Chicago, Illinois-based Ventas, Inc. (VTR) is a prominent healthcare real estate investment trust (REIT) that owns and manages a diversified portfolio of senior housing, medical office buildings, life science facilities, and healthcare-related properties. With a market cap of $36.5 billion, the company operates across North America and partners with major healthcare providers, hospital systems, and senior living operators.

The REIT has delivered standout performance over the past year, comfortably beating both the broader market and its sector peers. VTR stock prices have soared 29.1% over the past 52 weeks, outpacing the S&P 500 Index’s ($SPX) 14% gains. In 2026, both VTR and the index have gained marginally.

Zooming in, the sector-specific State Street Real Estate Select Sector SPDR Fund (XLRE) has observed a marginal rise over the past 52 weeks, trailing the stock.

Ventas has outperformed the broader market over the past year, largely due to a strong rebound in its senior housing business, with improved occupancy and rental rates as post-pandemic demand normalized and aging population trends strengthened. Investors have also been encouraged by rising cash flows, disciplined cost management, and better operating margins across its portfolio. In addition, easing interest-rate concerns and expectations of future rate cuts boosted sentiment toward REITs, making income-oriented stocks like Ventas more attractive.

For FY2025 that ended in December, analysts expect VTR to deliver an NFFO of $3.48 per share, up 9.1% year over year. On a more positive note, the company has a solid FFO surprise history. It has surpassed the Street’s cash flow estimates in each of the past four quarters.

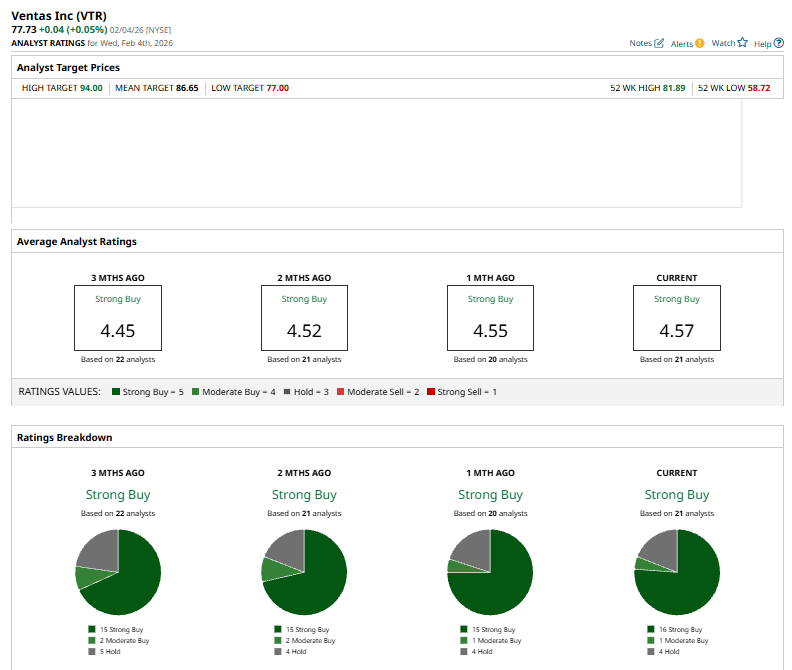

Among the 21 analysts covering the VTR stock, the consensus rating is a “Strong Buy.” That’s based on 16 “Strong Buys,” one “Moderate Buys,” and four “Holds.”

This configuration is slightly better than it was a month ago, when 15 analysts issued “Strong Buy” recommendations.

On Dec. 4, KeyBanc Capital Markets analyst Todd M. Thomas reaffirmed an “Overweight” rating on Ventas and raised his price target from $70 to $85, a 21.43% increase, signaling growing confidence in the company’s operating momentum and long-term performance.

VTR’s mean price target of $86.65 represents a modest 11.5% premium to current price levels. The Street-high target of $94 implies a 20.9% upside.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Abbott%20Laboratories%20vials%20and%20Logo-by%20Melniov%20Dmitriy%20via%20Shutterstock.jpg)