Rising geopolitical tensions are once again reshaping the macro landscape. The ongoing Middle East conflict has pushed oil prices sharply higher, reigniting inflation concerns just as markets were hoping for a more stable price environment. At the same time, there is growing unease that elevated energy costs could act as a drag on economic activity, squeezing consumers and businesses alike. This combination of persistent inflation and slowing growth has revived fears of a stagflationary environment—one of the most challenging backdrops for traditional equity portfolios.

In such conditions, many high-growth stocks tend to struggle. As a result, investors are increasingly shifting their focus toward income-generating assets that can offer more resilience when capital appreciation becomes harder to achieve. High-yield dividend stocks, in particular, can play a critical role by providing a steady stream of income that helps offset market volatility and eroding purchasing power.

Against this backdrop, Conagra Brands (CAG), Energy Transfer (ET), and Kraft Heinz (KHC) stand out as compelling options. All three companies have been identified by Barchart as attractive investments for periods of stagflation, thanks to their strong dividend profiles and defensive characteristics. Let’s take a closer look!

High-Yield Stock #1: Conagra Brands (CAG)

Conagra Brands is a prominent company in the consumer packaged foods industry. The company has a diverse portfolio of well-known brands, including Birds Eye, Marie Callender’s, Duncan Hines, Healthy Choice, Slim Jim, and Reddi-wip. Conagra operates across four primary segments: Grocery & Snacks, which offers shelf-stable products; Refrigerated & Frozen, focused on temperature-controlled goods; International, covering markets outside the U.S.; and Foodservice, supplying branded and customized culinary products to restaurants. Its market cap currently stands at $7.3 billion.

Shares of the consumer packaged foods company have fallen 11% on a year-to-date (YTD) basis. The stock came under pressure from broad-based declines on Wall Street tied to the Middle East conflict, with additional weakness driven by Campbell’s disappointing FQ2 results.

Conagra Brands is viewed as a strong defensive investment during periods of stagflation due to its position in the consumer staples sector. Stagflationary periods cause consumers to tighten their belts. As a producer of essential food items, Conagra’s demand remains stable, or “recession-resistant,” because people must eat regardless of economic conditions. Also, the company has demonstrated the ability to pass on rising input costs to consumers, a critical capability during stagflation.

