Valued at a market cap of $21.9 billion, Williams-Sonoma, Inc. (WSM) is an omni-channel specialty retailer that offers various home products. The San Francisco, California-based company offers a wide array of cookware, furniture, home furnishings, and decorative accessories.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and WSM fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the specialty retail industry. The company commands a significant presence in the e-commerce landscape and maintains a strategic network of retail stores across the United States, Canada, Australia, and the United Kingdom, supplemented by franchise agreements in various international markets.

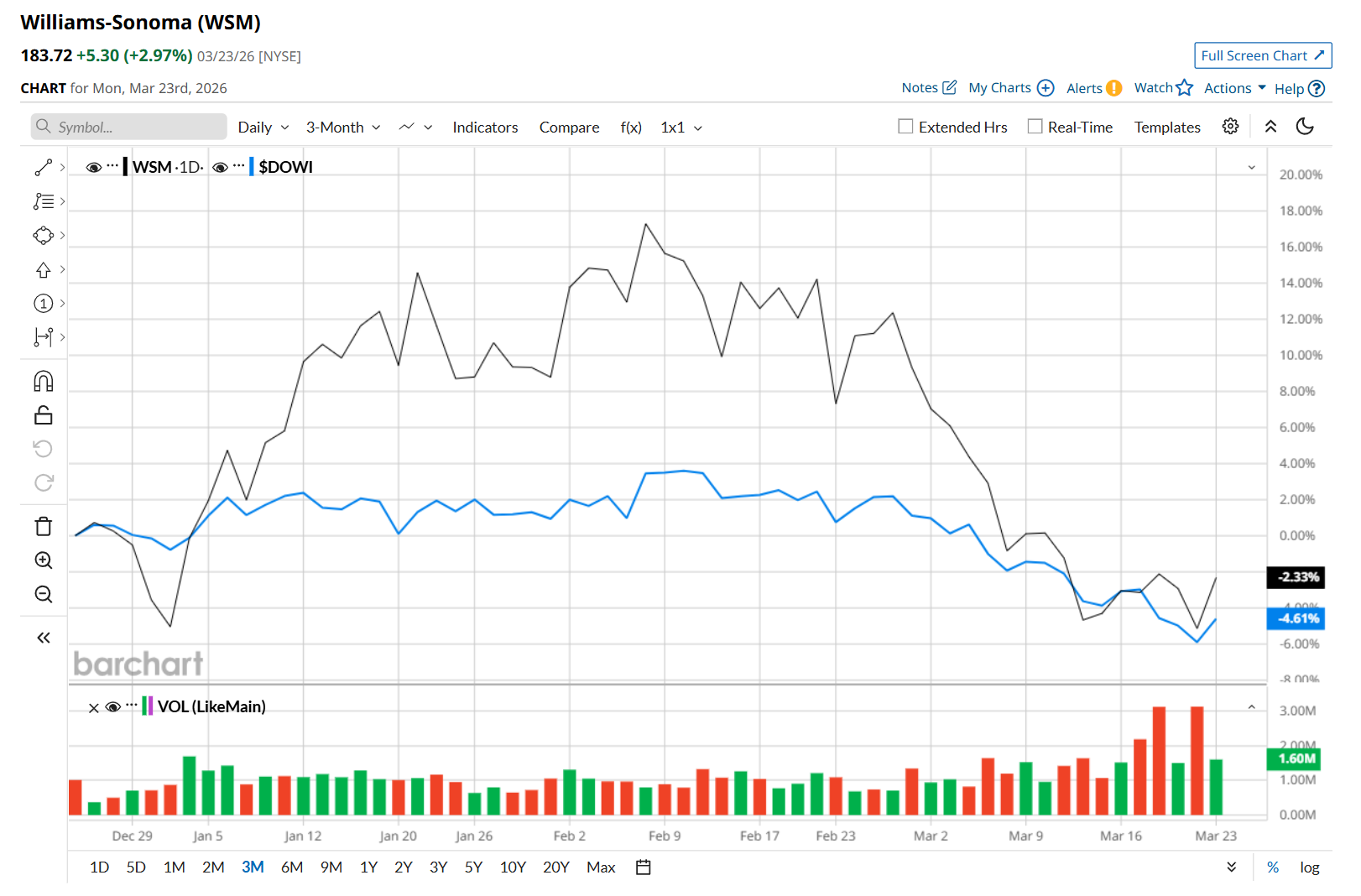

This specialty retailer has dipped 17.2% from its 52-week high of $222, reached on Feb. 20. Shares of WSM have declined 2.3% over the past three months, outperforming the Dow Jones Industrial Average’s ($DOWI) 4.6% drop during the same time frame.

Moreover, on a YTD basis, shares of WSM are up 2.9%, compared to DOWI’s 3.9% loss. In the longer term, WSM has surged 12.3% over the past 52 weeks, outpacing DOWI’s 10.1% uptick over the same time frame.

To confirm its recent bearish trend, WSM has been trading below its 200-day moving average since early March and has remained below its 50-day moving average since late February.

On Mar. 18, shares of WSM surged 1.1% after it reported mixed Q4 results. The company posted earnings per share of $3.04, beating analyst estimates of $2.89, supported by a 3.2% increase in same-store sales and an improved gross margin. However, its total revenue declined 4.3% year-over-year to $2.4 billion, missing Wall Street forecasts. Additionally, its operating margin narrowed to 20.3% from 21.5% in the prior-year quarter, reflecting higher operating expenses. Despite the revenue miss, investors seemed encouraged by the stronger-than-expected profitability amid a challenging sales environment.

WSM has considerably outpaced its rival, RH (RH), which declined 49.8% over the past 52 weeks and 27.8% on a YTD basis.

Looking at WSM’s recent outperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 20 analysts covering it, and the mean price target of $210.28 suggests a 14.1% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Broadcom%20Inc%20HQ%20photo-by%20Sundry%20Photogrpahy%20via%20iStock.jpg)