The reports of inflation’s demise, at least if you’ve been listening to the White House, appear greatly exaggerated.

The S&P 500, Dow Jones Industrial Average, and Nasdaq Composite were all down more than 1% yesterday on fears that inflation was making a comeback, prompting the Federal Reserve to leave its key interest rate unchanged.

“A new set of economic forecasts showed that Fed officials are now expecting the central bank’s preferred PCE inflation rate will end the year at 2.7 per cent, above the 2.4 per cent they predicted in December. That would be well above the Fed’s 2 per cent inflation target,” Financial Times reported.

The good news is that Fed Chairman Jerome Powell did say that the economic and inflationary conditions we face today are much better than the ones in the 1970s, which coined the term “stagflation,” the combination of stagnant economic growth and excessive inflation.

In yesterday’s options trading, volume was lower than usual, at 49.09 million, considerably less than the 90-day average of 58.69 million.

Despite the lower options volume, there were plenty of unusually active options, especially the top three by Vol/OI (volume-to-open-interest) ratios.

Here’s what I might have done with each of them.

The Unusually Active Options in Question

As you can see above, the Microchip Technology (MCHP) June 18 call stands out from the four others, with a massive Vol/OI ratio of 608.78, eight times the second-place Pfizer (PFE) put option.

It’s important to note that I exclude options expiring in less than seven days. That’s just a personal preference; 0DTEs (days to expiration) in the hands of expert traders isn’t a problem.

You’ll notice that the three stocks are relatively diversified, representing three different sectors, with market caps ranging from Invesco’s (IVZ) $10 billion to Pfizer’s $155 billion. You’ve also got two calls and one put; that’s about the same as the 60/40 calls/puts split for the entire options market yesterday.

Let’s dig into the three.

Microchip Technology (MCHP)

As I said earlier, its June 18 $55 call had a massive Vol/OI ratio with 70,010 in volume against an open interest of just 115. Somebody was busy. I’m not too familiar with the chip stock. Its performance over the past year (up 19%) and over the past five years (down 14%) is nothing to write home about. Analog Devices (ADI) is one of its competitors; it’s up 47% and 103% over the same period.

Back to the 70.010 volume for the $55 call. All but 10 contracts were from one trade at 3:13 p.m. ET yesterday. The trade price of $13.80 was almost halfway between the bid price and ask price. That’s a mildly bullish to neutral signal.

The Barchart Technical Opinion for MCHP stock is a Weak Sell with a 24% likelihood of maintaining its current direction -- it’s down 18% in the past month -- so the buyer of the call could anticipate that the share price will reverse course and retest the 52-week high of $83.35 hit on Feb. 12.

Going long the 70,000 $55 calls would cost the buyer $96.6 million, or 21.3% of its $64.71 closing price. That’s a nice use of leverage. Based on the 0.7519 delta, the value of the call increases by 75 cents for every $1 move in the share price. So, if the share price appreciates by $18.35 (28.4%) in the next 92 days, the buyer would double their money.

Given the expected move by June 18 is just $10.92 (16.88%), the likelihood of doubling your money is low. However, the shares only need to appreciate by $4.09 (6.3%) over the next three months to break even.

From where I sit, this long call trade makes considerable sense.

Pfizer (PFE)

Pfizer was in second spot yesterday with a Vol/OI ratio of 75.96. The May 15 $24 put’s 41,168 volume was about 27% pf the day's overall volume, which itself was 1.4 times its 30-day average.

For a change, Pfizer stock is outperforming the S&P 500, up nearly 10% in 2026, while the index is down more than 3%. Large-cap healthcare stocks like Pfizer have not done well in recent years -- PFE is down 56% from its all-time high of $61.71 in December 2021 when it was raking in the cash from COVID -- but its share price appears to have bottomed, and it’s slowly moving toward its 200-day moving average as the chart below shows.

On Jan. 9, I wrote about how Pfizer’s March 20 $29 put had the highest Vol/OI ratio from the previous day’s trading, something you rarely see from PFE. That brought to mind two options strategies: the Long Straddle and the Bull Put Spread.

The long straddle expects a big move in either direction by expiration. It is bullish about volatility increasing but neutral on the stock itself. It involves buying a call and a put option at identical strike prices. In this case, that’s the $24 call ITM (in-the-money) and $24 put OTM (out-of-the-money).

The cost of the long straddle, or net debit, would be $5.20 [$4.90 call ask price + $0.30 put ask price]. That’s also your maximum loss. Your net debit is 19.0% of Pfizer’s closing price of $27.32 from yesterday. Your breakeven on the upside is $29.20, and on the downside, it is $18.80.

The expected move by May 15 is $2.26 (8.28%). So, if you were to make money on the trade, it would most likely be on the upside, given its share price only needs to appreciate by $1.88 in the next 58 days to be above breakeven.

