/Lululemon%20Athletica%20inc_%20logo%20on%20shop%20by-%20FinkAvenue%20via%20iStock.jpg)

lululemon athletica inc. (LULU), headquartered in Vancouver, Canada, designs, distributes, and retails athletic apparel, footwear, and accessories under the lululemon brand for women and men. Valued at $20.2 billion by market cap, the company produces fitness pants, shorts, tops and jackets for yoga, dance, running, and general fitness.

Shares of this athletic apparel giant have significantly underperformed the broader market over the past year. LULU has declined 48.3% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 13.2%. In 2025, LULU stock is down 55.4%, compared to the SPX’s 14.5% rise on a YTD basis.

Narrowing the focus, LULU’s underperformance is also apparent compared to the VanEck Retail ETF (RTH). The exchange-traded fund has gained about 10.7% over the past year. Moreover, the ETF’s 11.5% returns on a YTD basis outshine the stock’s losses over the same time frame.

LULU's underperformance stems from slowing growth in North America, compressed profit margins due to higher tariff rates, and increased competition in the athleisure market. The company's product pipeline has also failed to resonate with customers, leading to decreased enthusiasm and spending. These challenges, combined with rising costs, forced LULU to trim its revenue and earnings outlook, further rattling investors.

On Sep. 4, LULU reported its Q2 results, and its shares closed down by 18.6% in the following trading session. Its EPS of $3.10 exceeded Wall Street expectations of $2.84. The company’s revenue was $2.5 billion, meeting Wall Street forecasts. The company expects full-year EPS to be between $12.77 and $12.97, and revenue to be between $10.9 billion and $11 billion.

For the current fiscal year, ending in December, analysts expect LULU’s EPS to decline 11.8% to $12.91 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

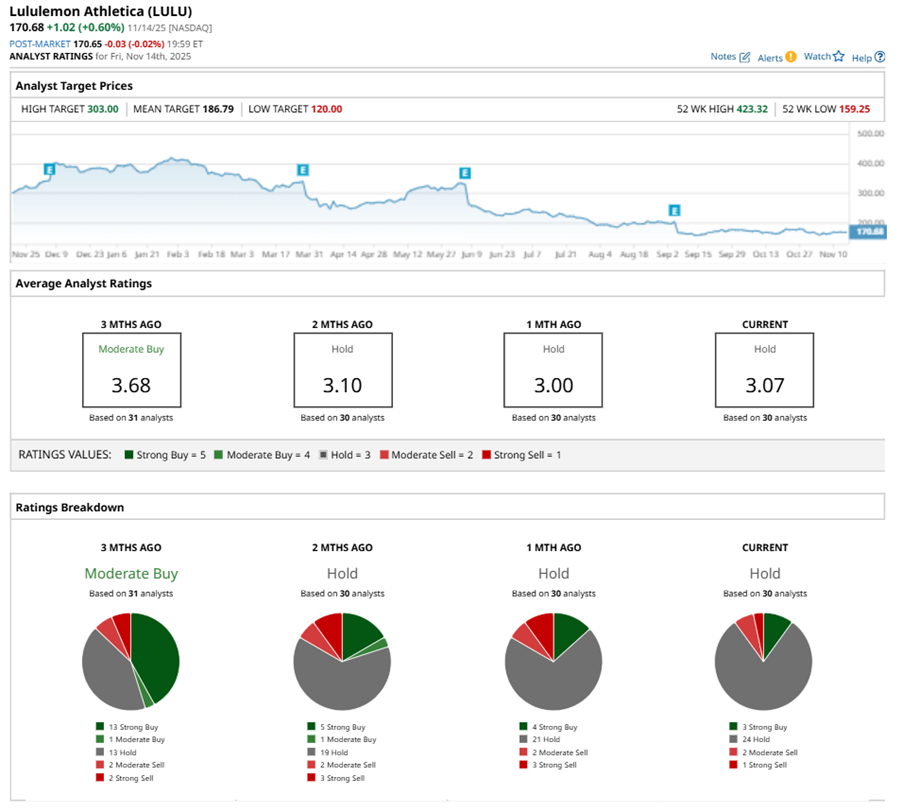

Among the 30 analysts covering LULU stock, the consensus is a “Hold.” That’s based on three “Strong Buy” ratings, 24 “Holds,” two “Moderate Sells,” and one “Strong Sell.”

This configuration is less bullish than a month ago, with four analysts suggesting a “Strong Buy,” and three advising a “Strong Sell.”

On Oct. 27, Matthew Boss from JPMorgan Chase & Co. (JPM) maintained a “Hold” rating on LULU with a price target of $191, implying a potential upside of 11.9% from current levels.

The mean price target of $186.79 represents a 9.4% premium to LULU’s current price levels. The Street-high price target of $303 suggests an ambitious upside potential of 77.5%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

/Sign%20of%20Intel%20at%20entrance%20%20by%20michaelmond.jpeg)

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)