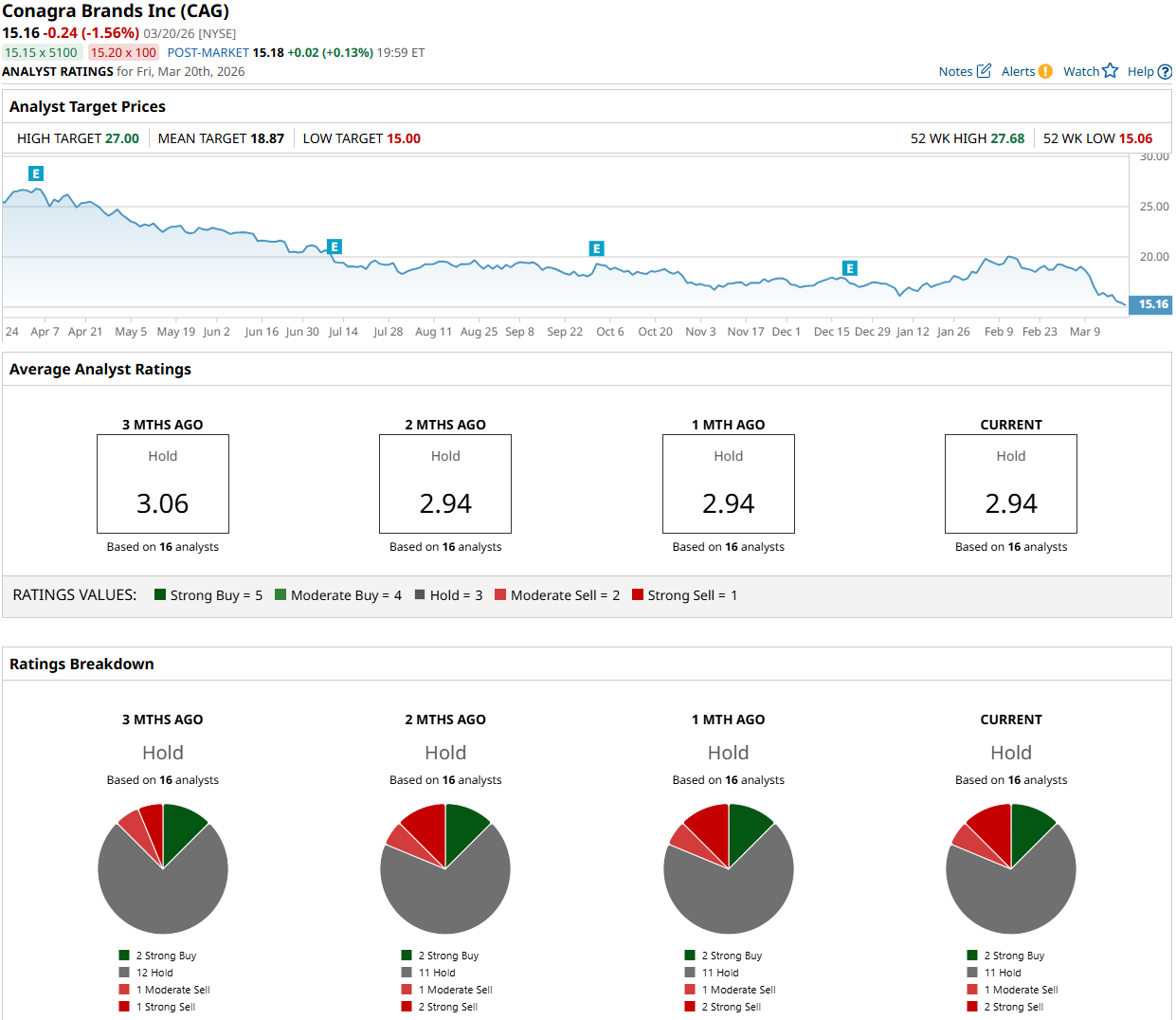

A 9.2% forward dividend yield adds to the stock’s attractiveness for income-focused investors willing to ride out near-term volatility or even a stagflationary environment. This is significantly higher than the sector median of 3.23%. Notably, Conagra currently offers the highest dividend yield in the S&P 500 ($SPX). However, some analysts have become skeptical that the company’s fat dividends may be at risk. But let’s take a closer look at some numbers. Conagra’s dividend payout ratio stands at 72.77%. And while its profit is projected to decline -25.13% year-over-year (YoY) to $1.72 per share in FY26, it still comfortably covers the company’s $1.40 per share annual dividend. That said, there is little reason to anticipate a dividend cut, particularly as analysts expect Conagra’s profit to return to growth in FY27.

Meanwhile, the stock looks cheap both historically and relative to peers, trading at a forward non-GAAP P/E of just 8.80x.

Wall Street analysts have a consensus rating of “Hold” on Conagra's stock. Among the 16 analysts covering the stock, two rate it a “Strong Buy,” 11 recommend holding, one assigns a “Moderate Sell” rating, and the remaining two issue “Strong Sell” ratings. The average price target for CAG stock is $18.87, representing 24.5% upside from Friday’s closing price.

High-Yield Stock #2: Energy Transfer LP (ET)

Energy Transfer LP is a Dallas-based, leading U.S. midstream energy company that owns and operates over 140,000 miles of pipelines, terminals, and storage facilities for natural gas, crude oil, NGLs, and refined products across 44 states. The company provides gathering, processing, and transportation services, connecting major production basins to domestic and international markets. Notably, it is structured as a master limited partnership (MLP). ET has a market cap of $65.4 billion.

Shares of the midstream giant have climbed 14.3% YTD, fueled by a mix of growth reacceleration and higher oil prices.

