/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

In a move that captured attention, Western Digital Corporation (WDC) announced selling down its remaining equity stake in SanDisk Corporation (SNDK) , the flash memory powerhouse it spun off last year.

The company is executing a multi-billion-dollar secondary offering of SanDisk shares, involving a debt-for-equity swap with affiliates of J.P. Morgan and Bank of America. The transaction, which prices roughly 5.8 million shares at around $545 each for about $3.17 billion, is designed to accelerate deleveraging and sharpen Western Digital’s focus on its core hard-disk drive business.

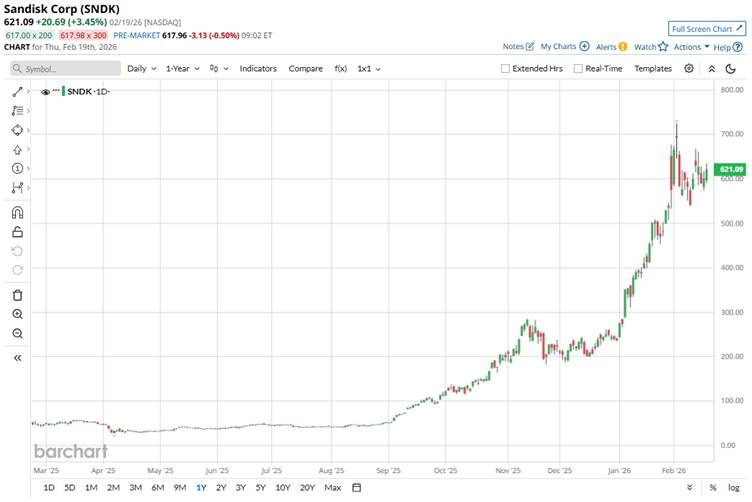

This strategic divestiture occurred against a backdrop of extraordinary performance for SanDisk since becoming an independent public company in early 2025; its shares have soared more than a thousand percent amid booming demand for NAND flash driven by AI and data-center growth.

Given this backdrop, what should be your move?

About SanDisk Stock

SanDisk Corporation is a leading data storage and flash memory company headquartered in Milpitas, California. The company designs, develops, and manufactures a broad portfolio of NAND flash storage products, including solid-state drives (SSDs), memory cards, USB flash drives, and embedded storage solutions. Founded in 1988, SanDisk has a long history of innovation in flash technology and, following its spin-off from Western Digital in 2025, operates as an independent publicly traded company listed on the NASDAQ. The company’s market cap has expanded dramatically, with its current standing at $95.9 billion.

Since its spin-off and listing on the Nasdaq on Feb. 24, 2025, SanDisk’s stock has delivered an extraordinary rally as investor enthusiasm quickly mounted as the company benefited from surging demand for NAND flash memory driven by AI infrastructure and enterprise storage growth.

The stock has experienced a meteoric run, hitting a high of $725 on Feb. 3, while total returns since its IPO is 1,223%, far outpacing broader markets.

However, SanDisk has seen recent dips tied directly to news of Western Digital’s share sale. The stock plunged 5.7% intraday on Feb. 17, following the news.

SanDisk’s overall momentum remained strong, with year-to-date (YTD) returns of roughly 180.77%, significantly outperforming major market benchmarks.

The stock is currently trading at a premium compared to the sector median, at 6.19 times forward sales.

Steady Financial Performance

SanDisk’s second-quarter fiscal 2026 earnings, released on Jan. 29, outpaced expectations. For the quarter, SanDisk reported revenue of nearly $3 billion, representing a 61% year-over-year (YOY) increase, driven by broad-based demand across data center, edge, and consumer segments and far exceeding consensus forecasts.

Breaking down, data center sales reached $440 million, up 76% YOY. The Edge segment generated about $1.7 billion, up 63% YOY, while consumer revenue of roughly $907 million grew 52% versus the prior period.

Moreover, on a non-GAAP basis, EPS came in at $6.20, far above the year-ago $1.23 and well above analysts’ expectations. Gross margins expanded dramatically to 51.1%, up roughly 18.6 percentage points versus the year-ago quarter, reflecting stronger pricing and a favorable mix toward higher-value SSD products.

