fact that the company closed $4.26 billion in total contract value for the quarter. This is a 138% YoY increase. This further cements the fact that the future revenue streams for the company are now more predictable.

But there is also a subtle but important shift taking place. Palantir is moving from a software business model to an outcomes business model. The reason is their ontology-based approach, which is enabling businesses to operationalize AI across their workflow, not just analyze their data. That is a different business model, and it could also enable better margins.

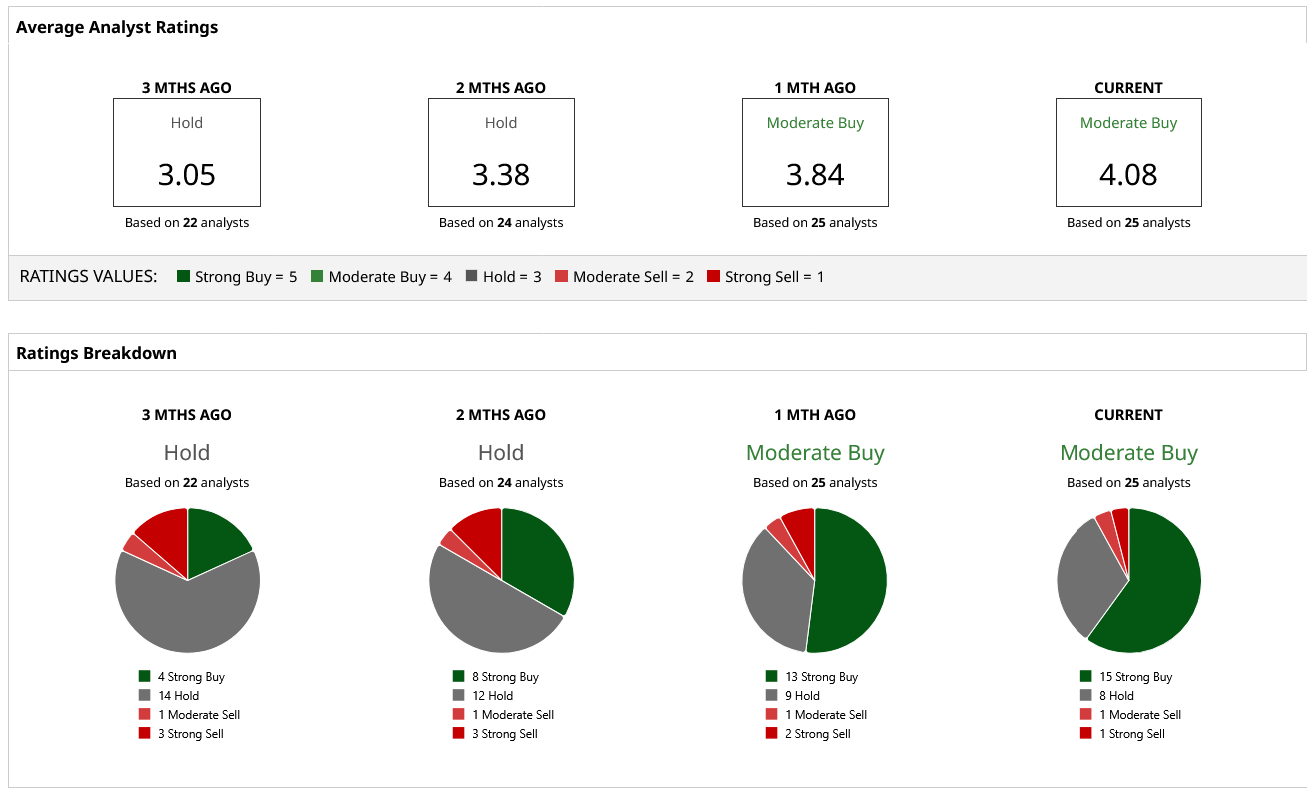

What Do Analysts Expect for PLTR Stock?

Analysts on Wall Street are still constructive but not blindly bullish, with a “Moderate Buy” rating consensus. The range of price targets varies from $90 at the low end to $260 at the high end, while the mean is $201.32. Based on the current stock price of about $145, its mean price target of $201.32 implies a potential gain of approximately 39%.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)