/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

Recent weakness in large-cap technology stocks has created a potential entry point for long-term investors. Shares of big tech companies have come under pressure amid escalating geopolitical tensions tied to the Iran war. Investors are increasingly assessing the broader implications of potential supply chain disruptions, rising energy costs, and the possibility of interest rate increases.

In addition to macroeconomic concerns, investor sentiment has been affected by scrutiny of elevated capital expenditure plans among large technology firms. Market participants are weighing the scale of these investments against the timeline and the certainty of future returns, which is contributing to downward pressure on valuations.

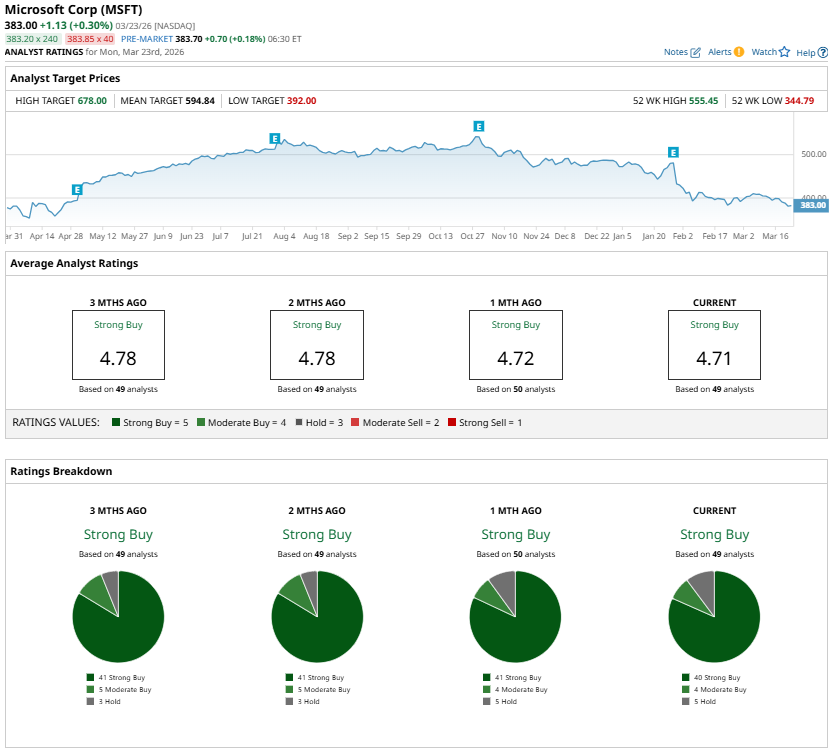

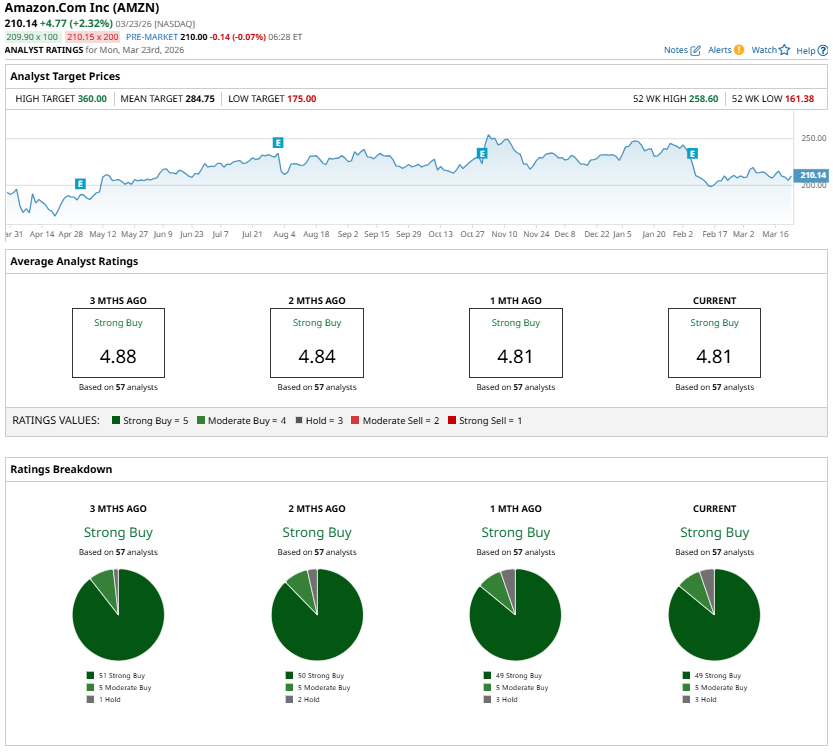

Despite the current headwinds, analyst sentiment toward Microsoft (MSFT) and Amazon (AMZN) remains constructive. Both companies continue to carry a “Strong Buy” consensus rating, supported by their dominant positions in a segment that is witnessing solid structural demand. The recent pullback in share prices is therefore viewed by many analysts as an opportunity to accumulate positions, with expectations of meaningful upside over time.

Strong Buy Tech Stock #1: Microsoft (MSFT)

Microsoft's shares have declined more than 32% from their 52-week high, reflecting investor concerns over rising capital expenditures and customer concentration tied to OpenAI. A significant portion of Microsoft’s backlog is linked to OpenAI-related agreements, raising questions about revenue diversification within its cloud business.

The company is investing heavily to expand its AI infrastructure, focusing on high-performance hardware such as GPUs and CPUs, alongside global data center growth. While these investments are expected to pressure margins in the near term, they are providing a solid base for capturing long-term opportunities in cloud computing and AI.

Supporting its higher spending are the solid demand trends. In the second quarter, revenue increased 17% year-over-year (YoY), while earnings per share rose 24%. Microsoft Cloud generated $51.5 billion in revenue, up 26% YoY. The Intelligent Cloud segment delivered robust results, with revenue rising 29% to $32.9 billion. Azure revenue grew 39%, slightly below the prior quarter’s 40% growth, primarily due to capacity constraints rather than weakening demand.

Demand for cloud and AI services continues to exceed available infrastructure, suggesting sustained growth potential as capacity expands. Management expects this momentum to persist across industries and geographies.

