The Iran war will be four weeks old come Saturday. With the White House suggesting negotiations are progressing nicely and the Iranians saying America is “negotiating with itself,” this war looks ready to go the distance.

That’s never good for the markets. Consumers and businesses will soon see what it means for gas prices, inflation, and the general health of the U.S. economy.

Naturally, with all the bad news right now, the NYSE and Nasdaq are seeing more new 52-week lows than highs.

On Tuesday, the NYSE had 113 new 52-week lows, while the Nasdaq had 252. That compares with 86 and 69 new 52-week highs for the former and latter, respectively.

Thanks to the four-week war, the S&P 500 is down over 4% in 2026. Not to be a Debbie Downer, but if the war keeps up, we can kiss a fourth consecutive year of gains goodbye.

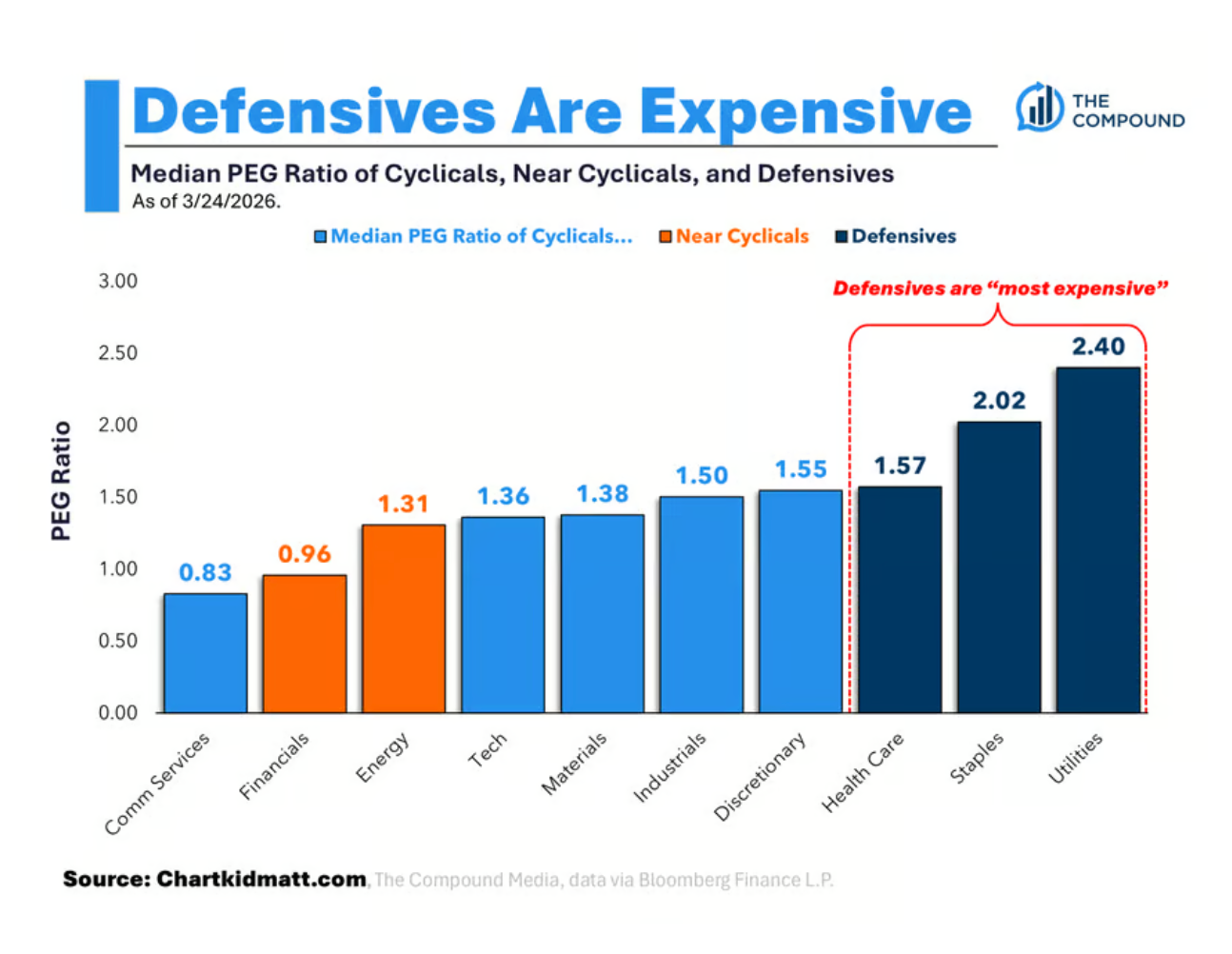

Yesterday, ChartKidMatt’s Matt Cerminaro highlighted that defensive stocks, at least from a median PEG ratio perspective, were the most expensive out of 10 sectors.

Based on his findings, I’ve identified three defensive stocks that hit new 52-week highs yesterday and explain why you might consider taking profits.

Consumer Staples - Darling Ingredients (DAR)

Darling Ingredients (DAR) hit a new 52-week high of $59.36 on Tuesday, the 39th of the past 12 months. DAR shares are up 94.44% in the past year.

This company has been around for a very long time. I can remember a friend recommending its stock over 30 years ago. Founded in 1882, the Chicago-based company has been turning animal byproducts into proteins and fats for over 140 years.

