/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

Chinese e-commerce and cloud giant Alibaba Group Holding Limited (BABA) is scheduled to release its financial results for the third quarter ended Dec. 31, 2025, before the market opens on March 19.

The update could mark a pivotal moment for investors, offering fresh insight into Alibaba’s core e-commerce momentum, cloud computing growth, and artificial intelligence (AI) investments, all key drivers shaping the company’s long-term strategy and the outlook for its stock.

About Alibaba Group Stock

Chinese multinational technology conglomerate Alibaba Groupt is best known for its dominance in e-commerce (Alibaba.com, Taobao, Tmall), cloud computing, digital media, logistics, and financial services. Headquartered in Hangzhou, China, the company operates a sprawling ecosystem that serves consumers, merchants, and enterprises globally. Alibaba has a market cap of around $316.7 billion.

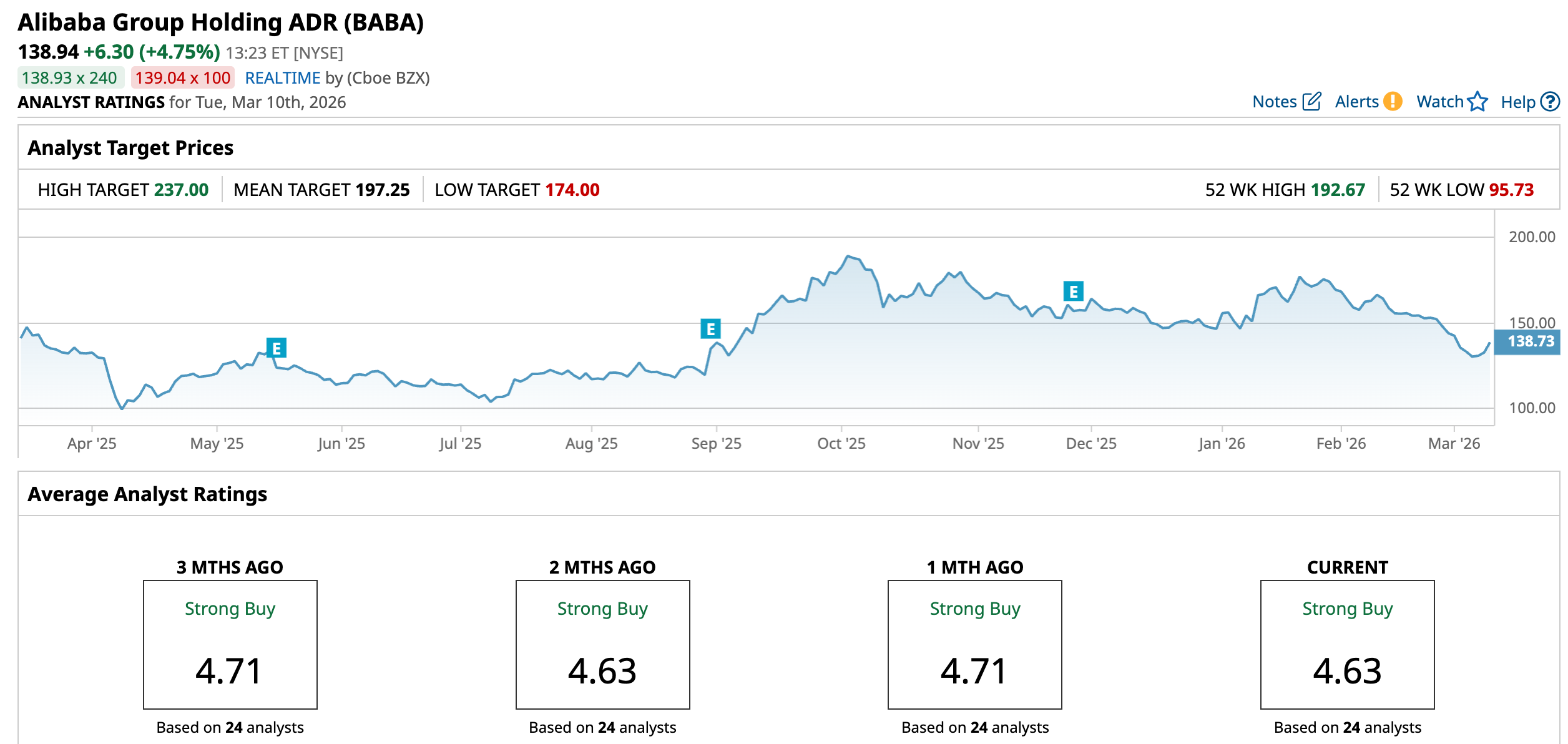

Shares of Alibaba Group have pulled back in recent weeks, reflecting a shift in investor sentiment. The stock closed the last session at $138.38, well below its 52-week high of $192.67 reached in October 2025. Over the past year, the stock is up 4.03%.

Yet, BABA has declined 5.94% year-to-date (YTD) with the selling pressure even more pronounced over the past month, with 17.2% plunge.

The recent weakness reflects several factors weighing on investor sentiment. Concerns about China’s slowing economic recovery and softer consumer spending have raised questions about the outlook for Alibaba’s core e-commerce business. At the same time, investors have become more cautious ahead of the company’s upcoming earnings report, while ongoing competition in China’s online retail and cloud markets has also contributed to volatility in the stock.

Despite the slump, the stock is trading at a lofty valuation compared to its industry peers at 24.72 times forward earnings.

Mixed Financial Performance

Alibaba Group released its fiscal 2026 second-quarter results on Nov. 25, 2025, reporting solid revenue growth but significantly lower profitability.

For the quarter ended Sept. 30, 2025, Alibaba generated revenue of RMB 247.8 billion ($34.8 billion), representing a 5% year-over-year (YOY) increase. On a comparable basis, excluding the divested Sun Art and Intime businesses, revenue growth would have been roughly 15% YOY, highlighting stronger underlying demand across key segments.

