/AI%20(artificial%20intelligence)/AI%20microchip%20by%20DesignKingBD360%20via%20Shutterstock.jpg)

This earnings season has been strange, as many semiconductor and tech stocks sold off sharply after reporting, even when they beat estimates. Even as the chip leader Nvidia (NVDA) cooled off after a blowout quarter, investors parsed supply, demand, and margin dynamics.

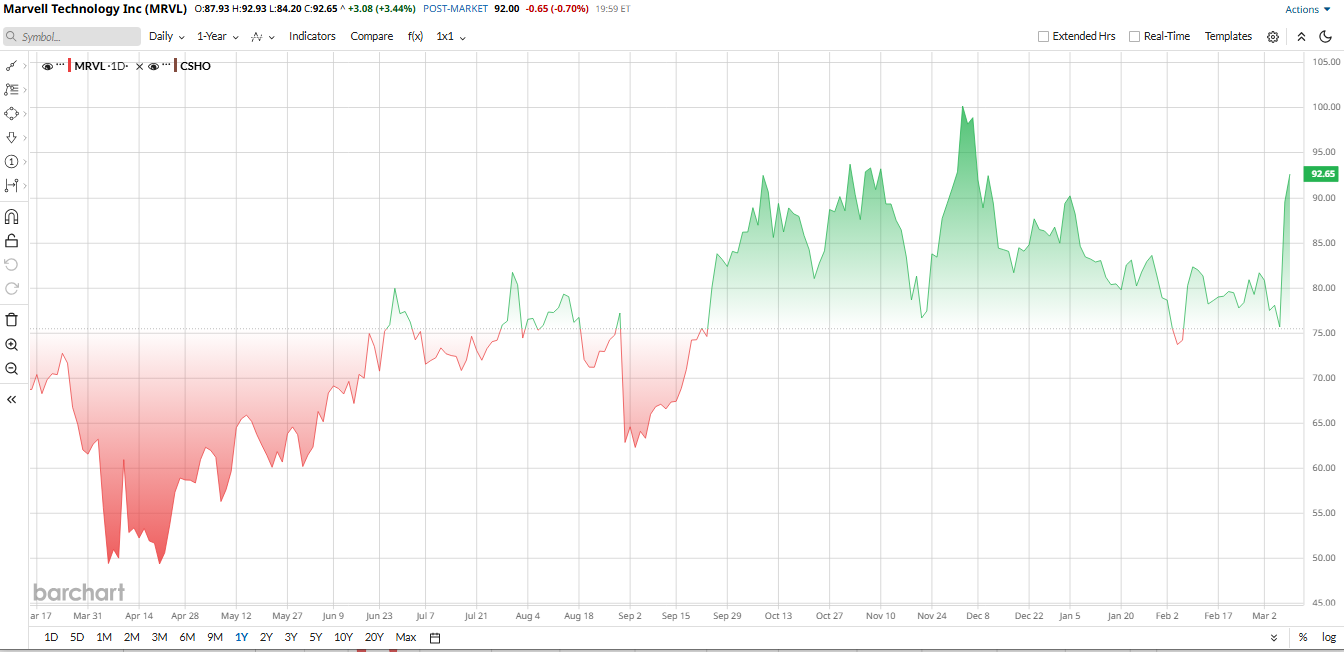

However, in the case of Marvell Technology (MRVL), it's been totally different. MRVL shares ripped higher, posting a double-digit jump after a strong beat and a lifted outlook. Analysts are saying they have fresh “confidence” in Marvell’s ability to monetize the AI boom.

Several analyst firms, including Bank of America, bumped their rating after the print, pointing to Marvell’s expanding custom-AI programs and optical interconnect wins with hyperscalers as key catalysts. If you’re weighing whether to buy now, the case comes down to two questions: can Marvell sustain accelerating data center revenue and turn a bigger cash pile into durable margin expansion?

Below is a closer look at the numbers and what Wall Street is saying.

Marvell’s AI-Driven Growth

Marvell is a leader in data infrastructure semiconductors. It's chips, power switches, optical interconnects, ASICs, and accelerators at large cloud and communications companies. The company reported a record revenue in 2026, which showed 42% growth from last year. CEO Matt Murphy notes “robust AI demand” has driven Marvell’s growth, and design wins hit an all‑time high in FY2026. Its products now serve data center and communications end markets across cloud and enterprise.

Beyond its core growth story, the company has also been strengthening its technology portfolio to capitalize on the AI boom. Late in 2025, it announced acquisitions of Celestial AI, a photonic interconnect start-up, and XConn Technologies. Both deals close in fiscal 2027 and expand Marvell’s AI-oriented product lineup. These were welcomed by investors as positive catalysts. Combined with the record design wins and bookings, they paint a bullish picture.

Over the past six months, MRVL shares have run solidly higher amid the AI chip boom. Marvell stock is roughly 40% above its last September slump. This outperformance came on the strong heels of Marvell’s fundamentals, strong bookings, and pipeline.

