/Cybersecurity%20by%20AIBooth%20via%20Shutterstock.jpg)

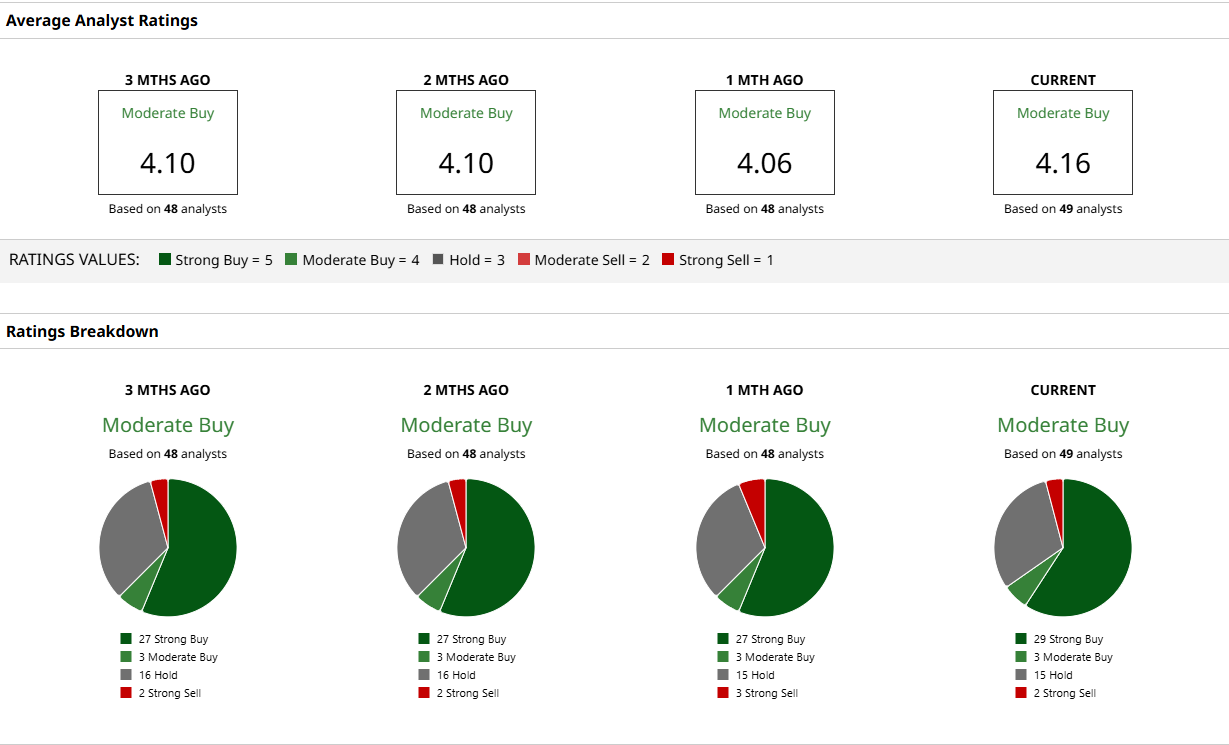

CrowdStrike (CRWD) stock is enjoying some green days at a time when software stocks are facing existential threats due to AI. The main reason for the optimism is, of course, the recent earnings, but analysts have also come out with positive comments, reassuring investors that things aren’t as bad as many were portraying since last month. Some did revise their target prices lower but maintained a bullish stance on the company’s outlook.

Wedbush analyst Dan Ives maintained the company on the IVES AI 30 list, calling the firm “the gold standard of cybersecurity.” Ives believes the company’s Falcon platform doesn’t face a threat from AI. Instead, it becomes even more relevant in today's AI threat landscape. Evercore was more or less neutral, calling the company’s performance in line with expectations. Morgan Stanley maintained a bullish outlook, impressed by the company’s ability to scale its operations and continue its growth. While these developments are positive, they are made even more attractive thanks to the recent pullback in stock prices.

About CrowdStrike Stock

CrowdStrike is known for its Falcon platform, a cloud-native cybersecurity platform that uses AI and machine learning to detect and thwart cyberattacks. The company has a significant role to play as AI and AI agents go mainstream. It is headquartered in Austin, Texas.

