/Nasdaq%20Inc%20NY%20building-by%20hapabapa%20via%20iStock.jpg)

The worst of the war-related market turmoil may be over. Setting a buy-in target for Nasdaq, Inc. (NDAQ) stock may be worthwhile. One play is to short out-of-the-money (OTM) NDAQ puts for one-month expiry. Another is to buy in-the-money NDAQ calls for longer periods.

Today it's trading at $88.17, up from a Feb. 12 trough of $79.01, well before the recent drop from the Iran war. But it could have much more to go. I discussed this in a Feb. 10 Barchart article.

The article discussed price targets for NDAQ stock and a short-put play (“Nasdaq, Inc. Stock Is Off Its Highs, Despite Strong Results - Short Put Plays Work Here”).

So, how has this worked out? And, what NDAQ play is best now?

Higher Price Targets (PTs)

I wrote that NDAQ was worth $95.95 per share, based on its strong free cash flow (FCF) and FCF margins. That is 8.8% higher than today's price.

Moreover, other analysts had higher price targets (PTs). For example, Yahoo! Finance reports 17 analysts have an average PT of $108.53. In fact, Barchart's mean analyst survey has a $111.88 PT.

These PTs are +23% and 27% higher than today's price. Even AnaChart's survey, which covers recent analyst write-ups, shows higher prices. It shows a $98.97 average PT from 13 analysts, or +12% upside potential.

That shows it makes sense to take advantage of this low NDAQ price. One way to do this is to sell short out-of-the-money (OTM) puts to set a lower potential buy-in point. That way, an investor can get paid while waiting for this lower buy-in.

Shorting OTM NDAQ Puts

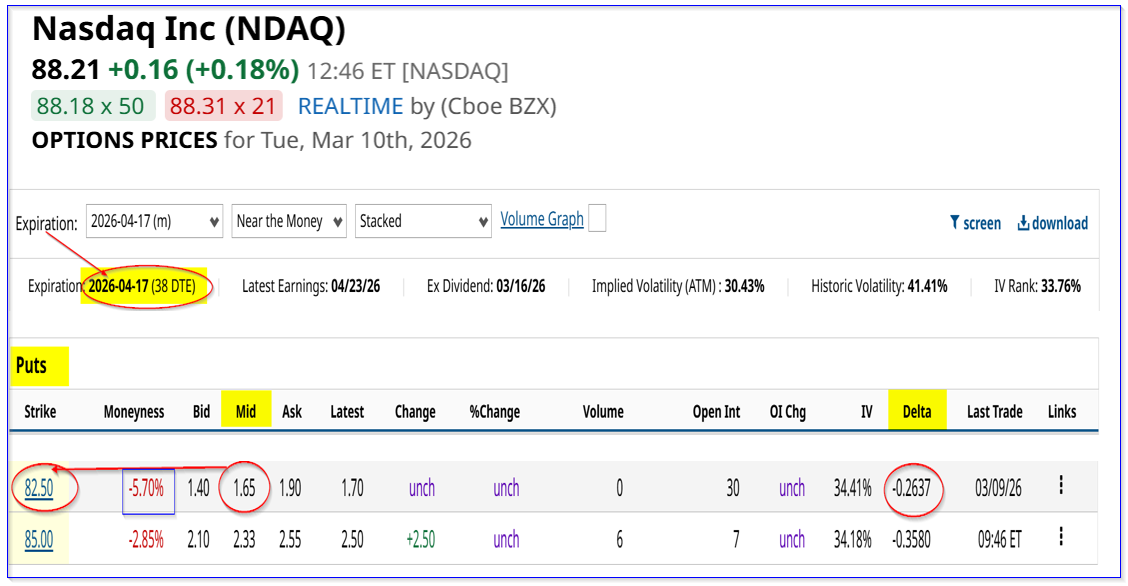

A month ago, I discussed shorting the $80.00 strike price put option that expires on March 20. At the time, the premium received was $1.60, for a 2.0% yield (i.e., $1.60/$80.00) over the next 38 days.

Today, that $80 put strike price premium is down to just 43 cents at the midpoint. That means much of the short-put play income has already been earned. It will expire worthless if NDAQ stays over $80 by March 20.

It makes sense to roll this play over (i.e., “Buy to Close”) and do a new short-put play. For example, the April 17, 2026, expiry period shows that the $82.50 strike price put contract has a midpoint premium of $1.65.

