/Tesla%20Inc%20logo%20by-%20baileystock%20via%20iStock.jpg)

Electric vehicle (EV) industry leader Tesla (TSLA) is set to build two new chip factories at its Austin, Texas, facility in partnership with SpaceX. CEO Elon Musk has stated that the advanced AI chip complex, with two factories, is expected to power cars and humanoid robots, and another is designed for artificial intelligence (AI) data centers in space.

However, this infrastructure buildout is set to entail high costs, scale, and complexity, which Morgan Stanley analysts believe is a “Herculean task.” Analysts wrote in a note that the objective of building “logic, memory, and packaging from a standing start” is quite challenging, and an amount of $20 billion or more over several years is likely insufficient to fully cover development costs.

Can Tesla thrive through this?

About Tesla Stock

Headquartered in Austin, Texas, Tesla is widely regarded as the frontrunner in the EV industry. It designs, manufactures, and sells electric cars, energy storage systems, and solar products, operating large vehicle and battery factories in the U.S., Europe, and China, along with a global network of showrooms and service centers.

In recent months, Tesla has faced investor concerns over softer vehicle deliveries, intensifying competition in the EV and self‑driving spaces, and debates around its AI‑driven strategy and proposed moves such as a semiconductor fab project, all of which have contributed to volatility in the company’s stock and sentiment among shareholders. Tesla has a massive market capitalization of $1.44 trillion.