Here in Halifax, where I live, I see the Darling trucks driving around town, picking up used cooking oil and leftover meat byproducts from restaurants in the area. It’s a big business.

In 2025, its revenues were $6.14 billion, 7.4% higher than in 2024. They include $1.2 billion in sales from Diamond Green Diesel, the company’s 50/50 joint venture with Valero Energy (VLO). However, its net income was just $62.8 million, or $0.39 a share, down from $278.9 million, or $1.73 a share.

Because Darling’s business model is capital-intensive — whether through the many acquisitions it makes or the cost of its rendering plants and machinery used to recycle used cooking oil and meat byproducts — it has high depreciation and amortization expenses.

So, it is useful to compare EBITDA (earnings before interest, taxes, depreciation and amortization) from one year to the next. In 2025, it was $1.03 billion, 4.6% lower than $1.08 billion a year earlier. Still lower, but nearly as much as its 77.4% decline in GAAP earnings year-over-year.

If you calculate Darling’s PEG ratio with a trailing 12-month P/E of 148.92, as reported by S&P Global Market Intelligence, and divide it by the average earnings growth rate over the past five years, which is -11.0%, you get -13.5x.

Let’s consider a forward-looking PEG ratio, as opposed to a backward-looking one.

Based on its current share price of $58.47 and a 2026 earnings-per-share estimate of $3.22, its forward P/E is 18.2x. The five-year EPS growth rate is 53.1%, based on earnings rising from a normalized $0.97 per share in 2025 to $8.15 per share in 2030.

Let’s take out the lowest and highest per share figures ($0.97 and $8.15), and you get a 28.9% annual growth rate, so it's still high. However, the forward-looking PEG ratio is 0.63. Anything under 1.0 is good.

So, why sell?

Except for the two years during COVID, when green energy was all anyone talked about, and the company was converting much of the used cooking oil and meat byproducts it collected into fuel, its shares have never traded higher than $60, and for most of its history, above $20.

Of course, with diesel fuel so expensive right now, you might be tempted to play the momentum game a while longer. Don’t.

Sitting on a near double over the past year, there’s no shame in taking profits, especially in a jittery market.

Health Care - Masimo (MASI)

Masimo (MASI) hit a new 52-week high of $179.00 on Tuesday, the 12th of the past 12 months. MASI shares are up 6.61% in the past year.

Normally, one wouldn’t consider a stock that’s gained less than 10% over 52 weeks to be a candidate for selling and taking profits.

However, the company best known for its Masimo SET (Signal Extraction Technology) noninvasive patient monitoring devices -- which accurately measure oxygen saturation and pulse rate (PR) -- received an offer from Danaher (DHR) in February that was too good to turn down. Its shares jumped 34% on the news.

Danaher’s $180 a share offer values Masimo at $9.9 billion, which includes $407 million in net debt, and is approximately 15 times the company’s estimated 2027 EBITDA after taking into account the $175 million in annual cost and revenue synergies Danaher expects to generate from the acquisition within five years post-closing.

At 19 times EBITDA before synergies, Danaher isn’t getting a bargain. Still, given that it can combine its existing Radiometer business with Masimo, it provides Danaher with a strong global diagnostics business, where it can sell more Masimo products in Europe and Radiometer products in the U.S.

At the end of the day, another competing offer isn’t coming. Why not sell and redeploy the capital elsewhere?

Health Care - Eton Pharmaceuticals (ETON)

Eton Pharmaceuticals (ETON) hit a new 52-week high of $23.96 on Tuesday, the 15th of the past 12 months. ETON shares are up 61.48% in the past year.

I don’t spend much time on pharmaceutical companies. From what I can tell, Eton does a good job of developing and bringing drug treatments for rare diseases to market and generating real revenue. It finished 2025 with eight commercially viable products and five in late-stage development.

So, from this perspective, it’s a stock I’d at least consider, unlike research-focused firms that lose millions in the development stages and then sell off the marketing rights to the big drug companies.

From a business perspective, it’s still a relatively small drug company with 2025 revenue of $80.0, double sales a year earlier, with 2026 revenue expected to be at least $110 million, 38% higher than this past year. This revenue estimate seems conservative.

Equally impressive, its non-GAAP net income in 2025 was $10.8 million, or $0.32 a share, substantially higher than its adjusted net income of $869,000 or $0.02 a share in 2024. Further, in 2025, its adjusted EBITDA was $15.8 million. Its 2026 guidance is $33 million, double last year’s EBITDA profit.

So, it’s fair to say that Eton is moving in the right direction, with a development pipeline ready to add to topline sales for years to come. To ensure this happens, it spent $7.8 million in 2025 on R&D (9.7% of revenue), more than double the $3.3 million (8.5%) it spent in 2024. That’s a very good thing.

Why sell if things are so good?

As I write this on Wednesday midday, its shares are up nearly 6% and have hit another new 52-week high at $24.45; also an all-time high. Since hitting a two-year low in April 2024, its shares are up 707%.

I don’t doubt the company’s got a great future, but based on a 2026 adjusted EBITDA of $33 million, it trades at more than 20 times those non-GAAP profits. Further, its P/B ratio is over 25x.

ETON stock is priced for perfection.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)