This gives a short-seller of this put contract a one-month yield of 2.0% (i.e., $1.65/$82.50 = 0.02), just like last month's $80.00 short-put play.

And this strike price is still -6.47% lowqr than today's price. Moreover, it offers a lower potential breakeven point, if NDAQ falls to $82.50 by April 10:

$82.50 - $1.65 = $80.85 B/E

That's -8.3% lower than today's price. So, it provides a great potential buy-in point for value investors.

However, what if NDAQ rises to our lower PT? Shorting puts doesn't provide any upside. One way around this is to use short-put play income over the next 6 months to buy in-the-money (ITM) calls.

Buying ITM NDAQ Calls

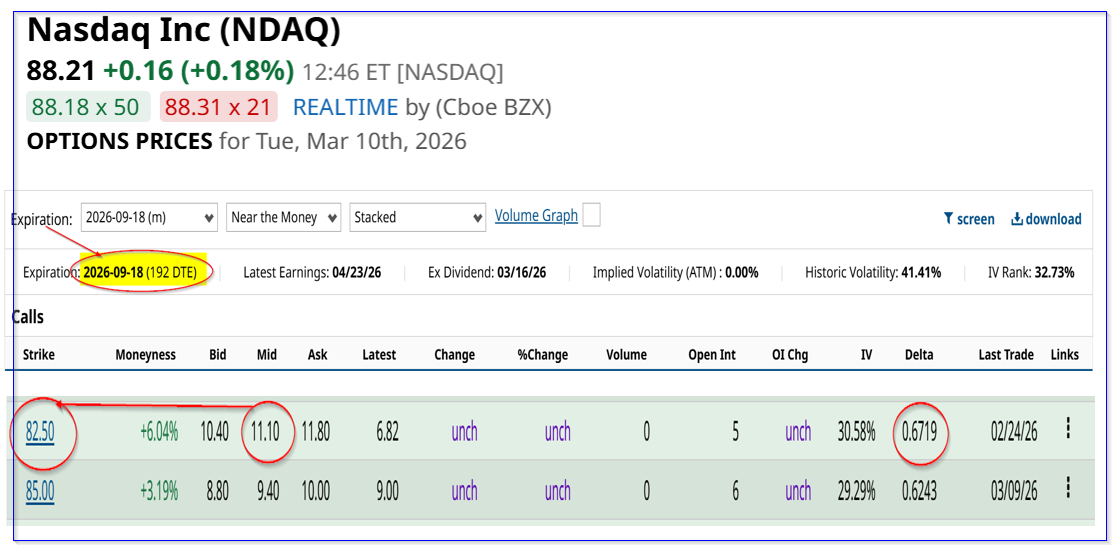

For example, look at the Sept. 18, 2026, expiry period, over 6 months or 192 days to expiry (DTE). It shows that the $82.50 call option has an attractive midpoint premium cost of $11.10.

That means that an investor who continues to short OTM puts each month for six months could potentially pay for most of this call option:

$1.65 x 6 = $9.90 put income

$11.10 - $9.90 = $1.20 net cost

That implies that an investor's cost to buy 100 NDAQ shares (assuming the call option is exercised) would be just $83.70 (i.e., $82.50 +$1.20).

Potential Returns

Here is what that could help an investor. Let's compare a 100 share purchase today vs. this mixed 6-month OTM short-put/ITM call purchase play.

If NDAQ rises to $100 by Sept. 18, the long-share buyer would make the following return:

Cost: 100 shs x $88.21 = $8,821

Return: $100 x 100 shs = $10,000

$10,000 - $8,821 = $1,179

ROI: $1,179 /$8,821 = +13.37%

However, consider the alternative:

Cost: $8,370 (mixed cost of short-put play and call option buy-in - $83.70 x 100)

Return: $10,000 - $8,370 = $1,629

ROI: $1,629 / $8,250 = +19.75%

The ROI is significantly higher over the six month period.

This is due to the lower cost of shorting $82.50 put contracts each month and eventually buying in at this lower in-the-money (ITM) cost of $82.50.

Moreover, the investor collects income each month, which helps pay for the longer-dated ITM call option. At any point, due to extrinsic value, the investor may be able to sell the call option for a much higher ROI.

The bottom line is that shorting OTM NDAQ puts and buying ITM calls makes sense here.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)