Energy Transfer LP is considered a wise investment during periods of stagflation because it operates as a “toll booth” for the energy sector. When inflation is specifically driven by higher oil prices, ET can benefit from increased domestic production and intrinsic inflation hedges built into its business model. Instead of depending on volatile commodity prices, ET earns revenue based on the volume of product moving through its pipeline. When oil prices are high, domestic producers are incentivized to increase output, leading to higher throughput volumes and more fees for ET. Notably, about 90% of ET’s adjusted EBITDA is fee-based. Moreover, unlike many other sectors, midstream energy infrastructure often has contractual protections against rising costs.

But don’t forget the second part of the adjusted EBITDA growth equation, as the company has been actively pursuing multiple expansion projects. Management expects 2026 adjusted EBITDA to increase by more than 10% YoY at the midpoint of the $17.45 billion to $17.85 billion guidance range, supported by the ramp-up and completion of several major expansion projects. That compares with 3.2% YoY adjusted EBITDA growth in 2025. And growth at an accelerated pace is expected to continue over the coming years, thanks to the company’s large backlog of expansion projects.

In a stagflationary environment where traditional growth stocks will likely struggle, ET offers a significant income component. Once again, Energy Transfer is an MLP, a specialized structure that passes through its profits, losses, and depreciation deductions directly to its partners (investors). Many MLPs offer sizable distributions (dividends), which helps explain ET’s substantial 7% distribution yield. MLP distributions are generally not taxed upon receipt. Instead, they reduce the investor’s cost basis, meaning taxes are deferred until the units are sold. Meanwhile, the company has stated a goal of increasing its distribution by 3% to 5% annually.

Meanwhile, the stock trades at a forward EV/EBITDA multiple of 8.68x, slightly above its five-year average of 7.86x, yet still below many other MLPs such as EPD and WES.