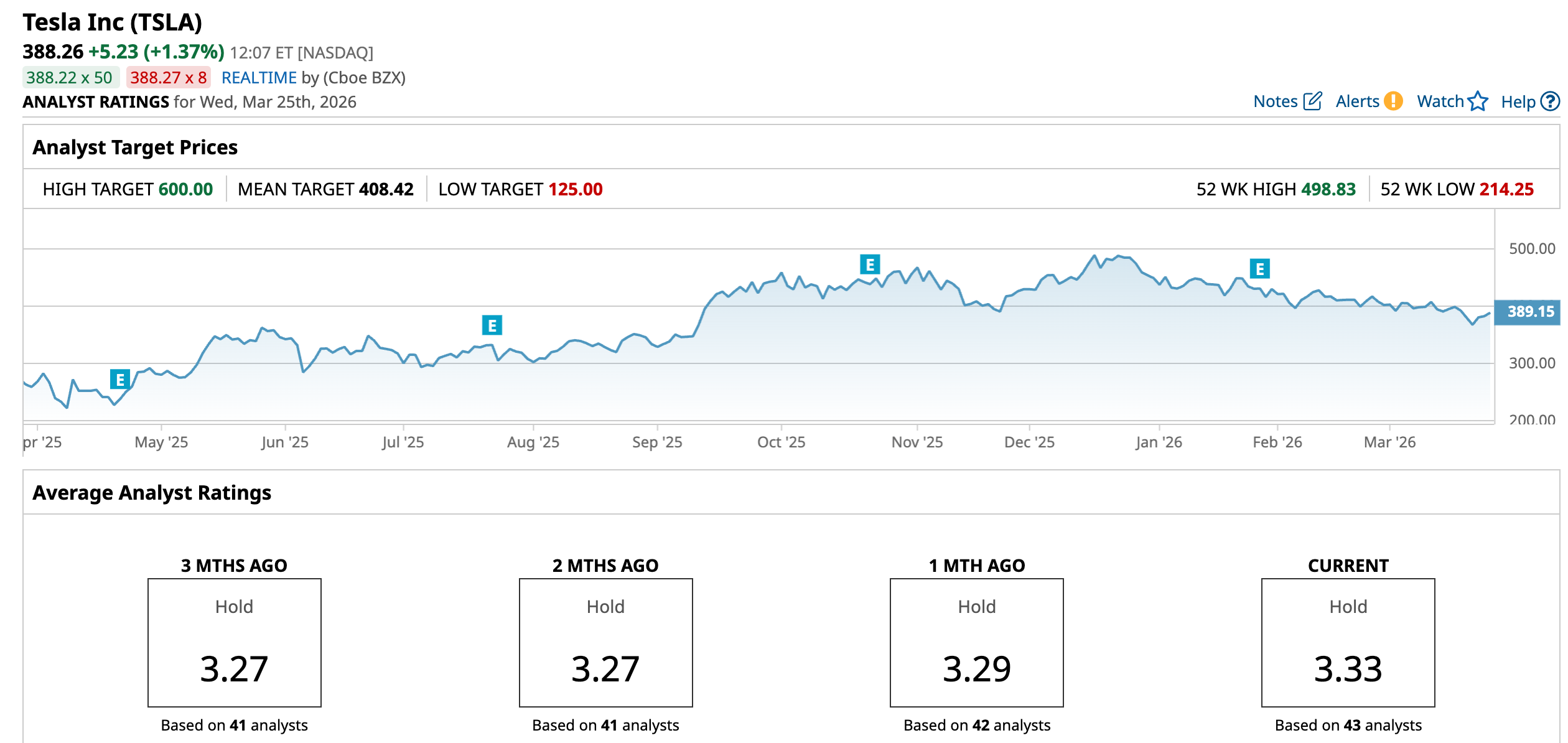

The company’s stock is down significantly from its highs but is still up 36.5% over the past 52 weeks. The recent price performance has not been impressive. This year, the stock is down 12.54%. It had last reached a 52-week high of $498.83 in December 2025, but is down 22% from that level.

Tesla’s stock is trading at an eye-watering valuation. Its forward price-to-non-GAAP earnings multiple is 184.12 times, significantly higher than the industry average of 14.51 times.

Tesla Q4 Earnings Highlight Margin Compression and Growth Concerns

Tesla’s fourth-quarter results highlighted a slowdown that was hard to ignore. Its Q4 vehicle deliveries declined by 16% year-over-year (YOY) to 418,227 units, while production dropped 5% YOY to 434,358 units. However, Tesla’s active full self-driving (FSD) subscriptions reached 1.10 million, up 38% YOY.

Tesla’s total automotive revenues decreased 11% from the prior-year period to $17.69 billion, leading to a 3% drop in total revenues to $24.90 billion. Its operating margin dropped by 50 basis points to 5.7%, while adjusted EBITDA margin declined 17 basis points to 16.7%.

Additionally, the company’s cash flow was affected by the slowdown. Tesla’s Q4 free cash flow was $1.42 billion, down 30% YOY. Its non-GAAP EPS also dropped by 17% annually to $0.50.

Wall Street analysts are optimistic about Tesla’s bottom line growth trajectory. For the current quarter, analysts expect the company’s EPS to grow by 60% YOY to $0.24. For the current year, Tesla’s EPS is projected to increase by 32.1% annually to $1.44, followed by a 35.4% YOY improvement to $1.95 in the following year.

What Analysts Think About Tesla’s Stock

Following an escalation of a federal safety investigation, GLJ Research analysts reiterated a “Sell” rating on Tesla’s stock. The National Highway Traffic Safety Administration (NHTSA) escalated its FSD investigation from a Preliminary Evaluation to an Engineering Analysis and confirmed a pattern. GLJ Research analyst Gordon Johnson said FSD’s visibility failure needs a hardware fix, noting that a recall could kill the robotaxi plan.

Conversely, last month Tigress Financial began coverage of Tesla’s stock with a “Buy” rating and a $550 price target, expecting the company’s long-term growth to remain buoyant as it transitions from a pure-play EV maker to a multi-layered physical AI platform. And, analysts pointed toward Tesla’s growing FSD subscriptions, robotaxis, and Optimus humanoid robots.

In January, Wedbush Securities analysts reiterated an “Outperform” rating on Tesla’s stock and a Street-high price target of $600. Analyst Dan Ives continues to express confidence in the company’s market position.

