Tech stocks have been on a roller coaster lately, especially the AI-chip leaders. Nvidia’s (NVDA) stock zoomed in 2023-2025 as everyone chased generative AI. This year has been a bit choppier. AI names have pulled back from last fall’s highs, as investors fret over valuation and competition. However, the demand is not slowing. The AI market could explode to $5.26 trillion by 2035, up sharply from $274 billion in 2023, according to an estimate.

Nvidia has been in the headlines for so many reasons, but this time it's a little different. Yesterday, Elon Musk tweeted on X that he’s a “huge admirer” of Nvidia and CEO Jensen Huang, adding that SpaceX and Tesla (TSLA) will keep buying Nvidia chips at scale. That praise, from one of Silicon Valley’s top customers, refocused attention on Nvidia’s leadership in AI semiconductors. It raises the question: with Musk as a fan and big orders coming, is NVDA stock suddenly too attractive to ignore?

AI Leadership Built on Chip Dominance

Nvidia is the frontrunner in AI because it dominates the most important layer, chips, with about 90% market share, giving it a huge lead over rivals like AMD (AMD) and Intel (INTC). As the AI chip market is predicted to grow from $500 billion to $1 trillion by 2030, Nvidia is in the best position to capture that growth. It’s also expanding beyond data centers into “physical AI,” powering robots, drones, and autonomous systems. Moreover, Nvidia is moving into software, aiming to control the entire AI ecosystem, which strengthens its long-term advantage.

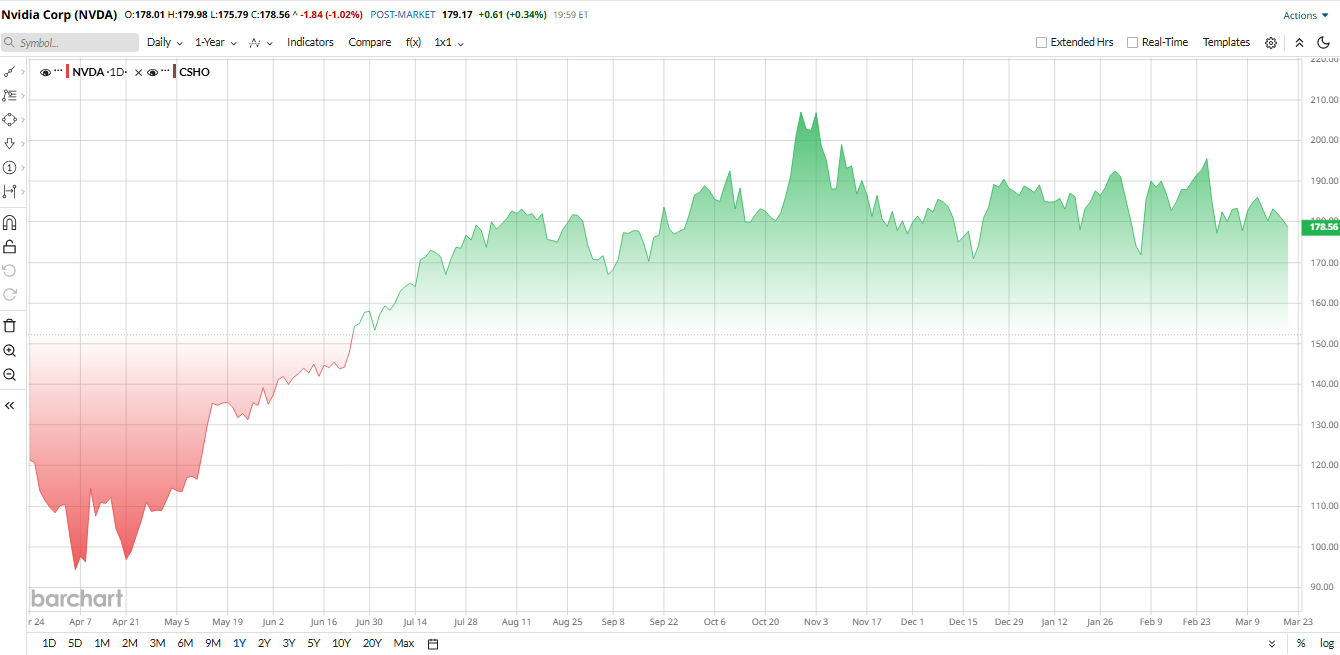

After having a solid year, Nvidia's stock is down roughly 6% year-to-date (YTD) in 2026. This slight dip comes despite a massive 48% gain over the past year. The muted start to the year is not linked to company weakness or fundamentals; it's just due to the broader tech sector pullback, even as the company delivered yet another quarter of jaw-dropping AI-driven growth

From a valuation standpoint, I see it as quite reasonable given the company's current growth. The PEG ratio sits at 0.55, well below the sector median of 0.66, meaning you're paying less for each unit of earnings growth. On the other hand, forward P/E is 21.9x, right in line with the sector median and offering a 50% discount relative to its own historical average. Moreover, with a 55.6% profit margin and 101.5% return on equity, I believe this is a high-quality business trading at a reasonable price.

Musk Praises Huang—What Happened?