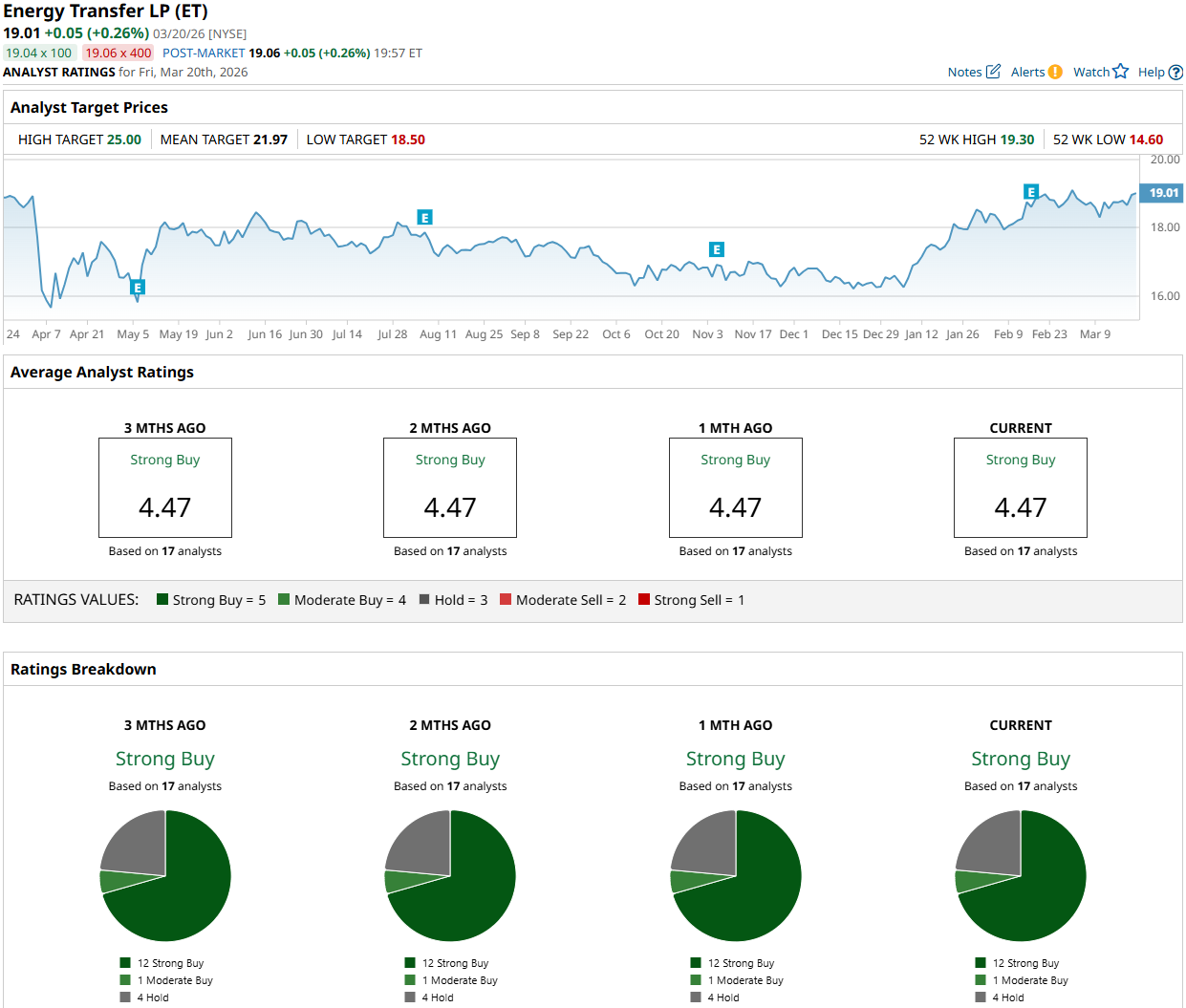

Overall, Wall Street analysts have deemed Energy Transfer stock a consensus “Strong Buy,” with a mean price target of $21.97, indicating an upside potential of 15.6% from Friday’s closing price. Of the 17 analysts covering the stock, 12 have a “Strong Buy” recommendation, one has a “Moderate Buy,” and four suggest holding.

High-Yield Stock #3: The Kraft Heinz Company (KHC)

With a market cap of $25.5 billion, The Kraft Heinz Company is a global food and beverage powerhouse. The company produces and sells a broad range of products, including condiments, sauces, cheese, meals, meats, and beverages, under well-known brands such as Kraft, Oscar Mayer, Heinz, Philadelphia, and Lunchables. It distributes its products through multiple channels, including supermarkets, convenience stores, and e-commerce platforms, with a substantial share of revenue generated from key customers such as Walmart (WMT).

Shares of the food company have dropped 10% YTD. The stock’s decline came amid structural headwinds from the rise of private labels, shifting health trends, and brand- and strategy-specific challenges.

The Kraft Heinz Company can be a solid investment candidate for stagflation due to its defensive, consumer-staples nature. Kraft Heinz produces essential goods that people continue to buy regardless of economic conditions. During economic downturns, consumers tend to eat at home more often to save money, which can bolster sales for retail-focused brands like Kraft. Overall, the company could offer some kind of stability when growth stalls and inflation erodes purchasing power.

What makes Kraft Heinz an even more attractive option for stagflation is its high dividend yield. It continues to pay a $0.40 quarterly dividend, a level it has maintained since its 36% cut in 2019. This equates to $1.60 on an annualized basis. At current share prices, the $1.60 annual dividend translates to a 7.42% yield. In a stagflationary environment where capital gains may be limited, this recurring income provides a significant portion of total returns. And the dividend looks safe, with a payout ratio of just 61.78% and earnings expected to remain sufficient in the coming years to comfortably cover the payout.

KHC stock is currently trading at an attractive valuation relative to its historical averages and peers. Its forward non-GAAP P/E ratio stands at 10.60x, compared to a five-year average of 12.49x and a sector median of 14.41x.