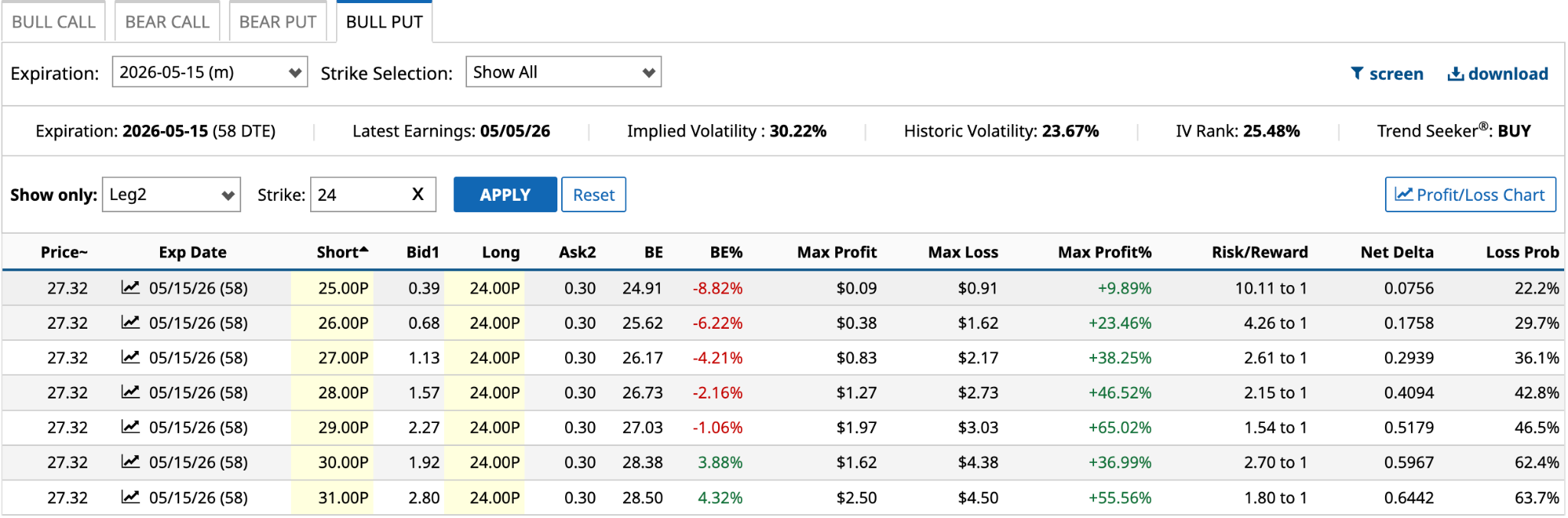

The bull put spread is bullish. You expect Pfizer’s share price to increase in value by expiration. It involves selling a put option and buying another at a lower strike price.

So, based on yesterday’s unusually active $24 put, it would be the lower-priced strike, and you would buy that and go long, while selling one of the seven put strikes short. In each case, you would generate a net credit rather than a net debit.

Your maximum loss would depend on which put you choose. For example, let’s say you sell the $25 put. Your net credit is $0.09. Your net loss is $0.91 [$25 strike price - $24 strike price - $0.09]. Your maximum profit is $0.09, or your net credit.

While the bull put spread is bullish, the upside and downside risks are defined before you make the trade, which makes it attractive for risk-averse investors. However, I’d probably go with a higher short put strike price, say $28, where the risk/reward ratio is more in your favor.

With eight trading days to expiration after Pfizer reports earnings on May 5, I’d be inclined to go with the long straddle over the bull put spread because a positive report is sure to push the share price over $29.20 by May 15.

Invesco (IVZ)

The asset manager’s April 17 $28 call had the third-highest Vol/OI ratio yesterday at 57.13. The volume of 25,021 for the $28 call was 4.5 times the 30-day average, accounting for 99% of Invesco’s options volume.

Here are the two trades that accounted for all but 268 contracts traded on Invesco options yesterday.

As you can see, the trades occurred at different prices--$0.10 and $0.15. Why is this? There are several reasons, but the most likely was that an institutional investor was looking to avoid attention as it went long on calls to buy 25,000 Invesco shares at $28, nearly 20% ITM.

As you can see, the trades occurred at different prices--$0.10 and $0.15. Why is this? There are several reasons, but the most likely was that an institutional investor was looking to avoid attention as it went long on calls to buy 25,000 Invesco shares at $28, nearly 20% ITM.

In this instance, Invesco reports earnings on April 28, after the $28 calls expire. The investor likely expects the shares to move higher leading up to earnings. Should this happen, it could roll the 25,000 calls, pushing out the expiration date, before selling them for profits, or exercising the right to buy the shares and holding them for the long term.

So, the most obvious options strategy in this instance appears to be long the calls. You could also do a bull call spread or a Long Strangle, but in this instance, the long call appears to be the play.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)

/A%20logo%20for%20Bending%20Spoons%20displayed%20on%20a%20smartphone%20screen%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/ServiceNow%20Inc%20building%20in%20Silicon%20Valley-by%20Sundry%20Photography%20via%20iStock.jpg)