The last few weeks have felt like a roller coaster for software and cybersecurity stocks. When Anthropic rolled out new artificial intelligence (AI) tools through its Claude model in late January, investors quickly began questioning which companies might get disrupted next. LegalZoom.com (LZ) didn’t escape the panic. Fears that AI could upend traditional legal workflows sent the stock tumbling in early 2026, as the market braced for change. But the story did not end there.

Instead of resisting the AI shift, LegalZoom chose to lean into it. On Feb. 24, the company announced that its attorney-services integration would be built directly into the Claude ecosystem, with the launch of LegalZoom’s Connector. That is a meaningful pivot. While Claude can rapidly review documents and streamline early legal tasks, complex compliance questions and liability risks still demand human expertise.

Through LegalZoom’s Connector, users can move seamlessly from AI-powered analysis to real attorney guidance on the same platform. The update has helped restore some confidence in the company’s long-term relevance. But with the stock still stuck deep in the red so far in 2026, is this lingering weakness a warning sign or an opportunity hiding in plain sight?

About LegalZoom Stock

Founded in 2001, California-based LegalZoom has carved out a leading position in online legal services by making the legal system more approachable for individuals and small businesses. Its platform combines easy-to-use technology with access to licensed attorneys, covering needs such as business formation, compliance, intellectual property, and ongoing legal support. The company has also been actively adopting AI to stay relevant.

As AI begins to transform how legal tasks are handled, LegalZoom is emphasizing a human-in-the-loop model, using technology to streamline processes while keeping professional legal judgment at the center. With more than two decades of operating history and millions of customers served, the company continues to position itself at the intersection of automation and accountability.

Currently valued at a market capitalization of about $1.2 billion, LegalZoom’s shares sprang back to life after the company announced the launch of its Connector and attorney-services integration into Claude’s ecosystem on Feb. 24. The market clearly liked what it heard, sending the stock higher for three consecutive sessions as investors reassessed the company’s AI strategy.

Yet, the bigger picture remains challenging. Despite the recent bounce, LegalZoom remains under pressure in 2026. Lingering concerns around agentic AI disruption have weighed heavily on sentiment, driving the stock down nearly 29.9% year-to-date (YTD). That stands in sharp contrast to the broader S&P 500 Index ($SPX) which has managed to stay marginally positive over the same stretch.

LegalZoom’s Q4 Earnings Snapshot

LegalZoom’s latest earnings report added fuel to the recent share price decline. After releasing its fiscal 2025 fourth-quarter results on Feb. 19, the stock slid roughly 7% in the following session, as investors reacted to a mixed performance. On the surface, the top line looked solid. Fourth-quarter revenue rose about 18% year-over-year (YOY) to $190.3 million, comfortably beating Wall Street’s estimate of $184.3 million.

Breaking it down further, transaction revenue climbed 12% annually to $59.3 million, while subscription revenue jumped 20% to $130.9 million, underscoring continued strength in recurring revenue streams. The bottom line, however, disappointed. Adjusted earnings per share slipped to $0.17 from $0.19 a year earlier and missed the Street’s $0.18 expectation. Still, there were encouraging signs beneath the surface.

Gross margin improved to 68%, up from 67% in the same quarter of 2024. Meanwhile, cash and cash equivalents strengthened significantly, rising to $203.1 million as of Dec. 31, 2025, compared to $142.1 million a year earlier. In a notable show of confidence, the board approved a $100 million increase to the company’s existing share repurchase authorization, reinforcing its commitment to returning capital to shareholders.

Looking ahead, LegalZoom is projecting steady growth in 2026. The company expects full-year revenue between $805 million and $825 million, representing roughly 8% YOY growth at the midpoint, driven by higher-value customer acquisition and expanded human-in-the-loop service offerings.

On the profitability side, adjusted EBITDA is forecast to range between $190 million and $200 million, implying about 13% growth at the midpoint. The outlook reflects improving gross margins and disciplined cost management, signaling that the company is focused not just on expanding revenue, but on doing so efficiently.

How Are Analysts Viewing LegalZoom Stock?

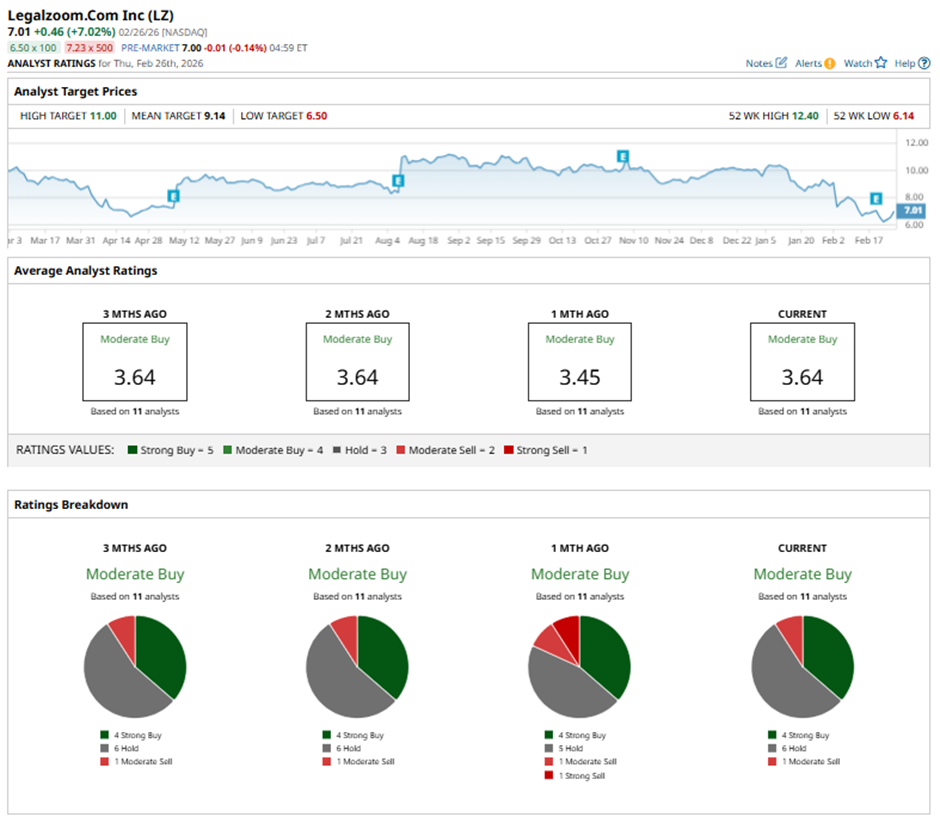

Despite the recent slide, Wall Street’s outlook is far from gloomy. The stock still carries a consensus “Moderate Buy” rating, reflecting cautious optimism about its recovery potential. Of the 11 analysts covering the name, four call it a “Strong Buy,” six suggest “Hold,” and only one recommends a “Moderate Sell.” The average price target of $9.14 signals about 30% upside from current levels, while the Street-high target of $11 points to a possible surge of nearly 57%.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

/Sign%20of%20Intel%20at%20entrance%20%20by%20michaelmond.jpeg)

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)