Alongside the earnings beat, SanDisk issued very strong guidance for the third quarter of fiscal 2026, projecting revenue of $4.4 billion to $4.8 billion and non-GAAP EPS in the $12.00 to $14.00 range, implying another substantial sequential acceleration in both top and bottom line growth if achieved.

Analysts remain optimistic, forecasting EPS of $22.96 for fiscal 2026, a 1,190% YOY jump, followed by a further 95.5% rise to $44.88 in 2027.

What Do Analysts Expect for SanDisk Stock?

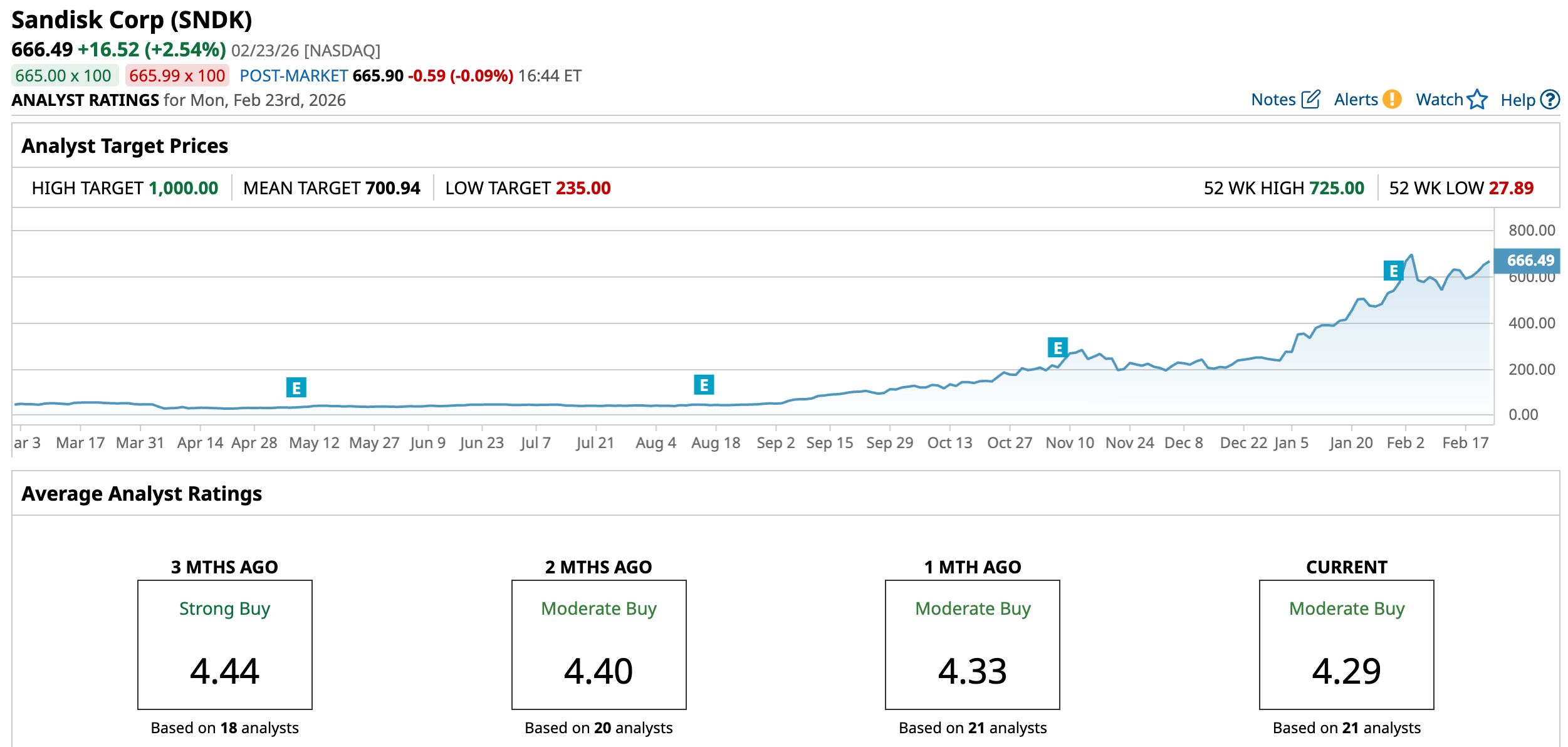

Earlier this month, Bernstein SocGen Group raised its price target on SanDisk to $1,000 from $580, maintaining an “Outperform” rating after a strong second-quarter earnings beat. Bernstein attributed the sharp price target hike to the sizable earnings beat, strong forward guidance, and a robust pricing environment.