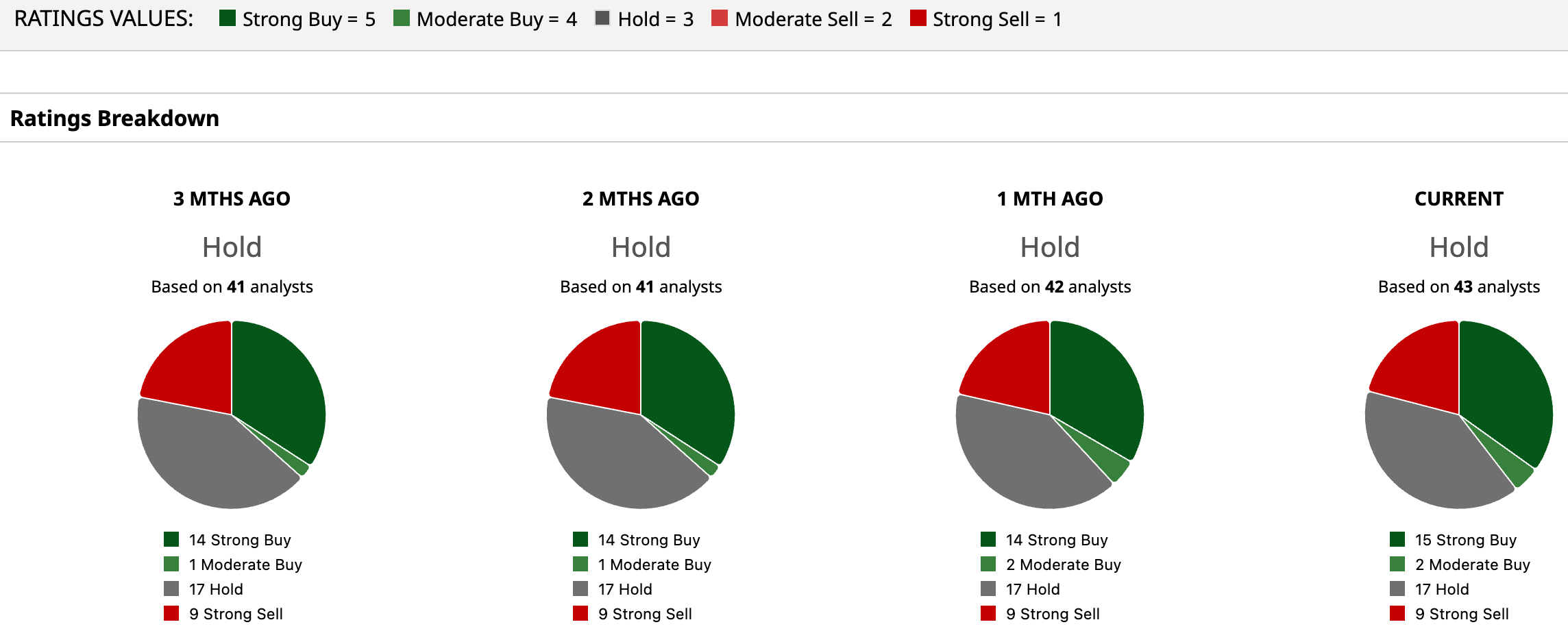

Wall Street analysts are taking a cautious stance on Tesla’s stock now, with a consensus “Hold” rating overall. Of the 43 analysts rating the stock, 15 analysts gave a “Strong Buy” rating, two analysts gave a “Moderate Buy” rating, while 17 analysts are playing it safe with a “Hold” rating, and nine analysts gave a “Strong Sell” rating. The consensus price target of $408.42 represents a 5.2% upside from current levels. Moreover, the Street-high Wedbush price target of $600 indicates a 54.5% upside from current levels.

Key Takeaways

The company stands at a critical juncture, whereby it’s trying to transform into a physical AI giant. Last year marked a crucial step as it furthered its FSD, launched its Robotaxi service, began installing production lines for its Cybercab, and fine-tuned its Optimus design. So, it remains to be seen what happens with the “Terafab” buildout. Therefore, at this moment, it might be prudent to observe Tesla.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)