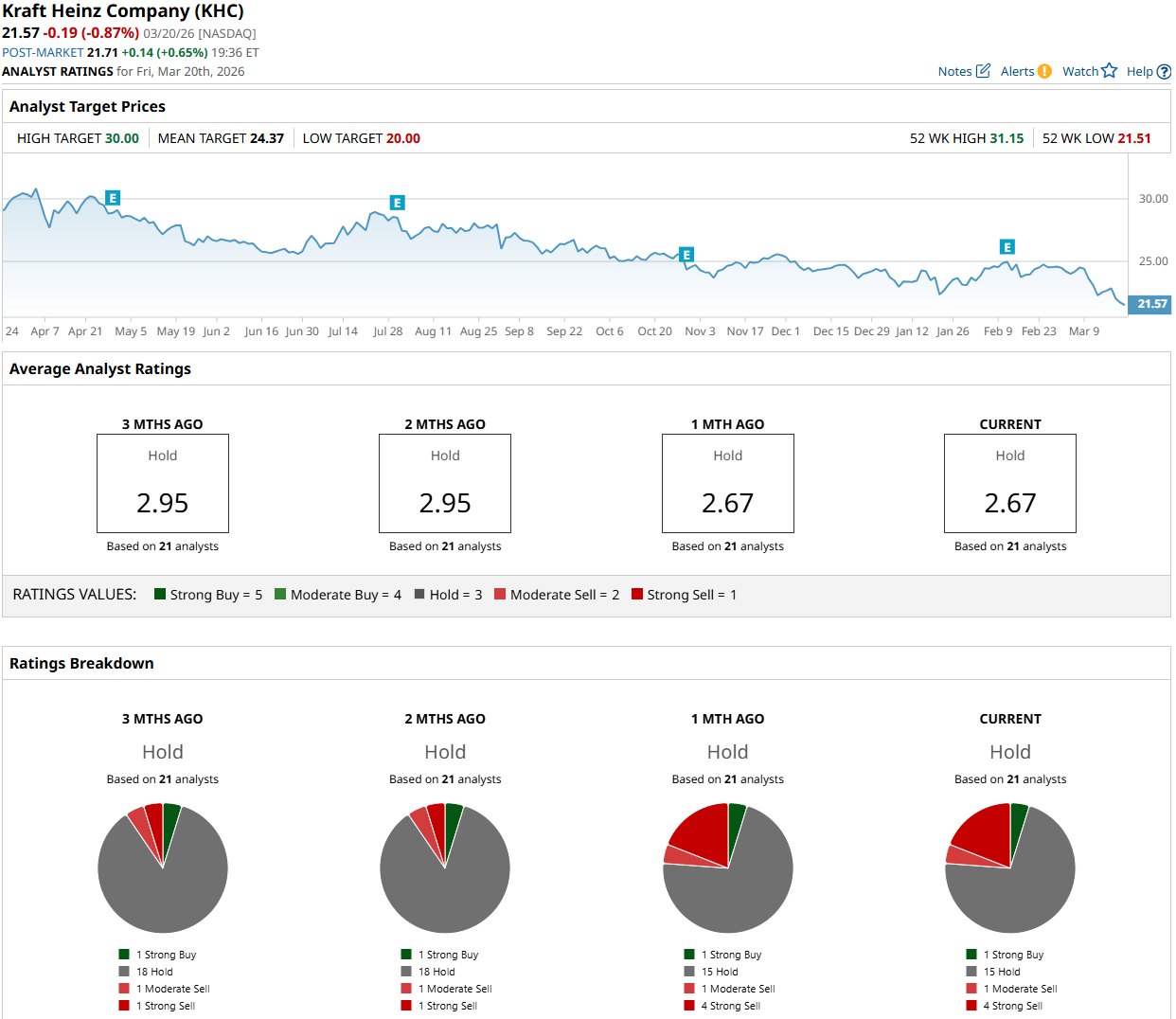

Wall Street analysts have a consensus “Hold” rating on Kraft Heinz stock. Among the 21 analysts covering KHC stock, one has a “Strong Buy” recommendation, 15 advise holding, one suggests a “Moderate Sell,” and four issue “Strong Sell” ratings. The average analyst price target of $24.37 indicates a potential upside of 13% from Friday’s closing price.

On the date of publication, Oleksandr Pylypenko did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)