On March 19, Elon Musk tweeted that he is a “huge admirer” of Nvidia and Jensen Huang and confirmed Tesla and SpaceX would keep buying Nvidia AI chips in big quantities. He emphasized Tesla’s own upcoming AI chips will be “optimized” for their robots and self-driving, but for now, Nvidia remains key. Wall Street interpreted this as a win-win: Musk’s praise is a great endorsement, and the news confirmed that two of the world’s most high-profile AI customers (Tesla and SpaceX) aren’t abandoning Nvidia anytime soon.

The market response, however, was modest. Nvidia shares dipped slightly following the announcement, as the overall tech sector was under pressure. Some analysts noted that Musk’s comments were more an affirmation of existing plans Tesla has already been a customer of than a surprising new development. Still, for investors who feared Tesla might shun external chips, Musk’s words were reassuring. The broader impact is that it helps dispel worry about losing big AI contracts. In essence, Musk’s thumbs-up has likely reinforced confidence in Nvidia’s business, even if it didn’t spark a huge rally.

Nvidia's Record Revenue, Still Accelerating

In Q4, Nvidia again smashed expectations and underscored why Musk is such a great admirer. Revenue surged to $68.13 billion in Q4, up 73% year-over-year (YoY), setting yet another record. The real engine was the data center business, which brought in $62.3 billion, jumping 75% from last year and 22% from the previous quarter. That segment alone now accounts for more than 90% of Nvidia’s total sales.

Profit growth was just as impressive. Net income climbed to $42.96 billion, up 94%, while adjusted earnings per share rose 82% to $1.62. The company also generated massive cash flow, with $34.9 billion in free cash flow during the quarter. Nvidia ended with roughly $62.6 billion in cash and investments, giving it enormous flexibility to invest in future growth.

Looking ahead, management expects Q1 revenue to hit around $78 billion, well above expectations. Gross margins are projected to stay strong at about 75%. CEO Jensen Huang emphasized that AI demand is still accelerating, calling it an industrial revolution. CFO Colette Kress echoed that sentiment, noting demand is coming from cloud providers, enterprises, and governments alike, with its latest Blackwell chips already fully booked.

Wall Street expects that momentum to continue. Analysts are projecting fiscal 2027 revenue of about $369 billion and earnings per share of $7.54. That’s a big jump from fiscal 2026, when Nvidia generated around $215.9 billion in revenue and $4.77 in earnings per share.

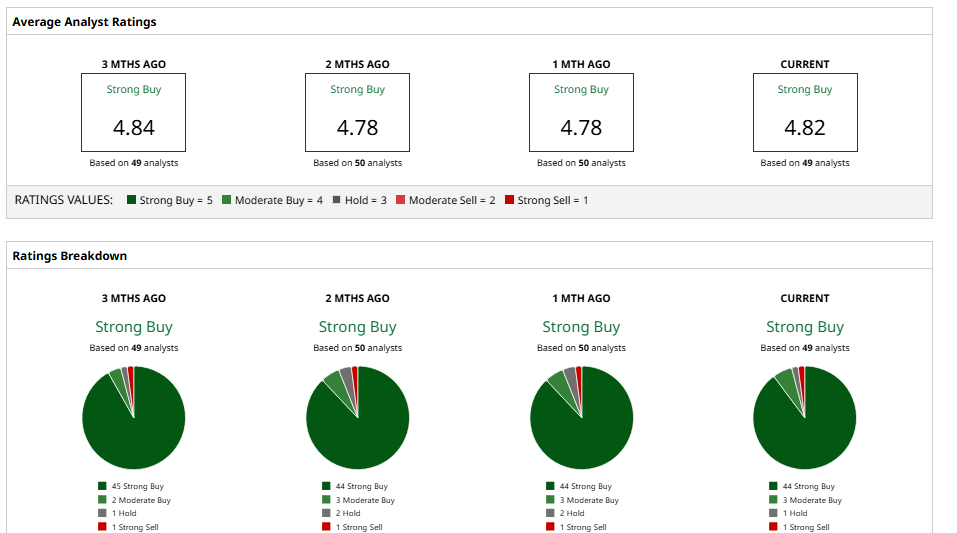

What Analysts Are Saying About NVDA Stock?

Analysts remain largely upbeat, though their target prices vary. Wedbush’s Matt Bryson recently reiterated his “Outperform” rating and actually raised his 12-month target to $300 from $230. He argued Nvidia’s long-term growth drivers, like hyperscale cloud builds and enterprise AI adoption, are “firmly intact.”

Goldman Sachs likewise reaffirmed its bullish stance with a “Buy” rating and a $250 target, raising its earnings forecasts by a couple of percent after Q4 and saying Nvidia’s guidance was very strong. Bank of America and Citigroup are especially bullish, each putting a $300 price target on the table, citing AI spending upside.

In contrast, a few firms are more cautious. For instance, J.P. Morgan’s target is around $265, noting Tesla’s entry into chips and macro risks.

But overall sentiment is clearly positive. Wall Street consensus rating on NVDA is “Strong Buy,” and the average 12-month price target is about $266, implying roughly 50% upside.

I think Wall Street still sees Nvidia as one of tech’s biggest winners, assuming the AI spending boom keeps rolling. As Morgan Stanley put it, concerns about loss of market share are “overblown,” and Nvidia’s “continued leadership” in AI should allow it to outperform.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)