However, profitability declined sharply due to heavy investments. Non-GAAP earnings were RMB 4.36 per ADS, down 71% YOY and below consensus estimates. Its net income fell 53% YOY to about RMB 20.6 billion, reflecting higher marketing costs and strategic spending.

Alibaba’s China e-commerce business remained the largest revenue contributor. The segment generated RMB 132.6 billion ($18.6 billion) in revenue, representing 16% YOY growth, supported by improved monetization and stronger adoption of AI-powered marketing tools by merchants.

The Cloud Intelligence Group was the fastest-growing major segment. Cloud revenue increased 34% YOY to roughly RMB 39.8 billion ($5.6 billion), fueled by surging demand for AI computing and LLM services. Also, management noted that AI-related products have been expanding rapidly, with triple-digit growth for multiple consecutive quarters.

Further, Alibaba’s quick-commerce and instant retail initiatives delivered strong growth. Revenue from the quick-commerce unit surged about 60% YOY, as the company invested aggressively in faster delivery services to compete with rivals.

However, operating cash flow came in at RMB 10.1 billion ($1.4 billion), down 68% from the prior-year quarter. Free cash flow recorded an outflow of about RMB 21.8 billion ($3 billion), reflecting large capital investments.

Management reiterated that AI and cloud computing will remain the company’s primary long-term growth engines. The company plans to continue investing heavily in AI infrastructure, cloud computing capacity, and quick-commerce logistics, even if it temporarily pressures margins.

For the Dec. ended quarterly report, about to be released on Mar. 19, the consensus EPS estimate of $1.73 suggests a decrease of 37.6% YOY. Analysts expect the company’s EPS to decline 36% YOY to $5.29 in fiscal 2026 and improve 51.4% to $8.01 in fiscal 2027.

What Do Analysts Expect for Alibaba Stock?

Recently, Goldman Sachs upgraded Alibaba Group to “Conviction Buy” and set a $186 price target. The firm expects Alibaba’s EPS to grow 31% in fiscal 2027 and 36% in fiscal 2028, driven by stronger AI and cloud demand and a recovery in China’s e-commerce profits.

