/D_R_%20Horton%20Inc_%20outside%20sign%20by-%20JHVEPhoto%20via%20Shutterstock(1).jpg)

With a market cap of $44.2 billion, D.R. Horton, Inc. (DHI) focuses on acquiring and developing land, as well as constructing and selling residential homes across 126 markets in 36 states. Its housing portfolio includes single-family detached homes and attached housing such as townhomes and duplexes.

Companies valued at $10 billion or more are generally considered "large-cap" stocks, and D.R. Horton fits this criterion perfectly. In addition to homebuilding, it offers mortgage financing, title services, rental property development, insurance-related operations, and manages various real estate and water-related assets.

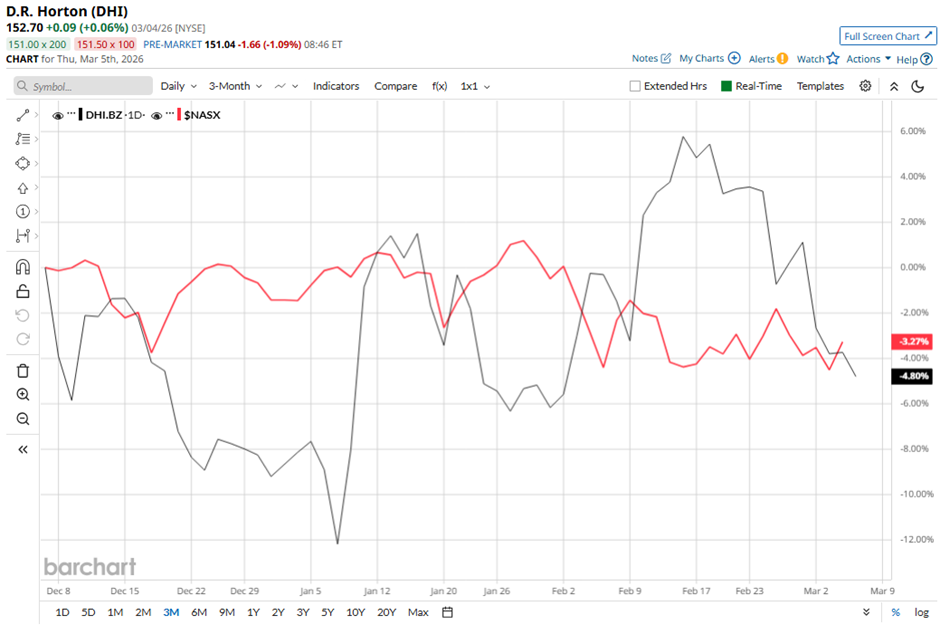

Shares of the homebuilder have fallen 18.2% from its 52-week high of $184.54. DHI stock has decreased 5% over the past three months, a more pronounced decline than the broader Nasdaq Composite’s ($NASX) 3% dip during the same time frame.

In the longer term, shares of D.R. Horton have surged 21.3% over the past 52 weeks, lagging behind the NASX’s 24.7% return over the same time frame. However, DHI stock is up 6% on a YTD basis, exceeding NASX's 1.9% drop.

The stock has been trading above its 200-day moving average since late July 2025.

Shares of D.R. Horton fell 1.8% on Jan. 20 after the company reported Q1 2026 net income of $594.8 million ($2.03 per share), which declined 30% year-over-year, while EPS dropped 22%. The report also showed homebuilding revenue fell 9% to $6.5 billion, and homes closed declined 7% to 17,818, indicating slowing housing activity despite total consolidated revenue of $6.9 billion. Additionally, management warned that affordability constraints, cautious consumer sentiment, and continued elevated sales incentives in fiscal 2026 could pressure demand and margins.

In comparison, rival Lennar Corporation (LEN) has lagged behind DHI stock. LEN stock has gained 3.1% on a YTD basis and decreased 13.1% over the past 52 weeks.

Due to the stock's underperformance relative to the Nasdaq over the past year, analysts remain cautious about its prospects. DHI stock has a consensus rating of "Hold" from the 21 analysts covering the stock, and the mean price target of $161.57 suggests a premium of 5.8% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)

/Advanced%20Micro%20Devices%20Inc_%20logo%20on%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

/Palantir%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock.jpg)

/Robinhood%20app%20on%20phone%20by%20Andrew%20Neel%20via%20Unsplash.jpg)