/Micron%20Technology%20Inc_logo%20and%20website-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)

Micron Technology's (MU) stellar fiscal second quarter has reignited bullish sentiment on Wall Street, with analysts rushing to raise their price targets. Strong AI-driven demand, tight memory supply, and expanding margins have put all of the limelight on Micron’s growth story, prompting Barclays to set a new high price estimate of $675.

Micron has had a massive run of more than 300% over the past year. Can MU stock continue its momentum and reach new highs?

New Price Upgrades for MU Stock

Valued at $500 billion by market capitalization, Micron is a semiconductor company that makes memory and storage chips. It has become a key player amid the growing demand for AI and cloud computing, with core products spanning DRAM, NAND and high-bandwidth memory (HBM), power data centers, AI systems, smartphones, PCs, cars, and industrial devices.

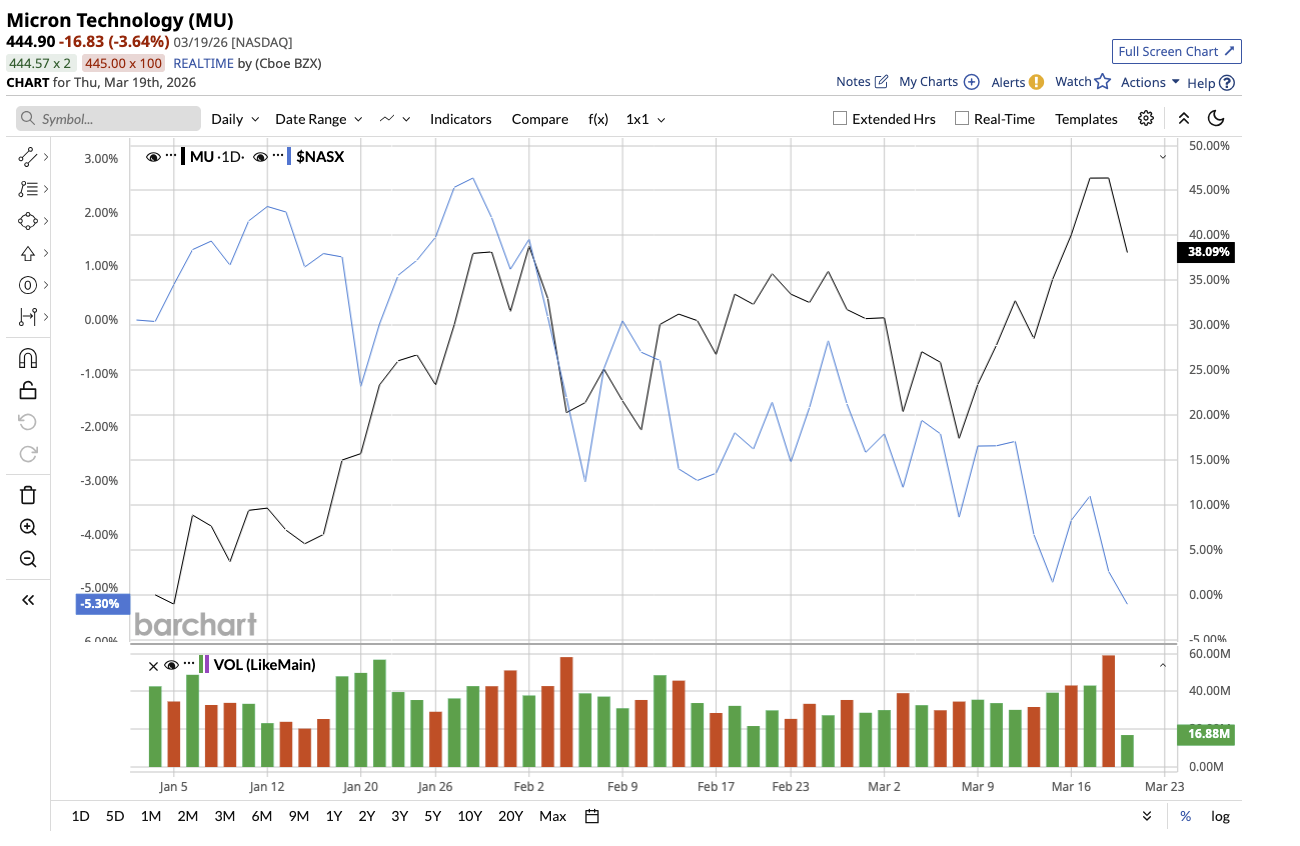

Despite a blowout quarter, MU stock is down 5% as of this writing, a reaction that often reflects market positioning rather than weakness in fundamentals. So far this year, the stock is up 46% — and if Barclays analyst Thomas O’Malley’s projections prove correct, MU stock could surge 60% from current levels.

Aside from Barclays, numerous other firms have boosted their price targets for this AI stock. KeyBanc and Rosenblatt Securities raised their price targets to $600 with “Buy” ratings. Separately, JPMorgan, Wedbush, Wells Fargo, TD Cowen, Deutsche Bank, and a few others increased their target prices to $550. Many other firms have followed suit.

