/AI%20(artificial%20intelligence)/Image%20of%20server%20racks%20and%20cabinets%20full%20of%20hard%20drives%20inside%20large%20data%20center%20by%20IM%20Imagery%20via%20Shutterstock.jpg)

Projected to reach a market size of more than $2 trillion by 2032, the rally in chip stocks is far from over, as AI and the associated infrastructure buildout show no signs of slowing down. Now, the ways to benefit from this burgeoning industry have been through the same old counters like Nvidia (NVDA), AMD (AMD), and Broadcom (AVGO), which have already seen significant upside in their share prices. However, there was a time, about a decade ago, when these multibaggers used to trade at penny stock levels. Courage and conviction shown by shareholders to add these names to their portfolios during those times has led to immense wealth creation for them.

Thus, in this piece, I bring to you three names from the chip industry, trading at single digits, that are being favored by analysts currently. Although they have limited coverage, highlighting them here will keep these stocks on investors' radars.

Best Unheard-of Chip Stock #1: Atomera (ATOM)

Founded in 2001, Atomera (ATOM) is a semiconductor materials and technology licensing company based in California. Atomera’s business model centers on research, development, commercialization, and licensing of proprietary semiconductor materials technologies to semiconductor manufacturers and designers globally. Its flagship innovation, Mears Silicon Technology, is a quantum-engineered thin film of re-engineered silicon that can be integrated into existing CMOS fabrication processes to enhance transistor performance, power efficiency, and cost profiles across a wide range of applications.

Valued at a modest market cap of $74.8 million, the ATOM stock has dropped like an atom bomb over the past year, correcting by 85.9%.

In its latest quarter, the company reported a loss of $0.17 per share on revenues of $11,000. Although the loss came in higher than the consensus estimate of a loss of $0.14 per share, it remained unchanged from the previous year. However, the company closed the quarter with a healthy cash balance of $20.3 million, much higher than its short-term debt levels of $794,000.

