The Hunt Valley, Maryland-based McCormick & Company, Incorporated (MKC) is a global leader in flavor, generating roughly $7 billion in annual sales across 150 countries. The company produces and markets herbs, spices, seasonings, condiments, and flavors, serving retailers, manufacturers, and foodservice clients.

With a market cap of approximately $14.3 billion, it leans on a diversified brand portfolio, global scale, and steady innovation to capture rising demand for flavor and sustain long-term growth.

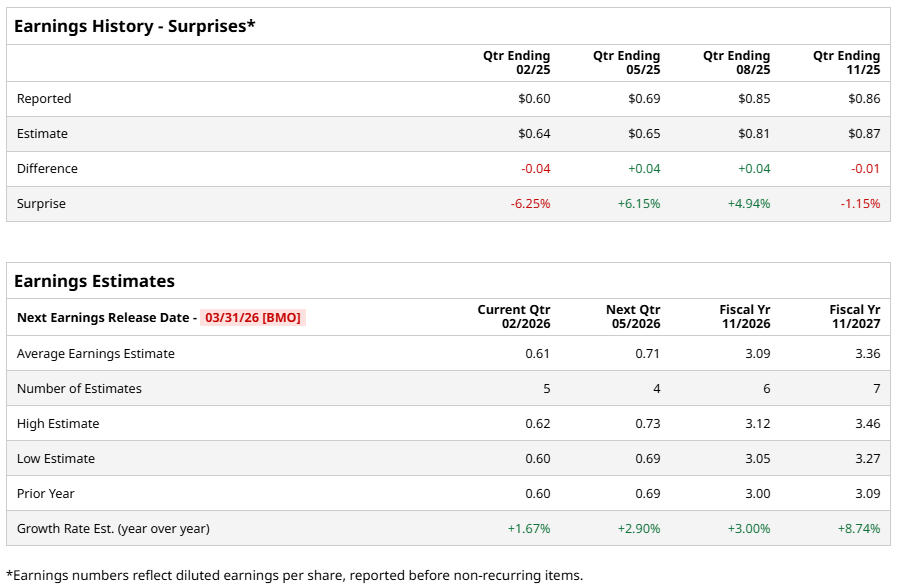

The company is scheduled to release its fiscal 2026 first-quarter earnings results on Tuesday, March 31, before the opening bell. Analysts expect diluted EPS of $0.61, reflecting a modest 1.7% increase from $0.60 in the previous year’s quarter. However, the company has exceeded EPS expectations in two of the past four quarters while falling short in the other two.

Looking beyond the immediate horizon, the Street sketches a steadier climb. Fiscal year 2026 diluted EPS is projected at $3.09, up 3% year over year, before accelerating to $3.36 in fiscal year 2027, implying 8.7% growth.

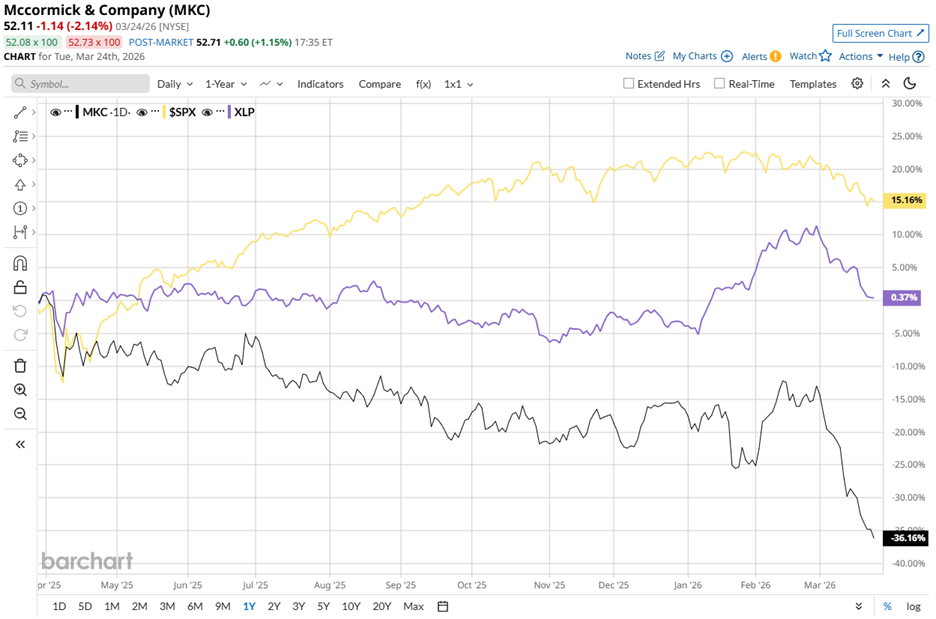

The market, however, has yet to buy into that narrative. Over the past 52 weeks, McCormick’s shares have fallen 35.1%, moving sharply against the grain as the S&P 500 Index ($SPX) gained 13.7%. The disconnect persists in 2026, with the stock down nearly 23.5% year-to-date (YTD), compared to a 4.2% decline for the broader index.

The contrast becomes even more pronounced within its own backyard. The State Street Consumer Staples Select Sector SPDR ETF (XLP) has gained 2.2% over the past year and added 4.4% so far in 2026, reflecting McCormick’s lagging performance.

Management, for its part, has taken a proactive stance. McCormick has confirmed discussions with Unilever PLC (UL) around a potential transaction involving its Foods business, underscoring an intent to reshape the portfolio. The initiative carries strategic significance, as it could streamline operations, refine the company’s focus, and surface value that remains underappreciated in the current setup.

Still, the market has little patience for open-ended outcomes. Limited visibility into the deal’s structure, fruition, timing, and financial implications has kept investors cautious, reflected in a 1.5% decline in the stock following the March 20 announcement.

The opportunity is evident, but so is the uncertainty. Until management provides sharper clarity, the situation is likely to straddle both sides of the equation, offering upside potential while injecting near-term volatility that tempers sentiment.

Even so, analysts have not turned their backs on the stock. McCormick holds a “Moderate Buy” rating, unchanged over the past three months, reflecting steady conviction beneath the surface noise. Out of 13 analysts covering the stock, seven assign it a “Strong Buy,” one calls for “Moderate Buy,” four remain on “Hold,” and one takes a “Strong Sell” stance.

To that end, MKC’s mean price target of $75.92 implies potential upside of 45.7%, while the Street-high target of $89 suggests a gain of 70.8% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)