President Donald Trump's administration is reportedly considering a ban on large institutional investors buying single-family homes to help alleviate the housing affordability crisis. The proposal is titled “Trump Homes” and could involve some 1 million houses.

With this proposal in clear view, shares of homebuilders Lennar (LEN) and Taylor Morrison Home (TMHC) both rose more than 3% on Feb. 3 after a Bloomberg report mentioned that the two companies were among the group working on the “Trump Homes” proposal. The plan is to have a large-scale program to sell entry-level homes, which would then transform into a pathway-to-ownership program funded by private investors. In one version of the plan, investors would lease the homes to renters, with a portion of the rent applied as a down payment credit. Tenants may choose to purchase the property after three years using the accumulated funds.

Against this backdrop, homebuilding stocks Lennar and Taylor Morrison Home might be the ones to watch out for.

Homebuilder Stock #1: Lennar (LEN)

Lennar ranks among the United States' top homebuilders, specializing in building and marketing single-family residences, townhouses, and condominiums targeted at entry-level, upgrade, retirement, and high-end buyers. Active in several states across homebuilding, financial services, multifamily ventures, and tech investments, it’s based in Miami, Florida with a market capitalization of $29.4 billion.

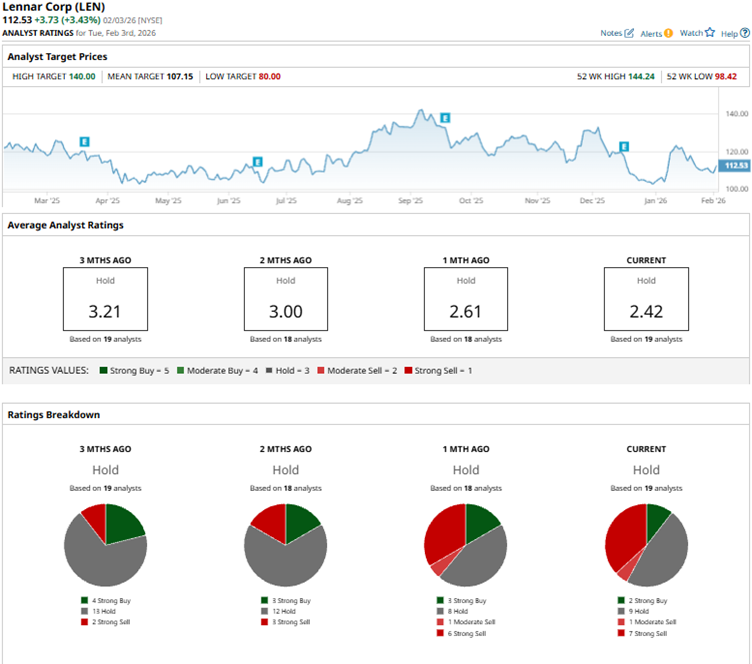

The stock has been seeing the headwinds from high mortgage rates, slowing demand, and margin pressures. LEN stock is down 9% over the past 52 weeks, while it has declined 4% over the past six months. Lennar shares reached a 52-week high of $144.24 in September 2025, but are down by about 20% from that level.

Lennar’s stock selloff has led to a modest valuation. Its forward price-to-earnings (P/E) ratio of 17.4 times is lower than the industry average of about 18.2 times.

In the fourth quarter of fiscal 2025, total revenue decreased by 5.8% year-over-year (YOY) to $9.37 billion, above Wall Street analysts’ $9.13 billion estimated figure. The drop in the topline is attributed to a 6.9% decline in homebuilding revenues, as the company continues to face a challenging environment despite lower interest rates in Q4. This, in turn, depended on a 10% decrease in the average sales price of homes delivered (despite the number of delivered homes growing) due to market weakness and sales incentives for homebuyers. The situation is also squeezing Lennar’s margins. Adjusted EPS dropped from $4.03 to $2.03, missing the Street's estimated $2.23 figure.

Lennar recently sold the majority interest in its struggling multifamily business Quarterra to TPG Real Estate (TRTX). The company continues to hold a minority stake, while TPG has made an additional $1 billion strategic commitment in connection with the acquisition.

For the current quarter, analysts expect Lennar’s profit to drop 55% YOY to $0.96 per diluted share. Meanwhile, for the current fiscal year, EPS is expected to decrease 20% to $6.44 per diluted share.