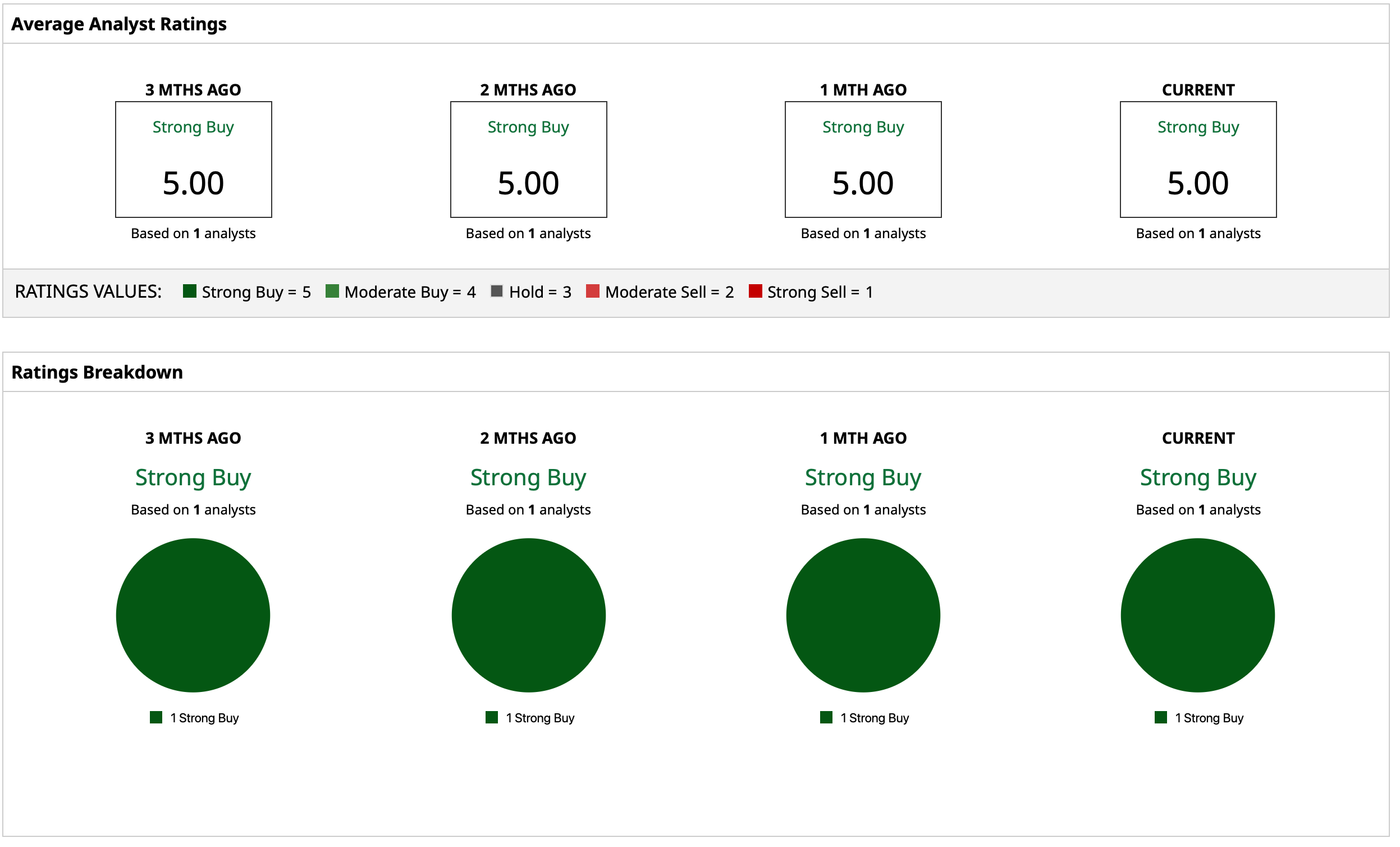

On Wall Street, only one analyst covers the stock with a “Strong Buy” rating and a mean target price of $5. This denotes an upside potential of about 118.3% from current levels.

Best Unheard-of Chip Stock #2: GCT Semiconductor (GCTS)

Founded in 1998, GCT Semiconductor (GCTS) is a fabless semiconductor company that designs, develops, and markets integrated circuits for the wireless semiconductor industry. Its portfolio includes 5G and 4G LTE integrated circuits, RF transceivers, baseband modem chipsets, and cellular IoT solutions for networks including eMTC, NB-IoT, and other protocols. Its chips are used in devices such as smartphones, tablets, mobile hotspots, USB dongles, routers, customer premise equipment (CPE), and machine-to-machine (M2M) IoT applications.

With a market cap of $69.7 million, the GCTS stock is down 56% over the past year.

GCT possesses higher total revenues than Atomera, with the company reporting revenues of $430,000 in the most recent quarter. However, it was considerably lower than the previous year's figure of $2.6 million. Moreover, its losses widened to $0.25 per share from $0.16 per share in the year-ago period, higher than the consensus estimate of a loss of $0.19 per share. Overall, the company closed the quarter with a cash balance of $8.3 million, much higher than its short-term debt levels of just $372,000.