Also, last month, Cantor Fitzgerald raised its price target on SanDisk to $800 from $550 and maintained an “Overweight” rating following strong quarterly results and upbeat guidance.

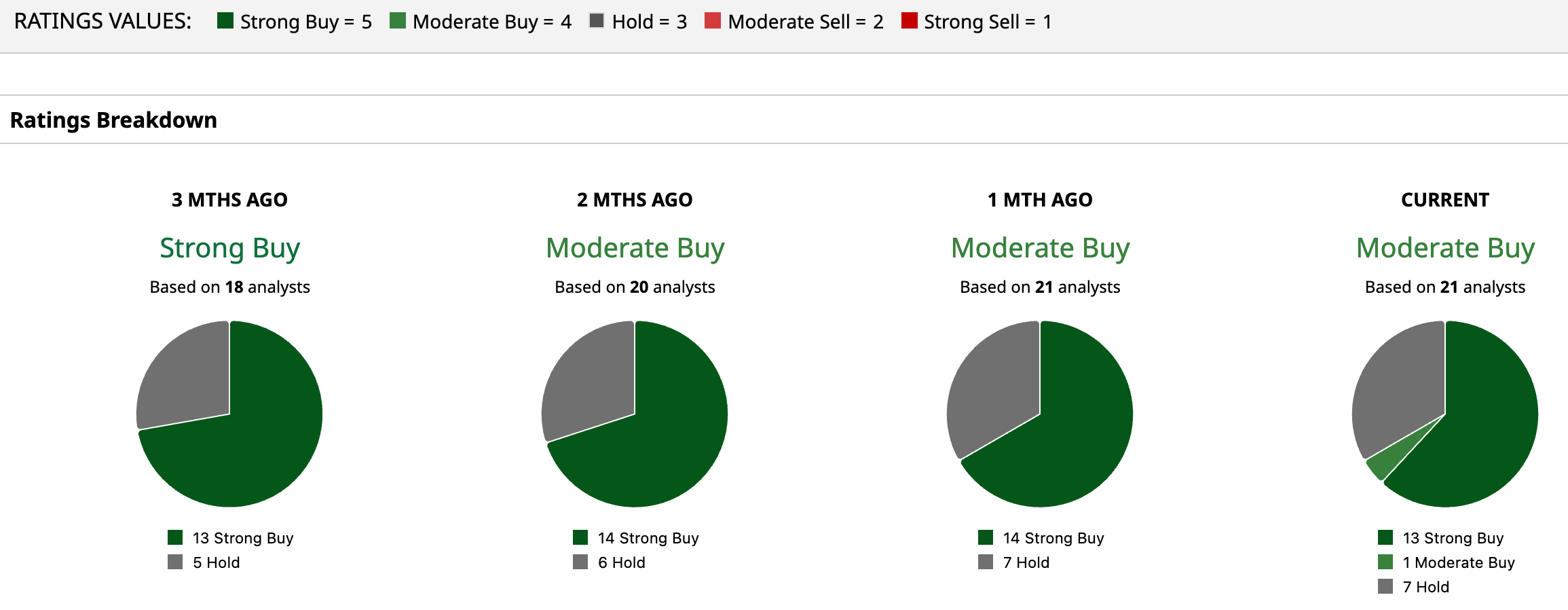

Overall, SNDK has a consensus “Moderate Buy” rating. Of the 21 analysts covering the stock, 13 advise a “Strong Buy,” one suggests a “Moderate Buy,” and the remaining seven analysts are on the sidelines, giving it a “Hold” rating.

SNDK’s average analyst price target of $700.94 indicates an upside of 5.2%, while Bernstein SocGen’s Street-high target price of $1,000 suggests that the stock could rally as much as 50%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)