Berkshire Hathaway (BRK.A) (BRK.B) doesn't make $1.8 billion bets lightly. The conglomerate is doubling down on Japan, and this time, it's not trading houses. Its subsidiary, National Indemnity Company (NICO), is set to acquire a 2.49% stake in Tokio Marine Holdings (TKOMY) for roughly ¥287.4 billion, or about $1.8 billion.

Why Berkshire Is Bullish on Tokio Marine Stock

The deal gives NICO a meaningful ownership stake in one of Asia’s largest insurance companies. According to a company statement, Tokio Marine said it would buy back its own stock to prevent dilution of existing shareholders. NICO has also agreed not to exceed a 9.9% ownership stake without prior board approval.

The partnership goes beyond just owning shares. The two companies plan to collaborate on reinsurance and jointly pursue mergers and acquisitions, combining NICO's enormous capital base with Tokio Marine's global underwriting platform.

Berkshire Hathaway vice chairman Ajit Jain, who oversees the insurance operations, said the company was "pleased to build a long-term collaborative relationship with TMHD, which has a strong underwriting franchise and an exceptional management team."

What is Tokio Marine?

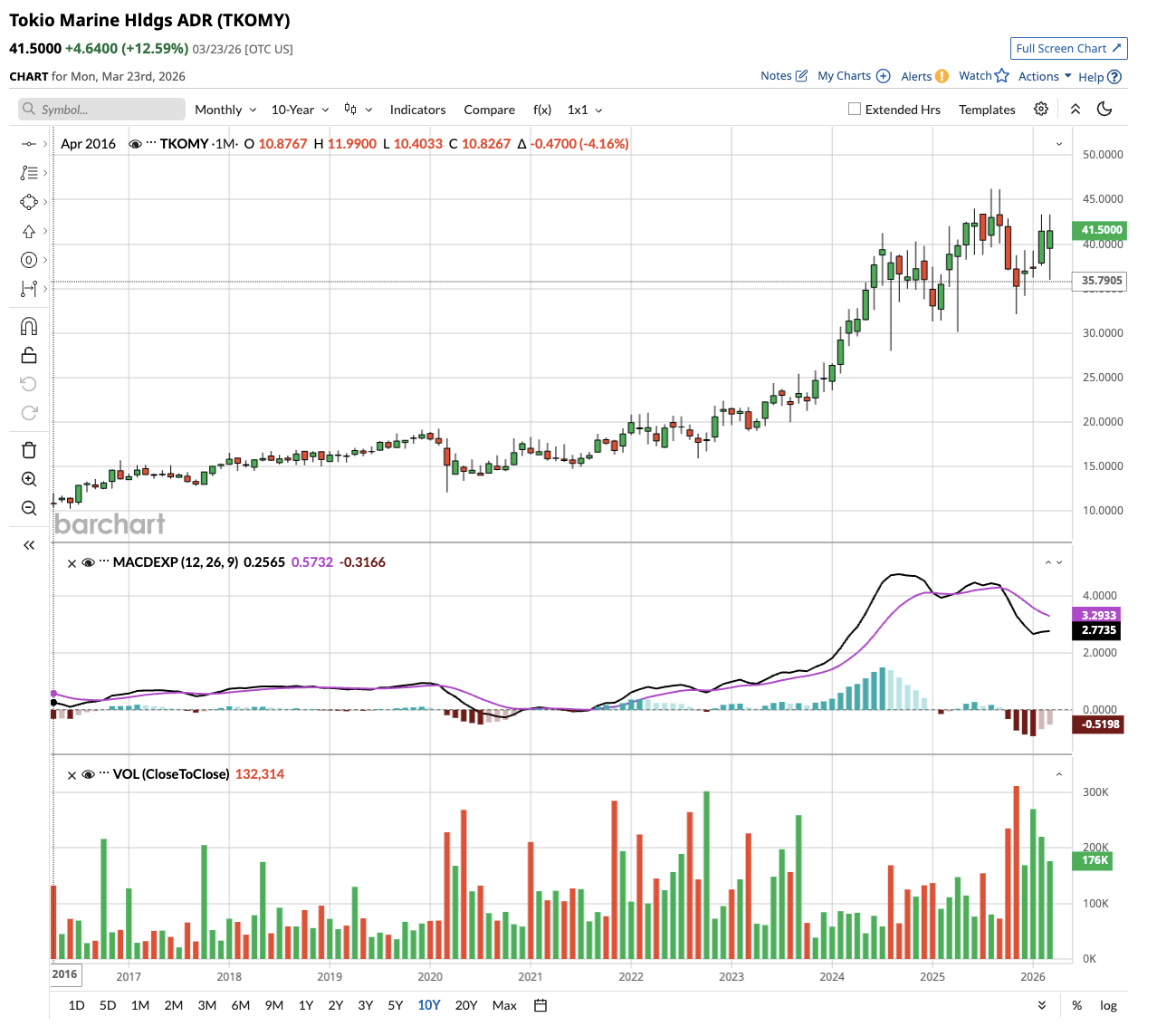

Founded in 1879, Tokio Marine is Japan's oldest insurance company. Most U.S. investors have never heard of it, but the numbers are difficult to ignore.

- Tokio Marine ended fiscal 2025 with $205 billion in total assets.

- It reported earnings per share of $2.47 and is projected to increase earnings to $3.31 in fiscal 2026.

- With a presence in 38 countries, Tokio Marine is also building a massive U.S. footprint.