AI Demand Reshapes the Memory Industry

The surge in analyst optimism is rooted in Micron’s extraordinary Q2 fiscal 2026 results. Total revenue climbed to $23.9 billion, up 196% year-over-year (YOY) and 75% over the first quarter. This marked Micron's fourth consecutive quarterly record of revenue growth. DRAM remained the primary growth engine, generating $18.8 billion in revenue and accounting for 79% of total sales. NAND also delivered a strong performance, with revenue reaching $5 billion.

Pricing played a critical role, reflecting tight industry supply and strong demand. DRAM prices surged in the mid-60% range, while NAND prices jumped to the high-70% range. According to management, the existing supply of DRAM and NAND is insufficient to meet AI and traditional server demand. The tight supply-demand dynamics are driving pricing power. Profitability surged alongside revenue. EPS came in at $12.20, up an eye-catching 682% YOY, reflecting the rapid rise of AI reshaping demand for memory and storage.

Micron’s HBM is its star product. The company has started volume shipments of its HBM4 36GB product and is scaling up production for next-generation AI platforms. These next-generation solutions are intended to satisfy the growing demands of AI workloads, which require increased performance and memory density.

During the Q2 earnings call, Micron made it clear that the current environment reflects tight supply and accelerating demand. Both DRAM and NAND markets remain constrained, while AI-driven workloads continue to push memory requirements higher. While the memory market is cyclical, Micron believes his demand-supply imbalance could persist beyond 2026. This means favorable pricing conditions and strong industry fundamentals could last longer, boosting the top and bottom line.

To meet this demand, Micron laid out an aggressive plan. Management expects capital expenditures to exceed $25 billion in fiscal 2026, with spending set to increase even further in fiscal 2027.

These investments include expanding its global manufacturing footprint through acquisition of a new DRAM facility, new fabs in the U.S., expansion projects in Japan, and a new NAND fab in Singapore. Micron has also begun shipments from a new assembly and test facility in India. As these facilities come online over the next several years, they will enable the company to capture a larger share of the growing memory market.

With a strong free cash flow balance of $6.9 billion, Micron announced a 30% raise in its quarterly dividend to $0.15 per share, showing confidence in its long-term growth and cash creation. At the same time, Micron remains committed to reinvesting in R&D and expanding capacity in order to sustain its competitive advantage.

Micron’s forward outlook further supports the bullish sentiment among analysts. For Q3 2026, the company expects revenue of approximately $33.5 billion, gross margin of around 81%, and EPS of about $19.15. Analysts expect earnings to increase by 599% in fiscal 2026, followed by 67% growth in fiscal 2027.

The Bottom Line on MU Stock

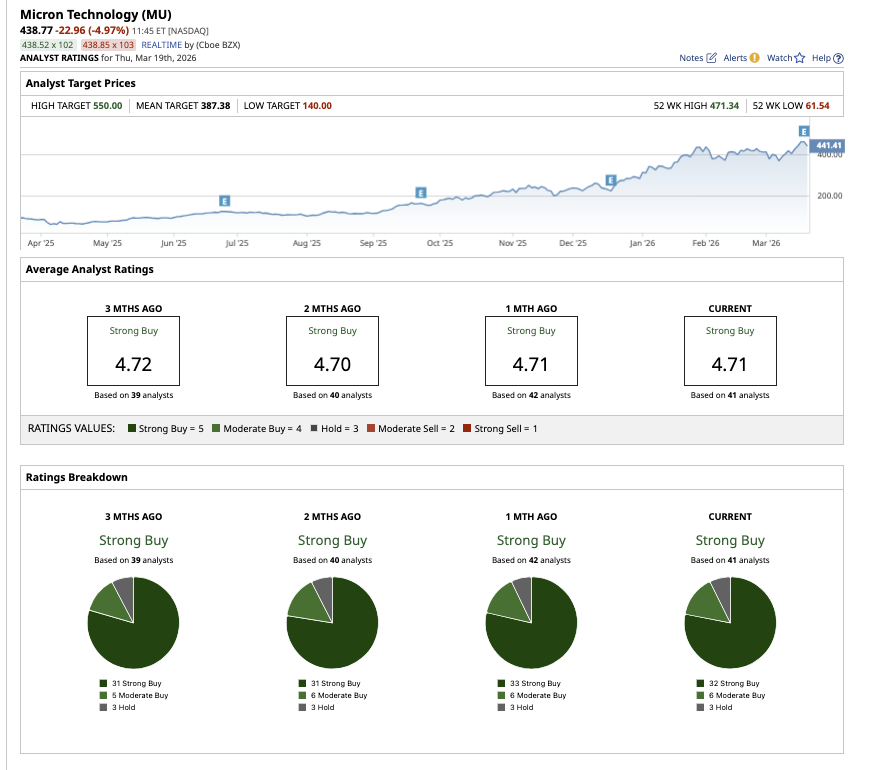

Overall, Wall Street rates MU stock as a consensus “Strong Buy.” Of the 41 analysts covering the stock, 31 rate it as a “Strong Buy,” six have a “Moderate Buy” rating, and four analysts offer a “Hold" rating.

With AI continuing to drive demand, supply remaining constrained, and execution firing across the board, Micron appears well positioned to maintain its current momentum. This explains why analysts are increasingly confident in the stock’s upside potential. While Micron’s surge this year might tempt investors to lock in profits, the opportunities ahead may be even greater.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)