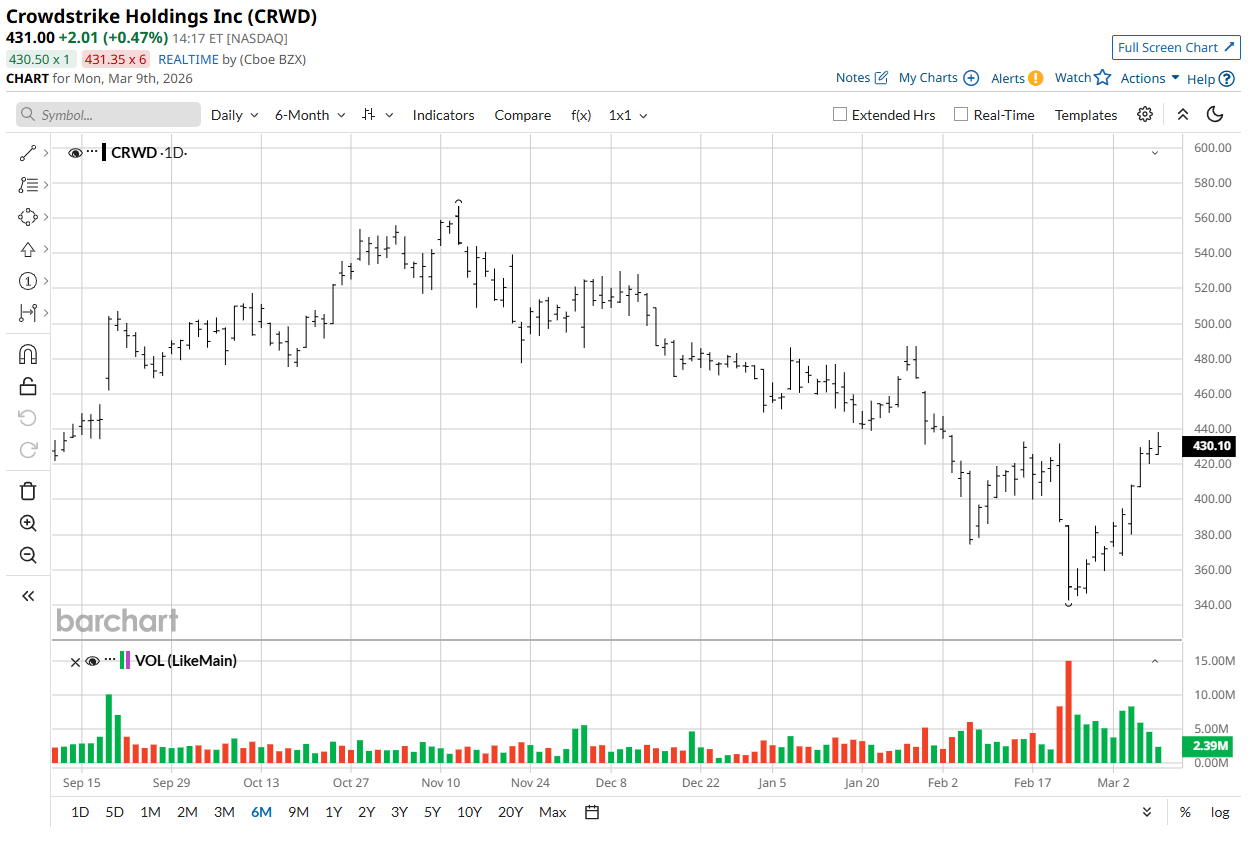

CRWD stock returned 39% in the last 12 months, while the iShares Cybersecurity and Tech ETF (IHAK) was down 6% during the same period. CrowdStrike enjoys a premium among cybersecurity companies, so it isn’t surprising that it has significantly outperformed its peers.

Despite more than doubling in the last five years, CRWD stock trades at a discount to its five-year average based on various metrics.

For instance, its forward price-to-book ratio of 19.15x is significantly lower than the five-year average of 30.22x. On a forward price-to-cash flow basis, it is trading at a multiple of 52.46x, quite high but still below the five-year average of 65.24x. What’s more, the discount exists despite impressive earnings growth prospects. The company is set to grow its profits by 30.3% in 2027, 27% in 2028, and 31.3% in 2029.

Yes, it is also trading at a forward P/E of 88.26x, but that is expected of a growing company, especially one that is a class above the rest. What’s more, this forward P/E is still less than half of the five-year average forward P/E of 193x. Quite a discount.

CrowdStrike Fails to Beat Wall Street Estimates

CrowdStrike announced its Q4 earnings report on March 4. It reported a revenue of $1.31 billion and a net income of $38.7 million. While the net income was down 141.9% year-over-year (YoY), a strong operating cash flow of $497.9 million means the firm is doing better than what the profits suggest. The company was unable to beat Wall Street estimates in the quarter despite registering a 23.3% YoY revenue growth.

The annual recurring revenue for FY 2027 is expected to be somewhere between $6.466 billion and $6.516 billion. This reflects a 23% to 24% growth rate, healthy enough to remove doubts surrounding disruption from the latest AI models. Responding to RBC’s Matthew Hedberg, management noted that protecting AI agents is a massive opportunity and one that the company is well-positioned to capitalize on. There is, of course, a threat from AI, considering it is a technology in development and brings new challenges with every innovation. It is a risk investors need to take on if they are betting on CrowdStrike being the major protector of AI cloud workloads.

What Analysts Are Saying About CRWD Stock

Analysts have been lowering their price targets on the CRWD stock in the last few days. Citi analyst Fatima Boolani lowered her price target on the stock to $525 from $610, while UBS analyst Roger Boyd lowered his price target to $525 from $590.

These new targets still offer significant upside despite being lower than the prior targets. The software selloff has brought the stock down to such low levels that the risk-reward ratio is skewed in favor of those who are brave enough to invest against the trend.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)