Devon Energy (DVN) pays a very high dividend each quarter. Most of this comes from the variable portion of the dividend. Last quarter it paid out 16 cents for the fixed amount of the dividend and $1.11 for the variable amount, for a total of $1.27. That gives it an annual run-rate dividend of $5.08. At today's price of $54.70, the apparent yield is 9.30%.

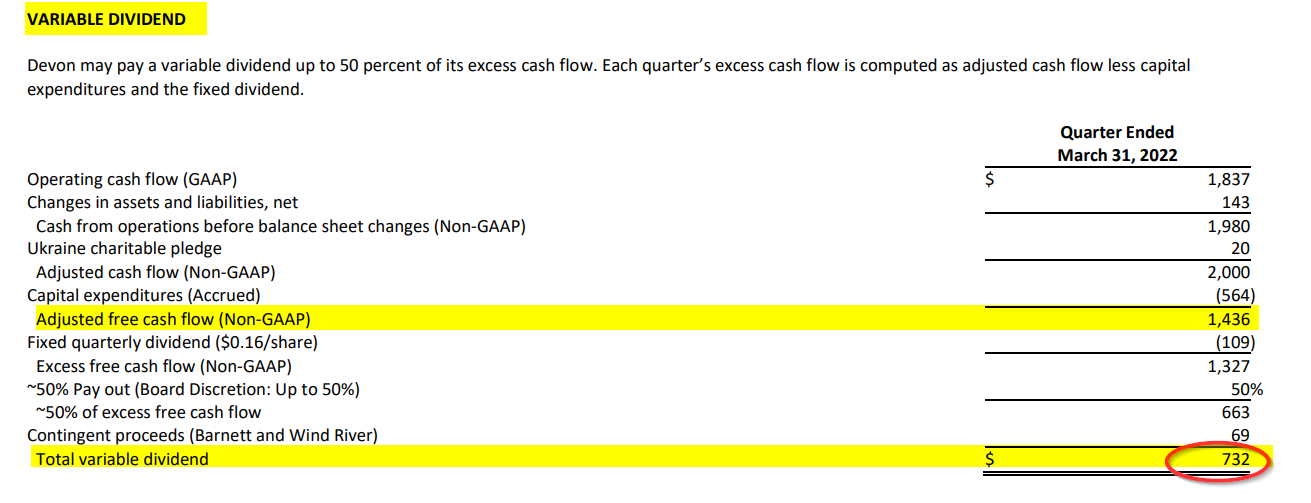

However, the variable portion of the divided changes each quarter. This is calculated as 50% of its adj. op. free cash flow. That worked out to $732 million last quarter, after deducting the 16 cents dividend or $109 million quarterly. That was also based on a very high operating cash flow margin

To be conservative we can assume that its adj. operating cash flow will be at least $550 million. Based on 658 million shares outstanding at the end of the quarter (and it could be much less), that brings the variable dividend down to 84 cents.

This lowers the total dividend to $1.00 per share (i.e., 84 cents + 16 cents fixed), and an annual dividend of $4.00. That gives the stock a run-rate dividend of 7.31%.

We Could Be Too Conservative

Now our assumption of a 25% cut in the quarterly adjusted operating cash flow could be way too conservative. Oil jumped about $10.41 per barrel during Q1 from the prior quarter, based on the company's realized pricing. This can be seen on page 8 of its supplemental data table.

That represented a gain of over 23% in its realized per barrel revenue. Since then I suspect that oil has fallen about one-quarter to one-third of that amount. But that still represents a 15% or so gain over the Q4 numbers. And that was when the company last paid out $1.00 per share in dividends.

Recently The company announced another major bolt-on acquisition in the Williston Basin at just 2.2x free cash flow. As a result of that acquisition, the company announced a 13% increase in its fixed dividend portion to about 18 cents, up from 16 cents. To be conservative, we have incorporated that into our $1.00 quarterly dividend estimate.

The company said that the transaction advances its financial strategy of returning capital to shareholders.

Share Buybacks

Devon stock is very cheap. For example, analysts expect that its 2022 EPS will reach $8.92 per share. That puts it on a very inexpensive multiple of 6.1x. Moreover, 2023 earnings are forecast to stay high at $8.88 per share. For that to happen, oil and gas prices have to stay close to where they are today. This will keep the P/E multiple very low.

On top of this Devon announced on Feb. 15 that it upped its buyback authorization to $1.6 billion by 60 percent. That works out to 4.2% of its $38 billion market capitalization. If it were to buy back this amount in one year that would use up 55% of the $2.9 billion in FCF it generated last year.

This will also lower the total number of shares outstanding, which automatically increases the dividend per share for the same amount of dividend paid out.

As a result, Devon Energy looks very cheap here, especially if oil and gas stay at these levels.

More Stock Market News from Barchart

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)