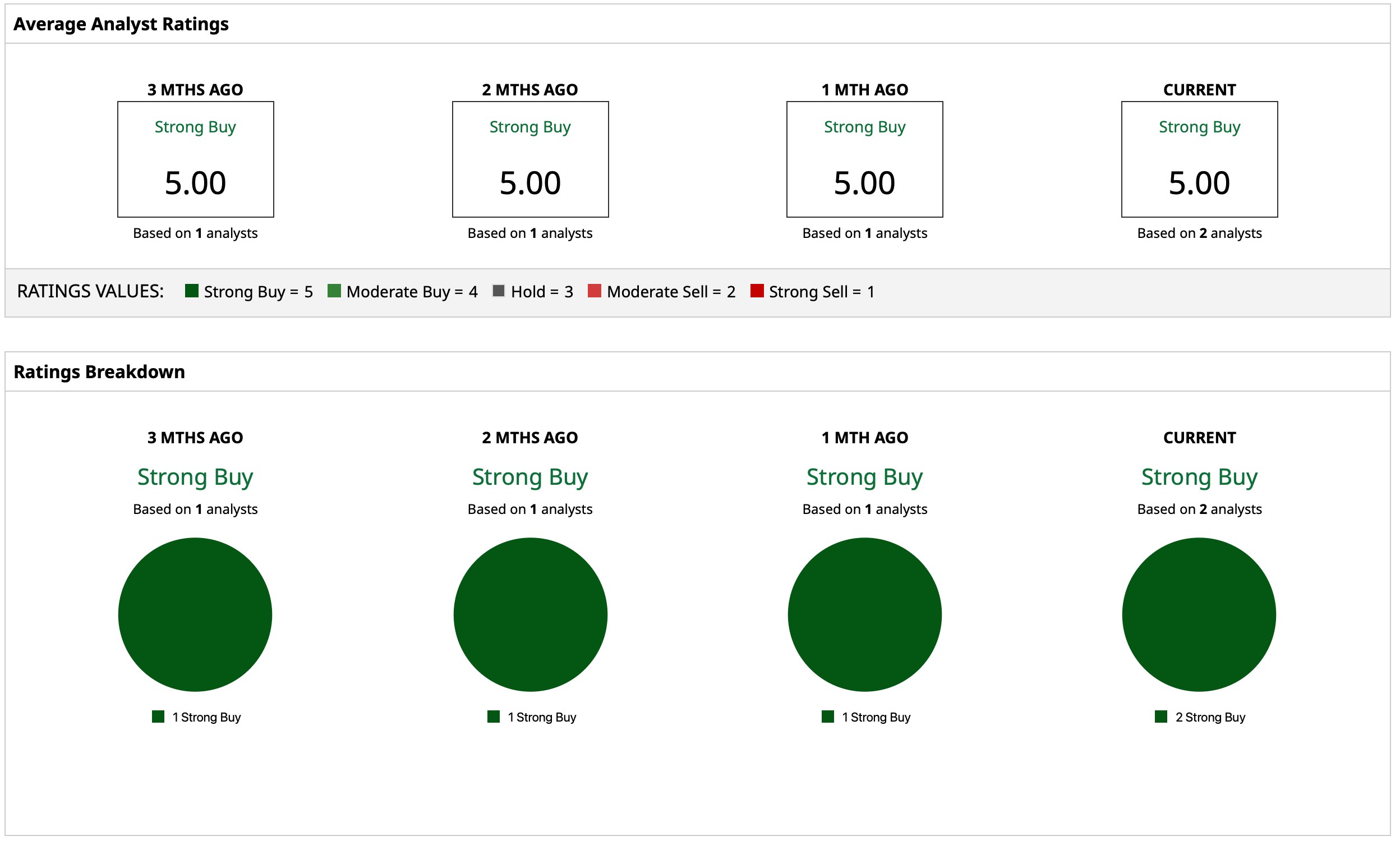

Overall, two analysts covering the stock have attributed to the GCTS stock a rating of “Strong Buy,” with a mean target price of $3.50, which indicates an upside potential of about 192% from current levels.

Best Unheard-of Chip Stock #3: Intchains Group (ICG)

We conclude our list with Intchains Group (ICG), a Chinese semiconductor and blockchain technology company founded in 2017 that operates primarily as a fabless designer of application-specific integrated circuits (ASICs) used in cryptographic and blockchain-related computing. Its core products are high-performance computing chips and systems optimized for specific cryptographic algorithms, along with associated hardware systems and software tools.

Valued at a market cap of $113.5 million, the ICG stock is down 59.1% over the past year.

Notably, Intchains happens to be the only profitable company in this list. For Q3 2025, the company reported revenues of $1.3 million, which was down 85% from the prior year. However, the EPS of $0.09 marked a significant leap from the previous year's figure of $0.04 per share. Overall, the company closed the September 2025 quarter with a cash balance of $36.5 million, with no short-term debt on its books.

