/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

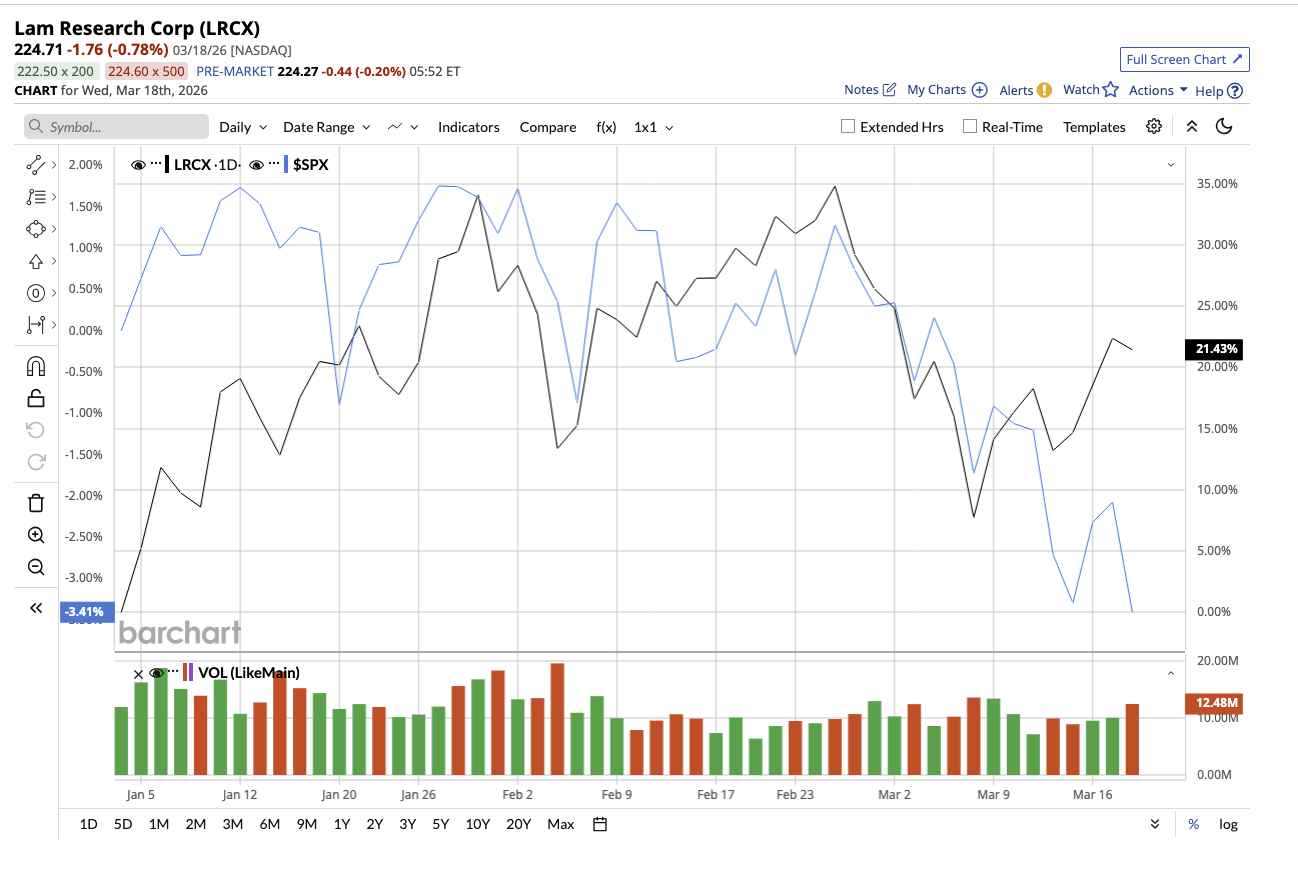

While much of the spotlight in the AI-driven market has gone to chip designers, a quieter player has been steadily climbing the charts. Lam Research (LRCX), a key supplier of semiconductor manufacturing equipment, has climbed about 33% year-to-date (YTD), wildly outperforming the S&P 500 Index's ($SPX) fall of 5%. Despite that strong performance, it still doesn’t receive the same attention as many high-profile semiconductor names

Lam Research may operate behind the scenes. But its role in the semiconductor ecosystem, especially in memory chips, puts it right at the center of one of the market’s most powerful growth trends. And Micron’s (MU) recent earnings help explain why LRCX stock continues to gain traction.

A Behind-the-Scenes Winner in the AI Boom

Lam Research operates at a critical layer of the semiconductor value chain. Instead of designing chips, it provides the equipment used to manufacture them, particularly tools for etching and deposition, which are critical in advanced chip production. Lam’s business is tied to memory manufacturers. That exposure is proving to be a major advantage right now, as memory — especially high-bandwidth memory (HBM) — has become central to AI infrastructure.

Lam’s revenue has grown at a healthy pace over the past five years, outperforming many peers. For full-year 2025, Lam reported 27% year-over-year (YOY) growth in revenue to $20.6 billion. The company has been translating top-line growth into even faster earnings expansion. Full-year EPS rose 49% YOY to $4.89, with a record gross margin of 49.9%. Lam continued its strong momentum for the most recent December quarter (Q2 of fiscal 2026). Revenue reached $5.34 billion, marking the 10th consecutive quarter of revenue growth.

