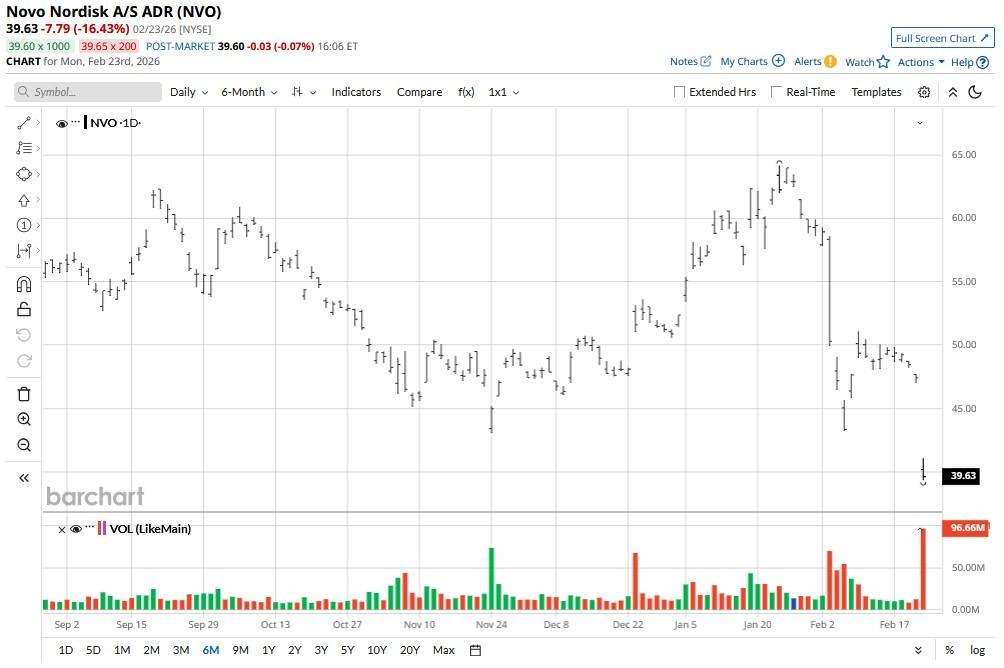

Novo Nordisk (NVO) crashed roughly 20% today after the pharma giant said its candidate obesity drug CagriSema failed to demonstrate non-inferiority to rival Eli Lilly’s (LLY) tirzepatide in the late-stage REDEFINE 4 trial. CagriSema achieved 23% weight loss in about 84 weeks compared to tirzepatide’s 25.5%, missing its primary endpoint and representing a notable competitive setback for NVO in the fast-growing obesity treatment market.

Versus its year-to-date high, Novo Nordisk stock is now down nearly 40% with a 14-day relative strength index (RSI) at less than 19, indicating oversold conditions that often precede a relief rally.

Is it Time o Sell Novo Nordisk Stock?

Despite recent weakness, NVO’s underlying fundamentals warrant consideration for patient, long-term investors.

Wegovy, the company’s core obesity drug, generated DKK 79.1 billion ($12.48 billion) in net sales last year — an exciting 36% year-on-year growth reflecting resilience against competitive pressures.

The drug was recently approved at a higher dose in Europe and as a pill in the United States, giving Novo Nordisk a headstart over Lilly, which has yet to launch its competing oral formulation.

A lucrative dividend yield of 4.69% makes NVO stock even more attractive as a long-term holding in 2026.

NVO Shares Are Trading at a Discount

Novo Nordisk shares are worth owning for its diversified portfolio as well, with multiple candidate drugs targeting adjacent cardiometabolic and metabolic diseases in late-stage trials.

Wegovy's emerging position as the only GLP-1 approved for metabolic-associated steatohepatitis, affecting an estimated 9 million to 15 million Americans, provides additional revenue streams less directly exposed to tirzepatide competition.

Moreover, NVO’s decline to its lowest levels since mid-2021 has compressed valuation metrics to levels that effectively make it a value stock.

At about 11x forward earnings, the pharma giant is currently trading at a significant discount to its historic multiple.

What’s the Consensus Rating on Novo Nordisk?

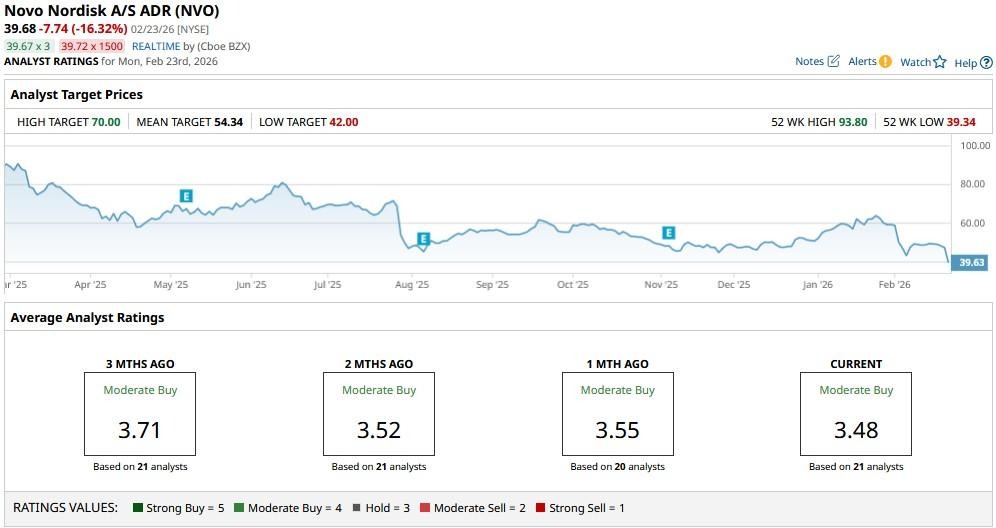

Wall Street analysts also recommend buying Novo Nordisk at the current, toned down valuation.

According to Barchart, the consensus rating on NVO shares remains at “Moderate Buy,” with the mean target of about $54 indicating potential upside of roughly 35% over the next 12 months.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)