For the third quarter, Microsoft forecasts total revenue between $80.65 billion and $81.75 billion, implying growth of 15% to 17%. Intelligent Cloud revenue is projected at $34.1 billion to $34.4 billion, with Azure expected to grow 37% to 38% in constant currency.

Although approximately 45% of MSFT’s $625 billion remaining performance obligation (RPO) is tied to OpenAI, the rest of the backlog grew 28%, highlighting diversified demand. Supported by strong fundamentals, expanding cloud adoption, and continued AI investment, Microsoft has a favorable long-term outlook. The consensus price target of $594.84 implies about 55% upside potential over the next 12 months.

Strong Buy Tech Stock #2: Amazon (AMZN)

Amazon has also declined about 19% from its 52-week high following management’s announcement of a substantial increase in capital expenditures through 2026. The company expects to invest approximately $200 billion, with the majority allocated to Amazon Web Services (AWS).

This marks one of Amazon’s largest investments. However, investors should note that the scale of spending reflects significant growth opportunities for the company, led by demand across cloud computing, AI, custom silicon, robotics, and satellite infrastructure.

AWS continues to contribute significantly to Amazon’s growth. The segment delivered accelerating growth, with revenue rising 24% in the fourth quarter, up from 20% in the prior quarter. Sequential revenue increased by $2.6 billion and nearly $7 billion YoY, supported by higher customer usage and rapid capacity deployment. At its current trajectory, AWS is operating at an annualized revenue run rate of approximately $142 billion and continues to serve as Amazon’s primary profit driver.

Within AWS, Amazon’s proprietary chips, including Graviton and Trainium, have surpassed a $10 billion annual revenue run rate and are expanding at triple-digit rates. In parallel, traditional cloud workloads are also gaining momentum as enterprises accelerate infrastructure migration. Amazon’s comprehensive service offerings, strong security capabilities, and extensive partner ecosystem continue to support higher adoption.

Beyond cloud, Amazon’s advertising business remains a high-margin growth driver, with revenue increasing 22% in the fourth quarter and contributing over $12 billion in incremental revenue during 2025. Retail operations are also improving through enhanced fulfillment efficiency and cost optimization.

Although higher capital expenditures may pressure near-term margins, they will likely position AMZN to capture strong demand and drive rapid monetization of new capacity. Amazon’s diversified growth engines support a favorable long-term outlook, with a consensus price target of $284.75 implying roughly 36% upside potential.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)