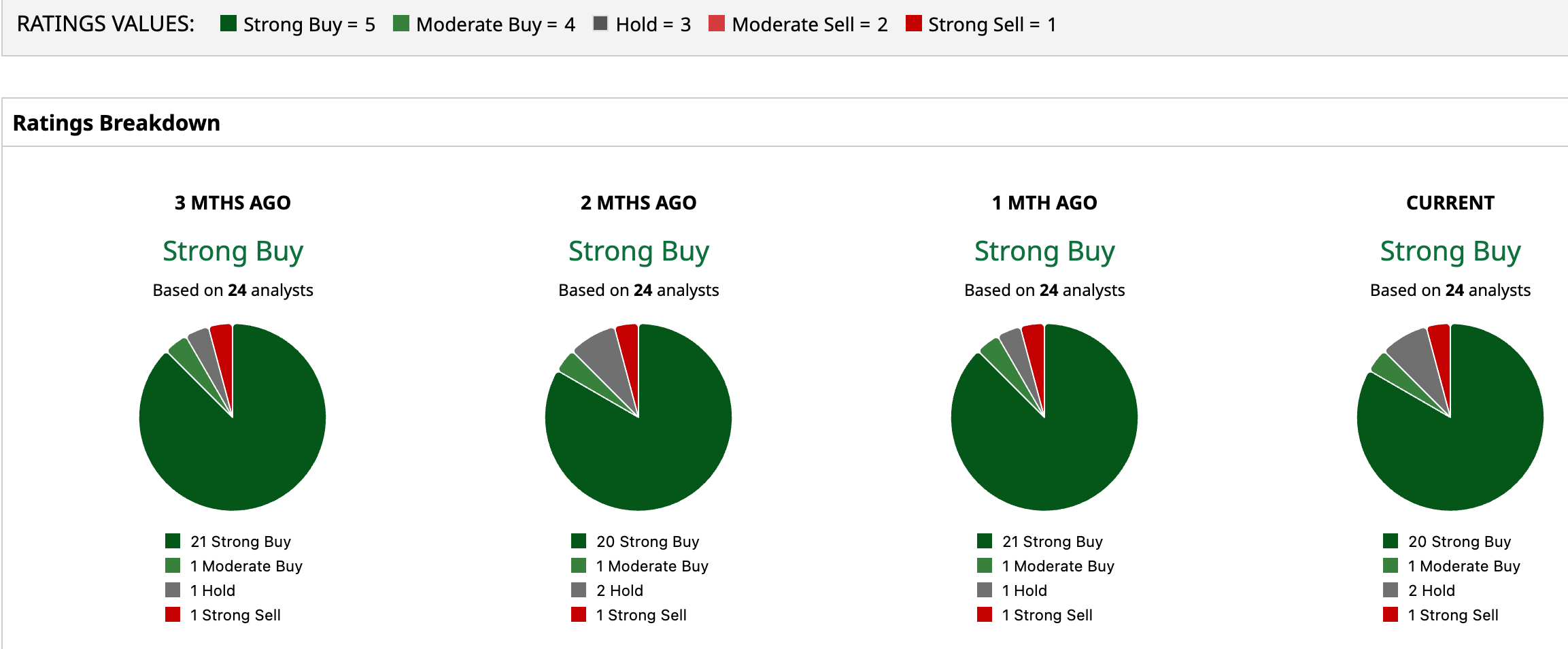

Overall, Alibaba has a consensus “Strong Buy” rating. Of the 24 analysts covering the stock, 20 advise a “Strong Buy,” one suggests a “Moderate Buy,” two recommend a “Hold,” and the remaining one analyst gives a “Strong Sell” rating.

The average analyst price target for BABA is $197.25, indicating a potential upside of almost 42%. The Street-high target price of $237 suggests that the stock could rally as much as 70.6%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)