Wall Street is currently taking a cautious stance on LEN stock, with analysts awarding it a consensus “Hold” rating overall. Of the 19 analysts rating the stock, two analysts have a “Strong Buy” rating, nine analysts offer a “Hold” rating, one analyst suggests a “Moderate Sell,” and seven analysts recommend a “Strong Sell.”

Despite the selloff over the past year, the consensus price target of $107.15 represents 7% potential downside from current levels. However, the Street-high price target of $140 indicates 21% potential upside from here.

Homebuilder Stock #2: Taylor Morrison Home (TMHC)

Taylor Morrison Home is a leading U.S. homebuilder designing, constructing, and selling single-family homes, townhomes, and communities across several states. It offers mortgage, title, and financial services to streamline the homebuying process. Headquartered in Scottsdale, Arizona, the company has a market capitalization of $6.4 billion.

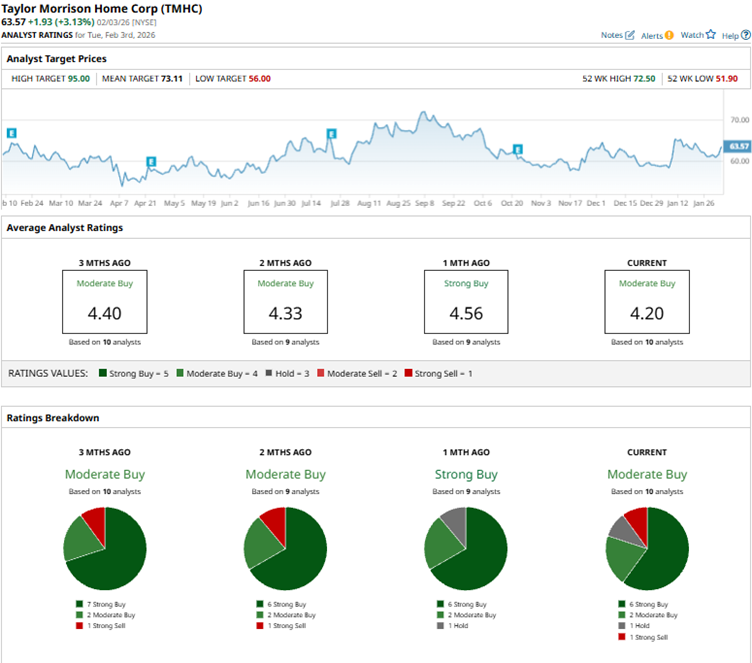

High mortgage rates and squeezing homebuilder margins have also affected TMHC stock. Over the past 52 weeks, the stock has gained a modest 1.5%. Over the past six months, shares are up by 1.6%. TMHC reached a 52-week high of $72.50 in September 2025, but the stock is now down 9% from that level.

TMHC shares are trading at an attractive valuation. The forward P/E ratio of roughly 9.4 times is cheaper than the industry average of 18.2 times.

For the third quarter of fiscal 2025, based on a challenging homebuying environment, total revenue decreased 1.2% YOY to $2.1 billion, surpassing the $2.04 billion expected figure. The topline decline was driven by a modest drop in net home-closing revenue and a significant drop in land-closing revenue.

Net sales orders in the homebuilding segment declined 13% due to a decline in monthly absorption to 2.4 from 2.8 a year ago. At the end of the quarter, backlog was 3,605 homes with a sales value of $2.3 billion.

The margins have also declined for Taylor Morrison. Its adjusted home closings gross margin (as a percentage of home closings revenue) dropped 25% to 22.4%, while adjusted EPS dropped 12.1% annually to $2.11. However, this exceeded the $1.93 that analysts had expected for the period.

For the fourth quarter of fiscal 2025 (to be reported on Feb. 11), analysts expect Taylor Morrison Home’s profit to decline 34% YOY to $1.73 per diluted share. For fiscal 2025, EPS is expected to drop 7% to $8.11 per diluted share, followed by a decline of 17% to $6.74.

Wall Street analysts are still moderately optimistic about TMHC stock, with analysts awarding it a consensus “Moderate Buy” rating overall. Of the 10 analysts rating the stock, six offer a “Strong Buy” rating, two analysts suggest a “Moderate Buy,” one analyst has a “Hold” rating, and one analyst recommends a “Strong Sell.”

The consensus price target of $73.11 represents 11% potential upside from current levels. However, the Street-high price target of $95 indicates 44% potential upside from here.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/Friends%20choosing%20a%20movie%20on%20a%20streaming%20service%20by%20Stock-Asso%20via%20Shutterstock.jpg)