/Hasbro%2C%20Inc_%20monopoly%20by-%20txking%20via%20iStock.jpg)

Hasbro, Inc. (HAS), headquartered in Pawtucket, Rhode Island, functions as a toy and game company. Valued at $12.8 billion by market cap, the company offers a diverse range of toys, games, interactive software, puzzles, and infant products through popular brands like MAGIC: THE GATHERING, Hasbro Gaming, PLAY-DOH, NERF, TRANSFORMERS, DUNGEONS & DRAGONS, PEPPA PIG, and more.

Companies worth $10 billion or more are generally described as “large-cap stocks,” and HAS definitely fits that description, with its market cap exceeding this threshold, reflecting its substantial size, influence, and dominance in the leisure industry. Hasbro's strengths include iconic brands, global distribution, strategic licensing, digital transformation, and innovation. These drive its market reach and revenue growth.

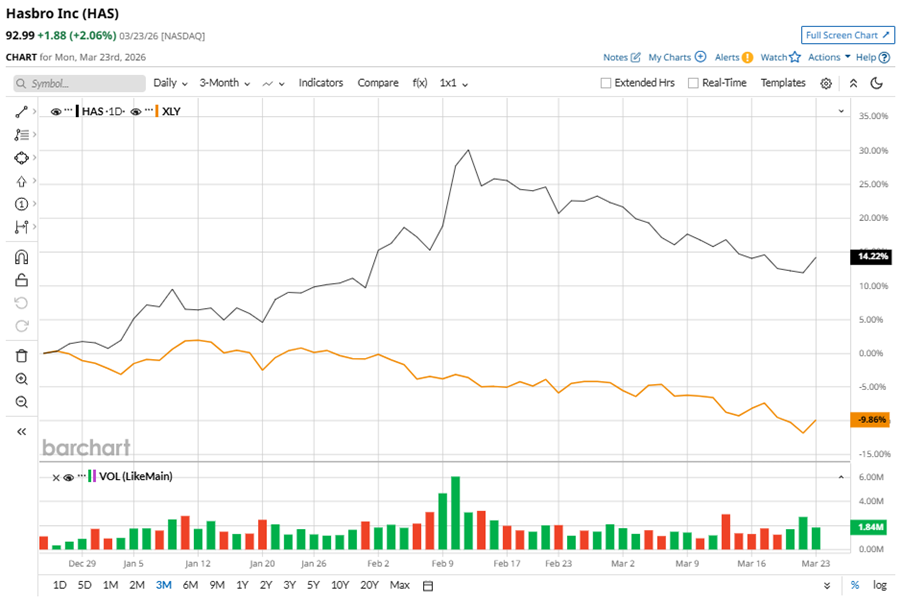

Despite its notable strength, HAS slipped 13.1% from its 52-week high of $106.98, achieved on Feb. 12. Over the past three months, HAS stock gained 14.2%, outperforming State Street Consumer Discretionary Select Sector SPDR ETF’s (XLY) 9.9% dip during the same time frame.

Shares of HAS rose 24.3% on a six-month basis and climbed 53.5% over the past 52 weeks, outperforming XLY’s YTD losses of 7.4% and 11.5% returns over the last year.

To confirm the bullish trend, HAS has been trading above its 200-day moving average since mid-May, 2025. However, the stock is trading below its 50-day moving average since mid-March.

Hasbro's Q4 results were strong, driven by massive growth in MONOPOLY, Peppa Pig, Marvel, and Wizards of the Coast's Magic: The Gathering. The consumer products division returned to growth, and new licensing deals with Warner Bros. Discovery, Inc. (WBD), The Walt Disney Company (DIS), and Amazon.com, Inc. (AMZN) are expected to fuel future launches.

On Feb. 10, HAS shares closed up by 7.5% after reporting its Q4 results. Its adjusted EPS of $1.51 exceeded Wall Street expectations of $0.99. The company’s revenue was $1.4 billion, exceeding Wall Street forecasts of $1.3 billion.

In the competitive arena of leisure, Mattel, Inc. (MAT) has lagged behind HAS, with an 11.6% downtick over the past six months and 23.8% losses over the past 52 weeks.

Wall Street analysts are bullish on HAS’ prospects. The stock has a consensus “Strong Buy” rating from the 15 analysts covering it, and the mean price target of $113.07 suggests a notable potential upside of 21.6% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)