/Akamai%20Technologies%20Inc%20logo%20on%20building-by%20Sundry%20Photography%20via%20Shutterstock.jpg)

Cambridge, Massachusetts-based Akamai Technologies, Inc. (AKAM) provides security, delivery, and cloud computing solutions in the United States and internationally. With a market cap of $15.8 billion, the company offers security solutions, including application and application programming interfaces (API) protection solution, Bot & Abuse portfolio, full account lifecycle protection, and more.

Companies valued more than $10 billion are generally classified as “large-cap” stocks, and Akamai Technologies fits this criterion perfectly. AKAM fits right into that category, with its market cap exceeding this threshold, reflecting its substantial size and influence in the software infrastructure industry.

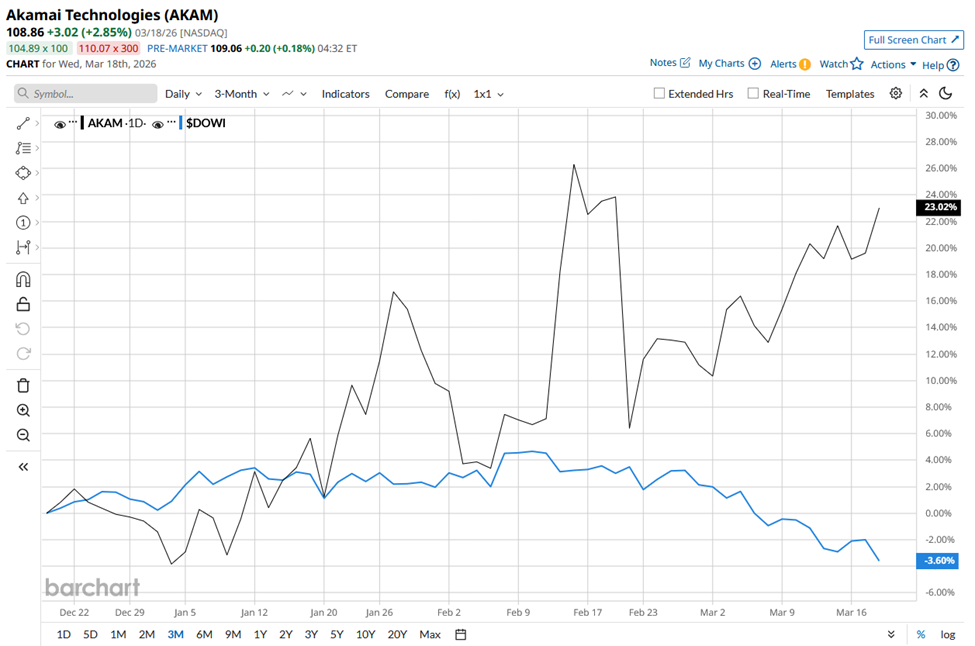

AKAM stock is down nearly 4% from its 52-week high of $113.50, reached on Feb. 13. Shares of Akamai have surged 22.2% over the past three months, outperforming the Dow Jones Industrials Average’s ($DOWI) 4.4% decline during the same period.

Over the past 52 weeks, the stock has surged 32.3%, outpacing DOWI’s 9.7% gain.

The stock has been trading above its 200-day and 50-day moving averages since November 2025.

Akamai Technologies has outperformed due to strong profitability, consistent growth, and the expansion of higher-margin security and cloud businesses beyond its legacy CDN operations.

The company reported strong Q4 2025 results on Feb. 19 with revenue rising 7% to $1.095 billion, adjusted EPS of $1.84 beating estimates, and high-growth segments like Cloud Infrastructure Services up 45% and security revenue up 11%. However, the stock tumbled 14.1% the next day as investors focused on weak 2026 guidance, with Q1 2026 EPS expected at $1.50 - $1.67 and full-year EPS guidance of $6.20 - $7.20, both below the consensus. The decline was further pressured by EPS falling 36% and net income dropping 39% in Q4.

In comparison, rival Okta, Inc. (OKTA) has lagged behind AKAM stock. OKTA stock has declined 6.2% on a YTD basis and 28.9% over the past year.

Despite the stock’s outperformance, analysts remain cautiously optimistic on its prospects. Among the 22 analysts covering the stock, the consensus rating is a “Moderate Buy.” Its mean price target of $109.10 suggests marginal upside potential from current price levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/McDonald's%20Corp%20arches%20by-%20TonyBaggett%20via%20iStock.jpg)