/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)

The semiconductor sector has been scorching hot, driven by AI demand and an ongoing chip shortage. Giants like Nvidia (NVDA) and AMD (AMD) have rallied, lifting chip stocks through 2025. Broadcom (AVGO), a diversified silicon powerhouse, also rode this wave. But just as the bulls roared, insiders at Broadcom began selling shares. Last week, the company’s CFO and several executives dumped tens of millions of dollars of AVGO stock. That development has rattled investors.

Let's review what’s going on with Broadcom's stock and fundamentals, and ask whether these insider sales signal trouble or just routine tax moves.

Broadcom's AI Strategy Drives Long-Term Growth

Broadcom is a $1.5 trillion semiconductor and software company that designs chips for wireless, networking, storage, and broadband, and also owns infrastructure software businesses. CEO Hock Tan has aggressively expanded Broadcom through acquisitions, such as VMware in 2022, and has focused the business on high-margin AI and data-center products. The company pays a growing dividend and has nearly tripled its earnings over the past few years.

Broadcom continues to roll out new products and strengthen its technology portfolio. It announced volume shipments of its Tomahawk 6 Ethernet switch chip, doubling throughput versus its last generation. It also started sampling a new 3-nanometer (3nm) digital-signal processor (BCM83640) for next-gen optical networking.

On the mergers and acquisitions front, no big deals have been announced yet, but management hinted at continued interest in “bolt-ons” to grow its software segment. The big story remains AI. Broadcom claims it can hit $100 billion in AI chip sales by 2027. If CEO Hock Tan is right, Broadcom could keep growing far beyond Wall Street’s current projections.

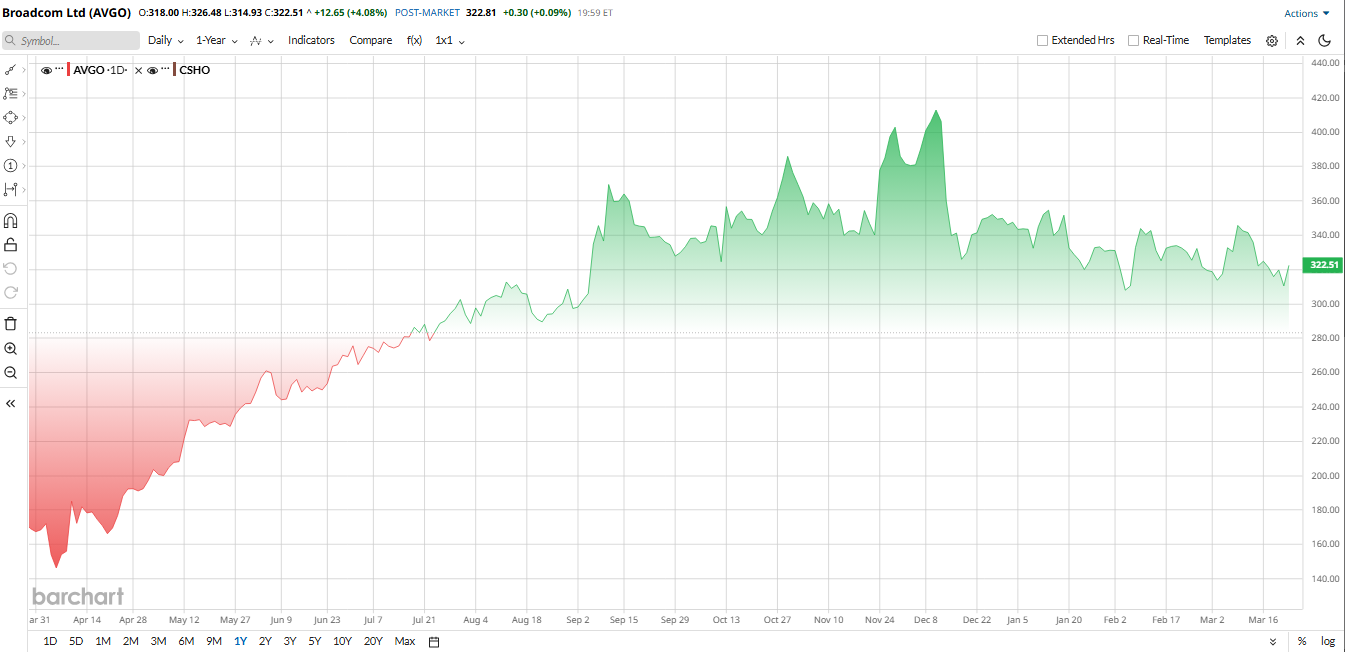

AVGO stock has had a wild ride, surging higher on booming sales and AI hype. In 2025, the stock's total return was more than 50%, making it one of the market’s top performers. However, 2026 has been choppier, with AVGO stock down roughly 8% year-to-date (YTD). The pullback came with broader tech profit-taking, interest rate worries, and now the insider selling headlines.

