/Incyte%20Corp_%20phone%20and%20logo-by%20T_Schneider%20via%20Shutterstock.jpg)

Valued at $20.7 billion by market cap, Incyte Corporation (INCY) is a biopharmaceutical company focused on discovering, developing, and commercializing innovative medicines, primarily in oncology and inflammation. Headquartered in Wilmington, Delaware, its flagship product is Jakafi (ruxolitinib), a leading treatment for myelofibrosis and polycythemia vera.

Shares of this biopharmaceutical behemoth have outperformed the broader market over the past year. INCY has gained 31% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 12.6%. In 2025, INCY stock is up 52.6%, surpassing the SPX’s 14.6% rise on a YTD basis.

Zooming in further, INCY has also outpaced the iShares Biotechnology ETF (IBB), that rose 13.6% over the past year. Moreover, INCY’s double-digit returns on a YTD basis outshine the ETF’s 23.5% gains over the same time frame.

On Oct. 28, INCY shares dipped 1.5% after the company released third-quarter earnings. The biotech reported $1.37 billion in total revenue, up about 20% year over year, driven by strong growth across its key products. Net product revenue rose to $1.15 billion, with flagship drug Jakafi generating roughly $791 million in sales, up 7%, and dermatology treatment Opzelura delivering $188 million, a robust 35% increase. Its non-GAAP net income per share showed a 111.2% year-over-year improvement. Despite the strong top-line momentum, the stock’s decline reflected investor caution around product concentration and future growth visibility.

For the current fiscal year, ending in December, analysts expect INCY’s EPS to grow significantly to $5.81 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in three of the last four quarters while missing the forecast on one other occasion.

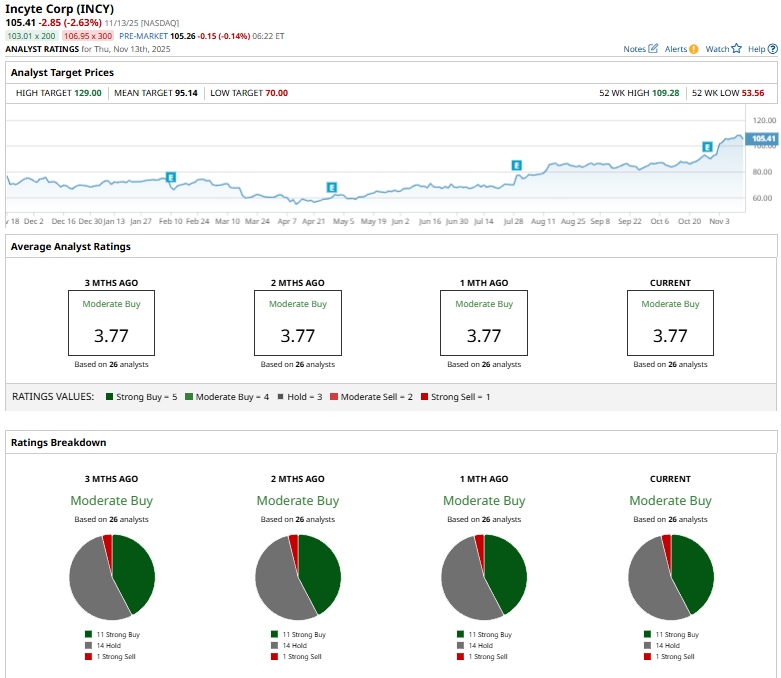

Among the 26 analysts covering INCY stock, the consensus is a “Moderate Buy.” That’s based on 11 “Strong Buy” ratings, 14 “Holds,” and one “Strong Sell.”

This configuration has been consistent over the past few months.

On October 15, UBS analyst Ashwani Verma reiterated a “Hold” rating on Incyte and set a $76 price target.

While INCY currently trades above its mean price target of $95.14, the Street-high price target of $129 suggests a 22.4% upside potential.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Abbott%20Laboratories%20vials%20and%20Logo-by%20Melniov%20Dmitriy%20via%20Shutterstock.jpg)

/Intuit%20Inc%20logo-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)