/Advanced%20Micro%20Devices%20Inc_%20office%20sign-by%20Poetra_RH%20via%20Shutterstock.jpg)

Shares of Advanced Micro Devices (AMD) have delivered a strong performance over the past year, significantly outperforming competitor Nvidia (NVDA). Indeed, AMD stock has climbed 95% over the last 12 months, compared to a gain of around 50% for NVDA stock. Despite this impressive rally, however, AMD has cooled in 2026 and now trades about 26% below its 52-week high.

While the stock has cooled off a bit, AMD's underlying business fundamentals remain solid. Strong demand for the company’s server central processing units (CPUs) and Instinct graphics processing units (GPUs) continues to support growth. AMD has steadily strengthened its position in the high-performance computing market, with its data center segment growing rapidly and positioning the firm to deliver solid growth. Rising capital investment by enterprise and cloud customers in advanced computing infrastructure is expected to further sustain demand for AMD's data center solutions.

Momentum is also evident across the company's broader product portfolio. AMD is seeing accelerating demand across several major markets, including data centers, personal computers, gaming, and embedded systems. The company has captured meaningful market share in both server and PC processors while rapidly expanding its data center AI business. This growth has been supported by increasing adoption of its Instinct GPUs and software platform among cloud providers, enterprises, and AI developers.

Factors Support a Rally in AMD

Strong demand trends, an expanding product portfolio, and an improving valuation indicate that AMD stock is poised for a significant rebound. Supporting AMD’s growth is its rapidly expanding data center business. The segment is benefiting from rising demand for high-performance computing and AI workloads.

In the fourth quarter of 2025, the data center segment generated $5.4 billion in revenue, representing a 39% year-over-year (YOY) increase. Much of this growth was driven by the launch of the AMD Instinct MI350 Series GPUs, which helped drive a noticeable rise in data center sales.

Supporting the segment’s growth are server processors. Adoption of AMD’s fifth-generation EPYC CPUs accelerated significantly, accounting for “more than half of the total server revenue.” This growing uptake highlights the increasing competitiveness of AMD’s server offerings.

Looking ahead, the momentum is likely to sustain. Hyperscalers and cloud service providers are aggressively expanding data centers, driving demand for AMD's chips. In addition, enterprises are modernizing aging data center infrastructure. This trend further supports demand for the company's EPYC processors, which have been gradually capturing market share from competitors.

The strength of AMD’s EPYC server processors and Instinct accelerator roadmap indicates that the company could sustain rapid expansion in its data center segment for several years. AMD projects data center revenue to grow at a compound annual growth rate (CAGR) of over 60% over the next three to five years. Within that segment, the AI-focused portion of the business may grow even faster as demand for next-generation Instinct systems and AI platforms rises sharply.

AMD’s broader financial outlook remains robust. The company expects total revenue to grow at a rate above 35% annually over the next three to five years, while operating margins expand and earnings increase substantially.

Strategic partnerships are also strengthening the chip firm’s competitive position in the AI ecosystem. One notable development is the company’s expanded multi-year agreement with Meta Platforms (META). For AMD, the deal could meaningfully contribute to long-term revenue growth and support EPS expansion.

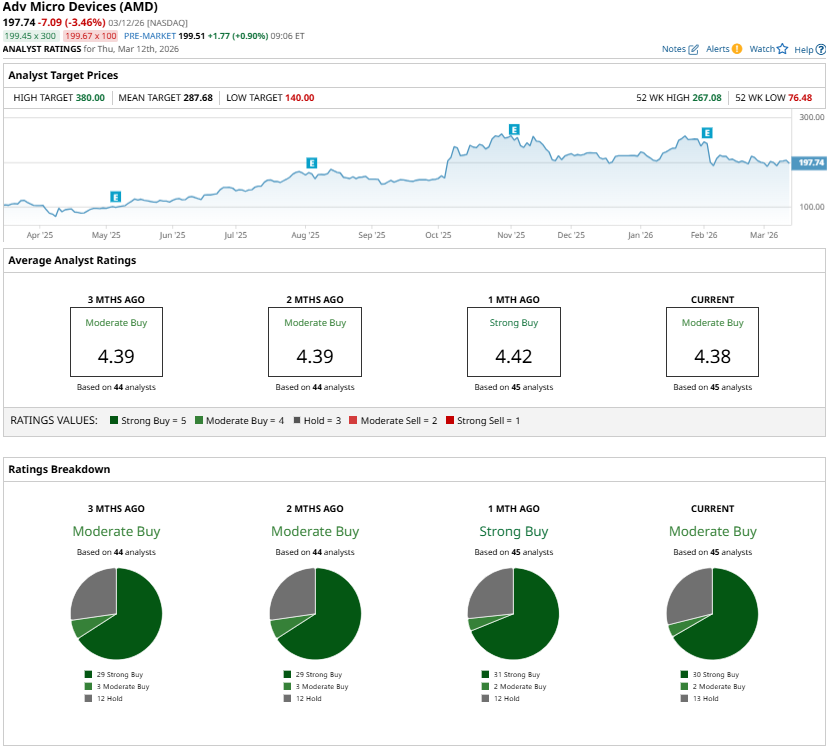

What Do Analysts Think of AMD Stock?

While AMD is set to grow rapidly, its valuation supports the bullish thesis. AMD currently trades at a forward price-to-earnings (P/E) ratio of around 34 times. When compared with expected earnings expansion — estimated at roughly 72% in 2026 and about 60% in 2027 — the valuation appears relatively attractive.

Analysts maintain a “Moderate Buy” consensus rating on AMD stock. Meanwhile, the average price target of $287.68 suggests significant potential upside of 46% over the next 12 months.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)