From a valuation standpoint, Broadcom doesn’t scream “cheap.” Its forward price-to-earnings (P/E) ratio sits around 33.6 times, a premium to the semiconductor sector median of about 21 times. However, the PEG ratio of 0.69 suggests that investors are paying a fair price for its growth profile.

Insider Selling News

On March 16 and March 17, Broadcom insiders sold a flurry of stock. CFO Kirsten Spears automatically sold 60,461 shares worth $19.4 million to cover RSU tax withholdings. Legal and business unit executives also sold stock, with total insider sales of $88 million. The news hit as AVGO stock was already slipping. Traders briefly panicked that the management team might be seeing weaker orders ahead.

In reality, Broadcom said these were routine tax-related sales, not a lack of confidence. Still, the market often overreacts. After the filings appeared, AVGO dipped about 1% to 2% before recovering. Investors are now watching closely to see if execution stays strong or if the sales presage any change in strategy.

Broadcom's Financials

Last month, Broadcom delivered another beat-and-raise quarter. In the first quarter of 2026, revenue reached $19.3 billion, up 29% year-over-year (YOY). The growth was largely driven by AI-related products. Net income came in at $7.34 billion, while adjusted EPS was $2.05, up 28% from a year earlier. Gross margin and operating margins were strong, as was free cash flow at approximately $8 billion.

CEO Hock Tan noted that AI revenue rose 106% YOY, “driven by robust demand for custom AI accelerators and AI networking.” Management signaled continued momentum, guiding Q2 revenue to about $22 billion, with AI semiconductor revenue expected to reach $10.7 billion. The company also “returned $10.9 billion in the first quarter through $3.1 billion of cash dividends and $7.8 billion of stock repurchases.”

Looking ahead, Wall Street expects fiscal 2026 revenue in the range of $95 billion to $100 billion, with EPS of around $9 to $10. Growth may moderate as comparisons become tougher, leaving future performance closely tied to sustained AI demand.

What Do Analysts Think About AVGO Stock?

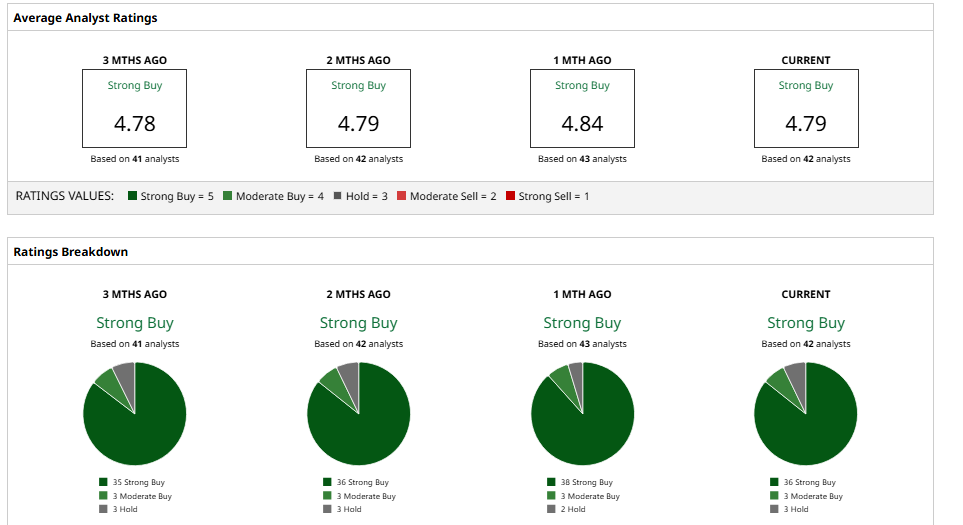

Wall Street remains overwhelmingly bullish on AVGO stock. Morgan Stanley analyst Joseph Moore has an “Overweight” rating and $470 price target, citing a boost in AI revenue. Similarly, JPMorgan has an “Overweight” rating and $500 target, while Bank of America has a $450 target with a “Buy” rating, naming Broadcom as a favorite AI stock. That said, not all analysts are in on AVGO. RBC Capital has a milder $360 price target.

The consensus rating from Wall Street is a “Strong Buy” based on 42 analysts with coverage. The average price target stands at $466.12, signaling potential upside of about 46% from current levels.

The bottom line? Analysts believe that Broadcom's pipeline, particularly its AI switches and dominant position in custom ASICs, justifies the current price.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)