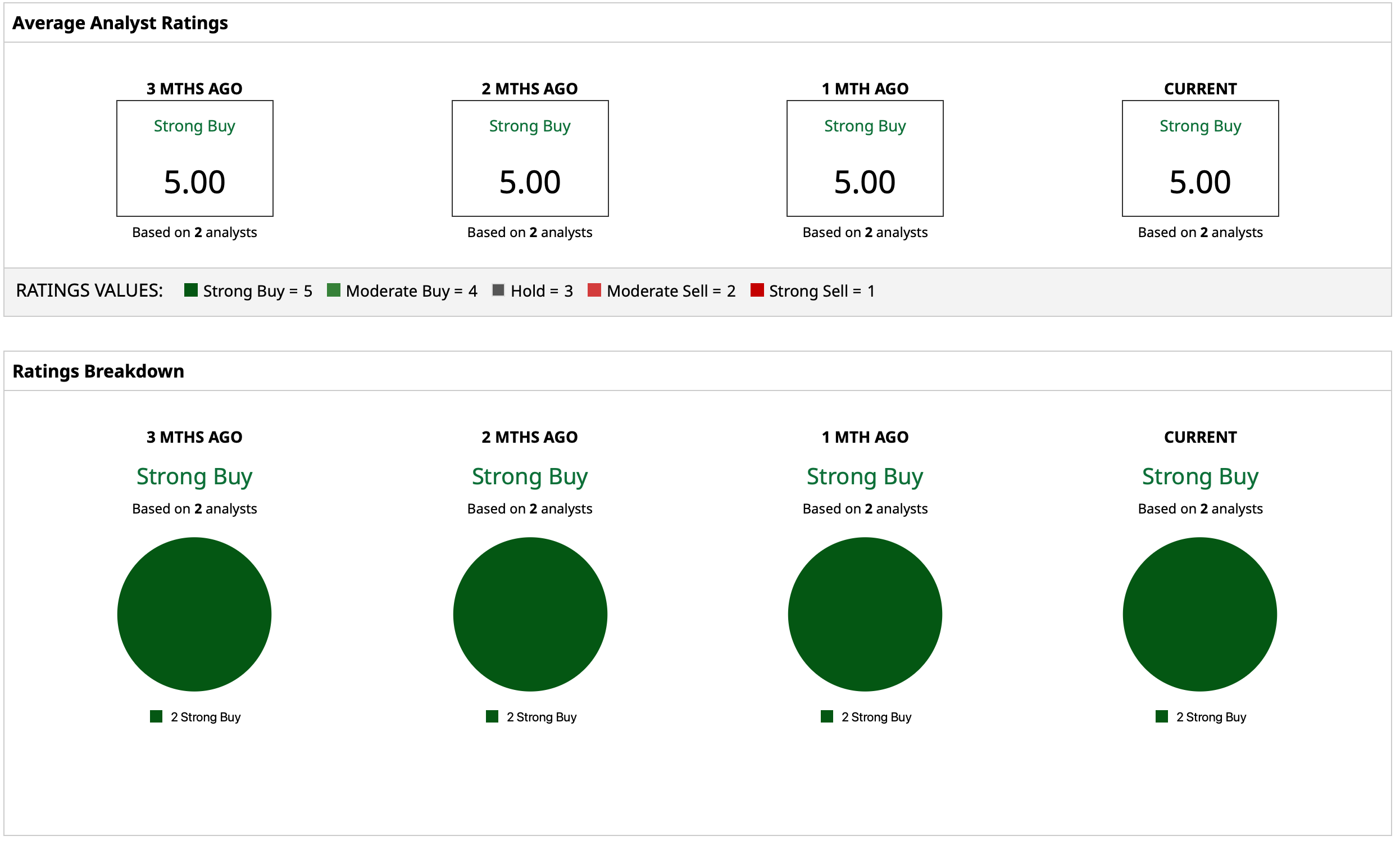

Meanwhile, two analysts covering the stock on Wall Street have unanimously deemed the ICG stock a “Strong Buy” with a mean target price of $3.50. This implies an upside potential of 96.6% from current levels.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)