Even after the rally, valuation metrics suggest the stock may still have room to run. From a valuation standpoint, Marvell still looks attractive. In 2027, its P/E is roughly 16×, well below the 29× average for large-cap chip peers. Likewise, its EV/sales is only 4× versus 9× for similar companies. In other words, MRVL trades at a steep discount to the sector despite faster growth. Even Goldman Sachs notes Marvell’s price-earnings relative to growth (PEG) is extremely low at 0.1.

Marvell Delivers Beat and Raise Q4

In its Q4 earnings results, Marvell blew past analysts’ estimates with a strong beat. Revenue came in at $2.219 billion, up 22% year-over-year (YoY). Data center sales, which account for nearly three-quarters of total revenue, reached $1.651 billion, marking a 21% increase, while the communications and other segment generated about $567 million, up 26%.

Profitability remained robust as GAAP net income rose to $396 million, compared with $200 million a year earlier. On an adjusted basis, profit reached $0.80 per share, topping Wall Street’s $0.79 forecast.

The company also generated $373.7 million in operating cash flow and ended the quarter with about $948 million in cash and equivalents. Free cash flow and liquidity remained solid despite recent acquisitions.

Management was clearly pleased. CEO Murphy said, “We delivered record fiscal 2026 revenue, growing 42% year-over-year, driven by robust AI demand.” He noted that “bookings are at a record pace” and design wins in FY2026 hit an all‑time high, setting the stage for continued growth. This confidence helped Marvell raise its guidance. For Q1 2027, it sees revenue around $2.40 billion ±5% with EPS near $0.79.

More impressively, management now projects roughly 40% annual revenue growth in fiscal 2027 to $11 billion, led by the data center segment. As a result, Wall Street analysts have boosted their numbers; BofA now forecasts FY2027 EPS of $3.82 and FY2028 of $5.43, up 34% and 42% YoY.

Investors cheered on earnings, sending the stock higher more than 10% following the results. Bank of America’s Vivek Arya attributed this jump to “strong earnings beat, upward outlook revisions, and analyst upgrades” around Marvell’s AI connectivity products. He upgraded the stock from “Neutral” to “Buy,” citing “increased confidence” in Marvell’s position in AI optical interconnects and custom chip programs.

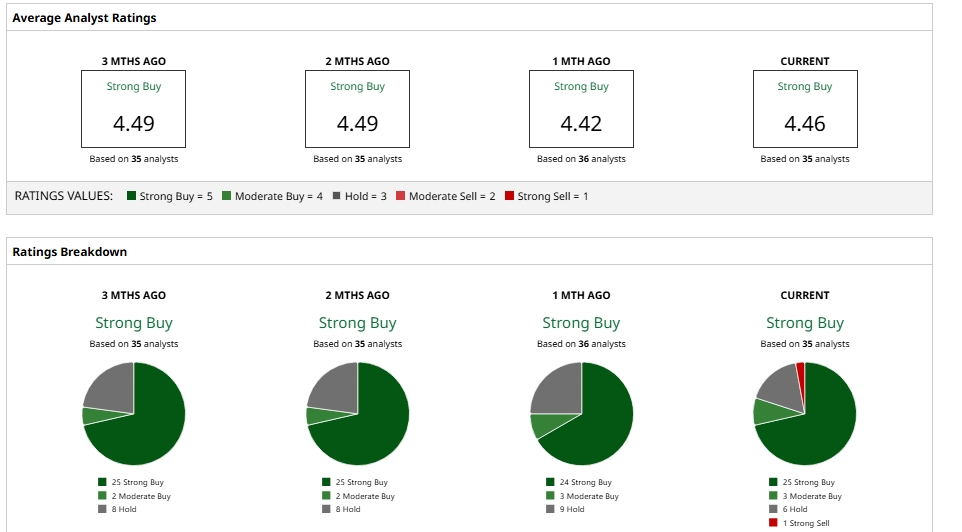

Analysts Remain Bullish on MRVL Stock

Wall Street’s analyst community has gotten uniformly more constructive on Marvell Technology after the quarter, lifting targets and citing a clearer line of sight into AI-driven demand.

Bank of America and RBC Capital pushed targets sharply higher to $110 and $115, pointing to stronger guidance and expanding custom-ASIC and interconnect pipelines.

Morgan Stanley highlighted management’s confidence and robust optical demand.

The most bullish call came from KeyBanc, which put a $130 target on the stock. Analysts broadly point to accelerating data center bookings, including custom programs with Amazon (AMZN) and Microsoft (MSFT), as the primary upside driver. A minority warns of cyclical chip risk and increasing competition.

If we see overall, the Wall Street aggregate is heavily bullish with a consensus “Strong Buy” rating from 35 analysts in coverage. Plus, the mean price target set by the bullish group is $119, which suggests even after the bull run, there's still room for a 25% increase from current levels.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)