/Oracle%20Corp_%20logo%20on%20phone%20and%20stock%20data-by%20Rokas%20Tenys%20via%20Shutterstock.jpg)

Oracle (ORCL) stock's performance has been ordinary, with a downside of 10% in the last 52 weeks. While valuations seem attractive, the markets have been concerned about AI investments, the impact on the balance sheet, and cash flows.

However, even after discounting these concerns, Oppenheimer has upgraded ORCL stock to “Outperform” from “Perform” with a price target of $185. The bullish thesis is backed by the view that Oracle is likely to be a strong EPS compounder. Even after a 25% haircut to management’s guidance, Oracle’s EPS is likely to double by 2030. Further, with Oracle announcing a $40 billion to $50 billion equity and debt financing program for 2026, the financing and execution risk is likely to decline.

Finally, Oracle's multiples have been "cut by more than half since September,” per Seeking Alpha. This provides a good entry opportunity in a stock that also offers an annual dividend yield of 1.38%.

About Oracle Stock

Headquartered in Austin, Texas, Oracle offers products and services for enterprise IT globally. The company’s main business segments include cloud, software, hardware, and services. For the first six months of fiscal 2026, the cloud and software segments contributed to 86% of total revenues.

For fiscal 2025, Oracle reported revenue of $57 billion. The company has guided for an ambitious revenue target of $225 billion by 2030. This would imply a compound annual growth rate (CAGR) of 31% between fiscal 2025 and fiscal 2030. Further, for the same period, Oracle expects non-GAAP EPS to increase at a CAGR of 28% to $21 by fiscal 2030.

While Oracle has ambitious growth targets, ORCL stock has corrected by 34% in the last six months. This is a good accumulation opportunity as the company focuses on the execution of remaining performance obligations (RPO) that have swelled to $523 billion as of Q2 fiscal 2026.

Clear Revenue Visibility

Oracle has witnessed a sharp growth in RPO with commitments from the likes of OpenAI, Meta Platforms (META), and Nvidia (NVDA) , among others. However, the stock price has been in a downtrend.

A key reason is the market skepticism on financing and execution. However, Oracle took a positive step with a $25 billion debt raise in February 2026 — a record-setting bond deal that has eased financing concerns. It’s worth mentioning that Oracle has also entered into an equity distribution deal to sell up to $20 billion in stock. With $19.2 billion in cash buffer as of Q2 2026, the growth financing is unlikely to be a concern.

Once the focus shifts to execution and results are seen in terms of top-line growth, ORCL stock is likely to trend higher. In regard to the RPO, Oracle expects to recognize 10% as revenue over the next 12 months. Further, 30% will be recognized over the subsequent month 13 to month 36, followed by 35% over the subsequent month 37 to month 60.

The next 12 to 24 months are crucial, as it will indicate whether Oracle is indeed executing the RPO according to schedule. Positive numbers on that front could potentially ensure a sharp reversal in ORCL stock.

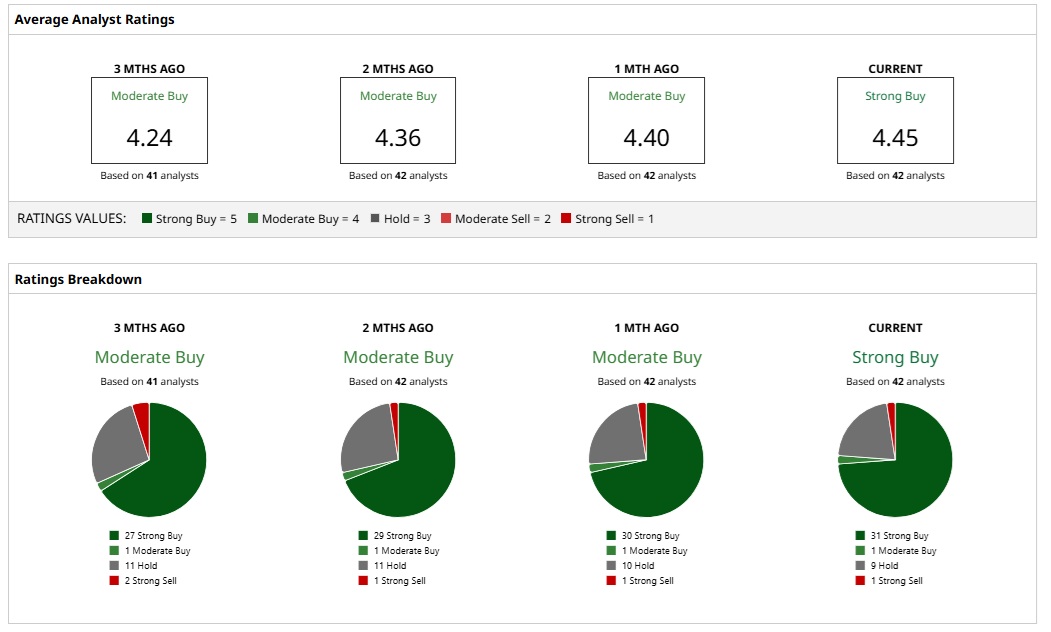

What Do Analysts Say About ORCL Stock?

Based on 42 analysts with coverage, ORCL stock is a consensus “Strong Buy.” While 31 analysts assign a “Strong Buy” rating, one analyst has a “Moderate Buy" rating, nine analysts have a “Hold,” and one analyst offers a “Strong Sell" rating.

Analysts have a mean price target of $284.02, implying about 91% potential upside from here. Further, the most bullish price target of $400 suggests that ORCL stock could rise as much as 168% from current levels.

From a valuation perspective, Oracle stock trades at a forward price-to-earnings (P/E) ratio of 24.18 times. This is attractive, considering the growth potential through 2030. According to BNP Paribas, OpenAI has plans to spend some $600 billion on computing power by 2030. Microsoft (MSFT) and Oracle are likely to be key beneficiaries of this spending.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)