- Over the past two decades, it has spent more than $17 billion on acquisitions in the United States, including Philadelphia Insurance Companies, HCC Insurance Holdings, and Pure Group.

During a recent investor briefing, Tokio Marine Group CEO Masahiro Koike highlighted a five-year earnings-per-share (EPS) growth rate of nearly 20%, placing it among the best-performing insurers globally. The company is also targeting EPS growth of 8% or more going forward.

Should You Buy TKOMY Stock Right Now?

TKOMY trades on U.S. markets as an American Depositary Receipt (ADR). For investors considering the stock, several things stand out.

Tokio Marine has low EPS growth volatility, a disciplined underwriting culture, and is actively managing capital. Its economic solvency ratio (ESR) is 155%, a measure of financial resilience that indicates the company has room to invest and return cash to shareholders.

The company recently increased its share buyback program to ¥240 billion annually. Dividends are also set to grow in line with earnings, even after the company transitions to International Financial Reporting Standards (IFRS) in fiscal year 2026.

There are risks to keep in mind. North American insurance markets are softening in certain lines. Social inflation, the trend of rising litigation costs, has caused some reserve development in specialty lines. And at current valuations, the stock is not cheap. But Berkshire Hathaway buying $1.8 billion worth of a company is rarely the beginning of a bad story.

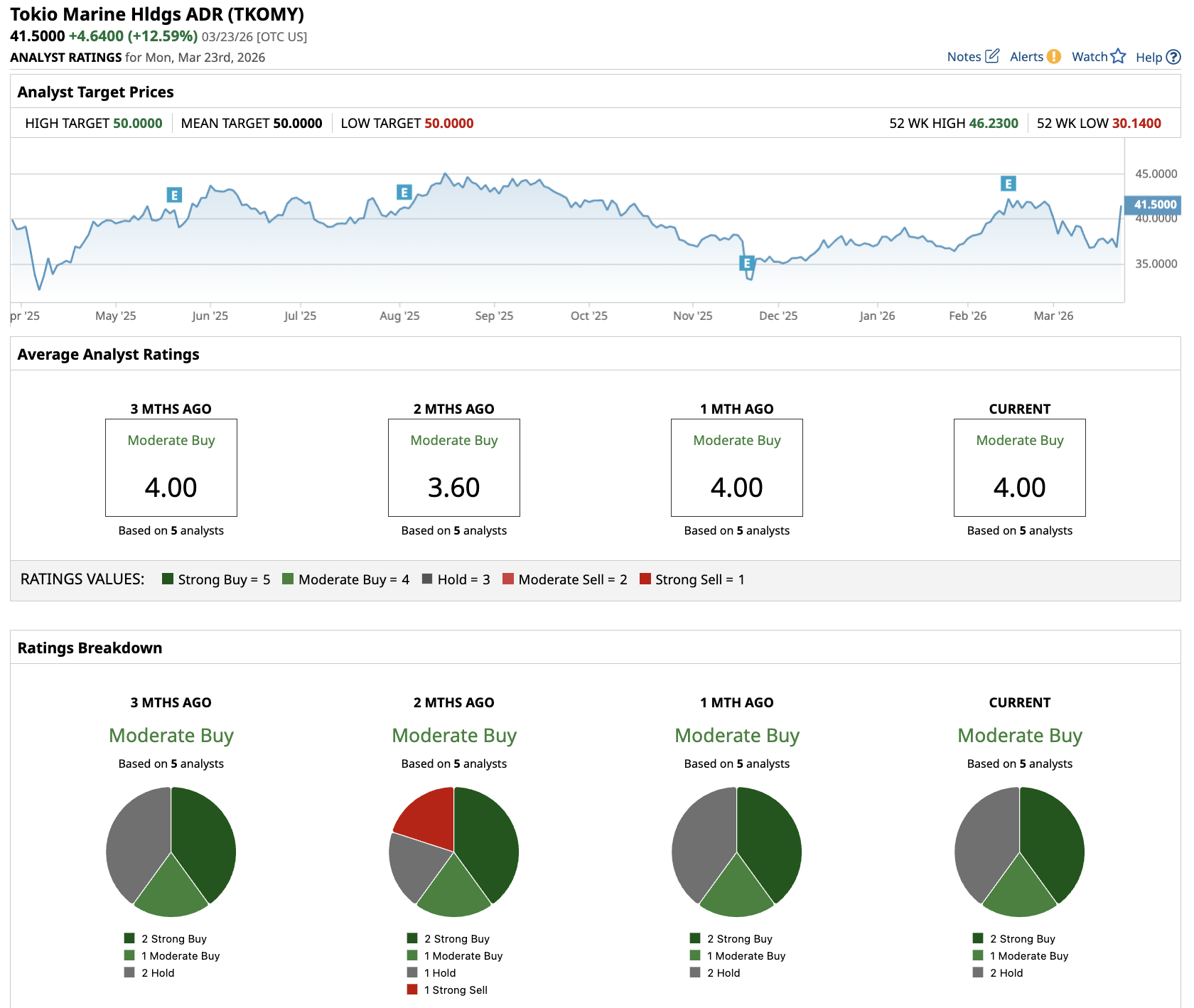

Out of the five analysts covering TKOMY stock, two recommend “Strong Buy,” one recommends “Moderate Buy,” and two recommend “Hold.” The average Tokio Marine stock price target is $50, indicating almost 20% upside from current levels.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)