/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

After a strong rally, shares of Palantir (PLTR) have come under pressure in late 2025 and early 2026. The stock has retreated from its record highs due to concerns about extremely high valuations, profit-taking following the earlier surge, and a broader rotation within the technology sector. This shift has seen capital move away from software companies as markets increasingly focus on the rapid emergence of AI agents. As a result, PLTR shares have declined roughly 25% from their 52-week high.

While PLTR stock has lost steam, several underlying fundamentals continue to support the company’s outlook. Demand for Palantir’s data analytics and AI platform (AIP) remains strong, while expanding profit margins indicate improving operational efficiency. At the same time, the recent pullback has helped ease some of the valuation pressures that previously concerned investors.

Geopolitical developments may provide another potential catalyst for the company. Rising instability in the Middle East could increase demand for advanced analytics and AI capabilities across government and defense sectors. Given Palantir’s established presence in government software and data intelligence systems, heightened defense and security spending could translate into stronger government revenue over time.

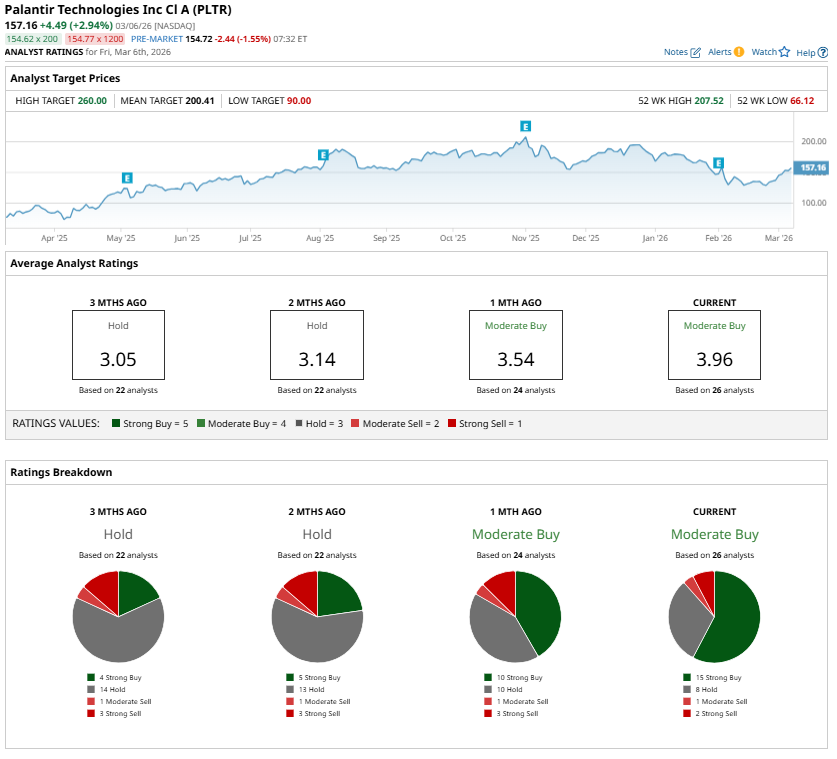

These factors could limit the likelihood of a significant downside move and suggest that PLTR stock has meaningful upside potential. The Street’s highest price target for PLTR stock is $260, implying more than 65% upside from its recent close of $157.16.

Strong Demand Supports PLTR’s Investment Case

Strong demand continues to strengthen the investment case for Palantir, and the company projects another year of accelerated growth. Management has guided for revenue between $7.182 billion and $7.198 billion, with the midpoint of $7.19 billion representing approximately 61% year-over-year (YoY) growth. This outlook implies acceleration from the 56% growth recorded in 2025, suggesting that the overall demand environment for the company’s AI platform remains exceptionally solid.

The strong adoption of Palantir’s AIP will continue to drive growth across the company’s U.S. operations. In the fourth quarter, the U.S. business grew 93% YoY and 22% sequentially. Within that segment, U.S. commercial revenue increased 137% YoY and 28% sequentially. This follows a sustained period of rapid expansion, with the segment posting 121% YoY growth in the third quarter and 93% in the second quarter.

AIP’s ability to rapidly move customers from initial engagement to measurable outcomes has been a key catalyst. Organizations are progressing from experimentation to full-scale deployments much faster than before. As a result, existing customers are increasing their spending while new clients are entering the ecosystem with larger initial contracts.

This trend is reflected in Palantir’s contract activity. The company recently reported its highest quarterly total contract value on record at $4.3 billion. Revenue concentration among its largest clients is also expanding. Over the past twelve months, revenue generated from the company’s top 20 customers increased 45% YoY, reaching an average of $94 million per customer.

This strong commercial demand is expected to translate into another year of solid growth. Palantir projects that its U.S. commercial revenue will exceed $3.144 billion in 2026, implying growth of at least 115%. For context, the segment delivered 109% YoY growth in 2025, generating $1.465 billion in revenue. Such expansion suggests that adoption of AIP is still in its early stages.

Government contracts remain another catalyst for the company. Palantir’s U.S. government business expanded 66% YoY and 17% sequentially in the fourth quarter, supported by increased adoption within defense and civil agencies. As geopolitical tensions intensify globally, spending on AI-enabled intelligence, logistics, and analytics platforms is expected to remain a priority for government agencies, supporting Palantir’s growth.

At the same time, profitability continues to improve. Palantir generated $798 million in adjusted operating income in the fourth quarter, representing a 57% margin, up from 45% a year earlier. Management expects adjusted operating income to reach between $4.126 billion and $4.142 billion in 2026, a substantial increase from $2.254 billion in 2025.

In short, strong demand, accelerating revenue growth, and expanding margins indicate solid growth ahead for Palantir, which will support the rally in PLTR stock.

What’s Next for PLTR Stock?

The rapid adoption of its AIP, accelerating commercial growth in the U.S., expanding government contracts, and improving operating margins all point to sustained business momentum. This suggests PLTR stock could recover.

That said, the stock still trades at a premium multiple relative to traditional software peers. This implies that achieving a $260 price target would require consistent acceleration in growth rate and major government contract wins.

Analysts maintain a “Moderate Buy” consensus rating on PLTR stock.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.