Turning to its segment performance, foundry revenue accounted for 59% of systems revenue in the quarter, highlighting a shift toward foundry demand, fueled by leading-edge investments and continued spending in mature nodes, particularly in China. Meanwhile, memory revenue accounted for 34%. Within memory, DRAM strength stood out, supported by investments in HBM and node transitions. Notably, DRAM revenue went up to 23%, while NAND was 11%. Management emphasized that demand for advanced packaging, particularly in HBM, is soaring. Lam expects its advanced packaging business to expand over 40% in 2026, outpacing overall industry growth.

Here's where Micron comes in.

Micron’s Earnings Call Signals a Powerful Tailwind

Micron is a key customer for Lam Research. The company reported Q2 2026 earnings on March 18. Micron outlined an aggressive expansion plan, with capital expenditure likely to surpass $25 billion this fiscal year and be even higher in fiscal 2027. The majority of this is due to anticipated increases in equipment spending.

That's where Lam fits in. When memory manufacturers expand capacity, they don’t just build fabs. They also fill them with highly specialized tools such as etching and deposition equipment, supplied by companies like Lam Research. Micron also highlighted that DRAM and NAND markets remain constrained due to high demand and tight supply. This often forces chipmakers to invest even more aggressively in production capacity. Micron is also ramping up next-generation HBM production, which will increase equipment demand and help Lam Research.

In fact, industry projections show the HBM market alone could increase at a compound annual growth rate (CAGR) of 28.4% between 2025 and 2033 to reach $64.8 billion, emphasizing the need for continued infrastructure buildout.

A Growing Market With Structural Tailwinds

The semiconductor equipment market is expanding rapidly, and Lam is capturing a larger share. Management expects wafer fabrication equipment (WFE) spending to reach $110 billion in 2025 and $135 billion in 2026. Furthermore, Lam is also expanding its served available market (SAM) by aligning its portfolio with next-generation technologies. The company is advancing into DRAM manufacturing, leading-edge foundry logic, and NAND and storage. That said, investors should also keep in mind that the semiconductor sector is cyclical, where performance can fluctuate sharply.

Financially, Lam Research remains in a healthy position with the flexibility to repay upcoming debt maturities. At the end of the December quarter, it had cash and equivalents totalling $6.2 billion. It also returned 85% of free cash flow to shareholders through dividends and share buybacks. Lam expects to continue this trend of returning to shareholders.

Analysts expect Lam’s earnings to increase by 28% in fiscal 2026, followed by 30% growth in fiscal 2027. Currently, LRCX stock trades at 42.8 times forward earnings, reflecting investors’ enthusiasm for its long-term prospects.

What Does Wall Street Say About Lam Research Stock?

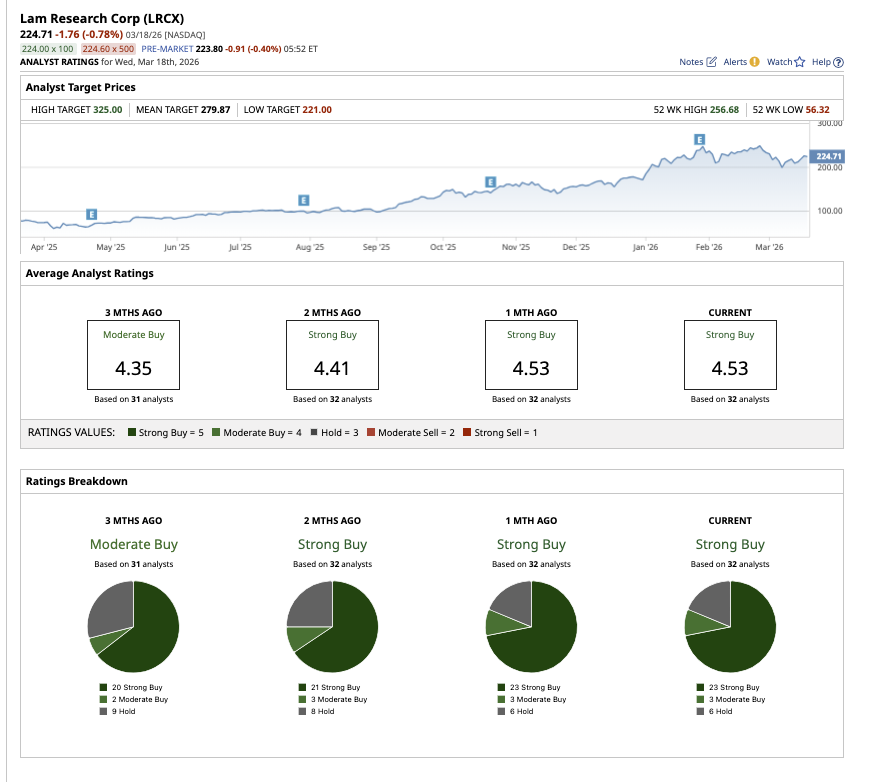

Wall Street has recognized Lam’s value, giving LRCX stock a consensus “Strong Buy” rating. Of the 32 analysts covering the stock, 23 offer a “Strong Buy" rating, three have a “Moderate Buy,” and six analysts offer a “Hold" rating.

LRCX stock's gain so far this year reflects that the company is benefiting from both cyclical recovery and structural development. Analysts believe the momentum will continue. Based on the average target price of $279.87, shares have potential upside of 23% from current levels. The Street-high estimate of $325 implies that shares can rally as much as 43% over the next 12 months.

The Bottom Line

While much of the market’s attention remains fixed on headline-grabbing stocks, Lam Research definitely deserves a second look. LRCX stock may not be the most talked-about AI stock, but the market is beginning to recognize its role. As the semiconductor industry ramps up investment to meet the demands of the AI era, Lam Research is positioned to thrive.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)