/Quantum%20Computing/A%20concept%20image%20of%20a%20green%20and%20yellow%20motherboard_%20Image%20by%20Gorodenkoff%20via%20Shutterstock_.jpg)

The AI boom has already turned many pick-and-shovel investors into millionaires over the past three years. Semiconductor companies have benefited the most, and software companies involved with AI have also driven significant gains. However, there are other industries that are just as essential for AI but don't get as much love.

Memory chips, cooling systems, wafer tools, and the other unglamorous bits of infrastructure are becoming the bottleneck that decides how fast the entire industry can grow. In that sense, the AI build-out looks less like a single gold mine and more like the old California rush, where the steady fortunes were made by the merchants who sold picks and shovels to every hopeful prospector.

DRAM (dynamic random-access memory) and NAND flash (a semiconductor that stores data) are two key bottlenecks. AI companies need oceans of both for their AI GPUs and broader operations.

Citi now expects both DRAM and NAND flash to be in undersupply through at least 2026, arguing that production discipline and exploding data-center demand have set the stage for a multi-year pricing tailwind.

Here are two stocks that are well-positioned to benefit from this:

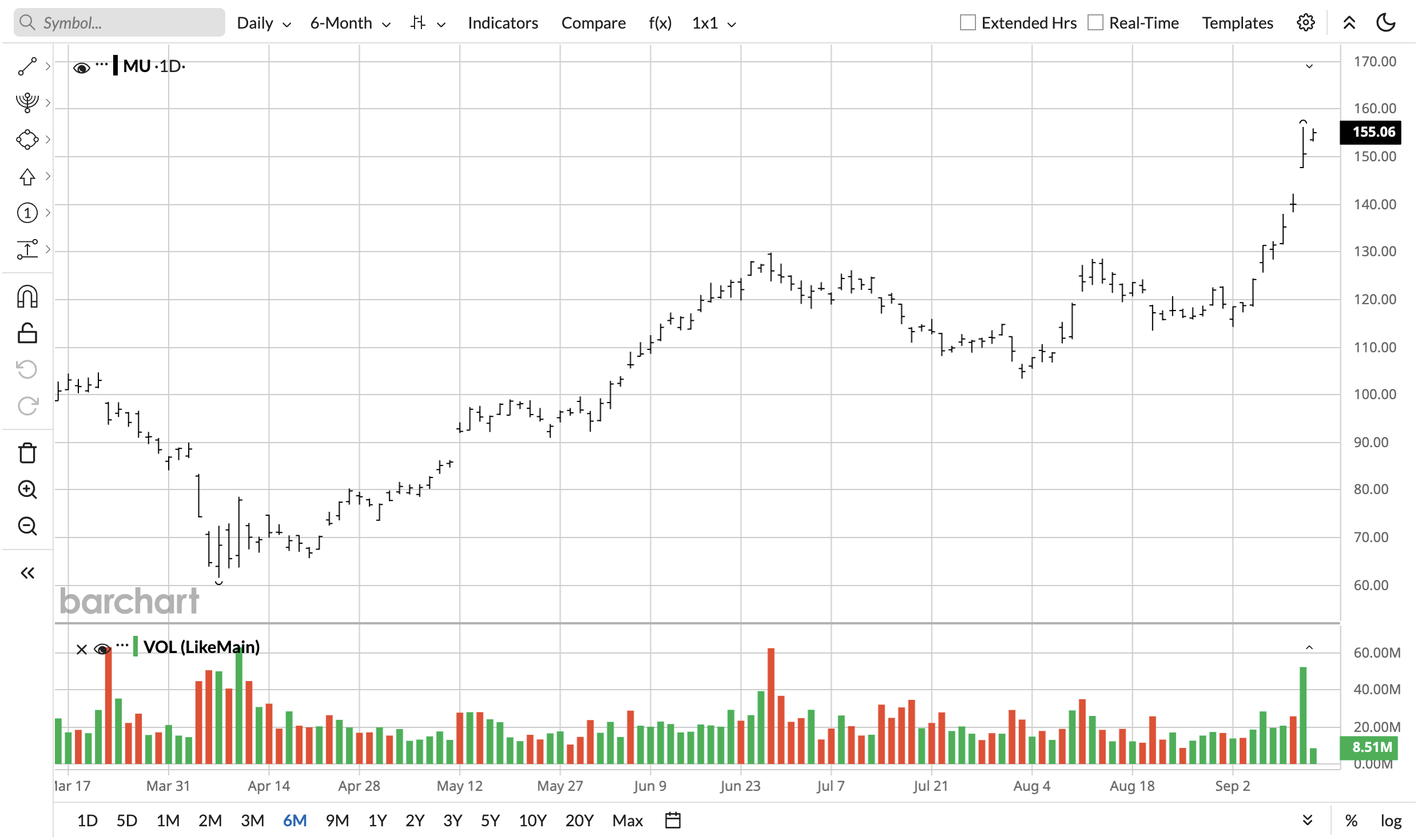

Micron (MU)

Micron Technology (MU) is no longer the boom-bust play. Memory stocks were once seen as highly cyclical and volatile, but that may be about to change as AI companies shift from training to inferencing. This will require massive amounts of data, and Micron is one of the few major beneficiaries.

This company makes both DRAM and NAND flash. Most of its competition comes from abroad, mainly from SK Hynix and Samsung (SMSN.L.EB), both from South Korea. Micron is the only major domestic producer that has a large market share, and with the current administration in charge, this is very bullish. Tariffs levied on these products will directly translate into a boost for Micron.

MU stock has surged by 18.8% in just the past five days. Q3 FY 2025 revenue grew 15% sequentially and 37% year-over-year (YoY) to $9.3 billion. DRAM constituted 76% of that, with NAND being responsible for 23%. ~99% of its revenue is locked in two fields that are expected to see shortages. This is already translating into pricing power, with operating income jumping from 13.8% in Q3 2024 to 26.8% in Q3 2025.

Citi has hiked its price target for MU stock to $175.

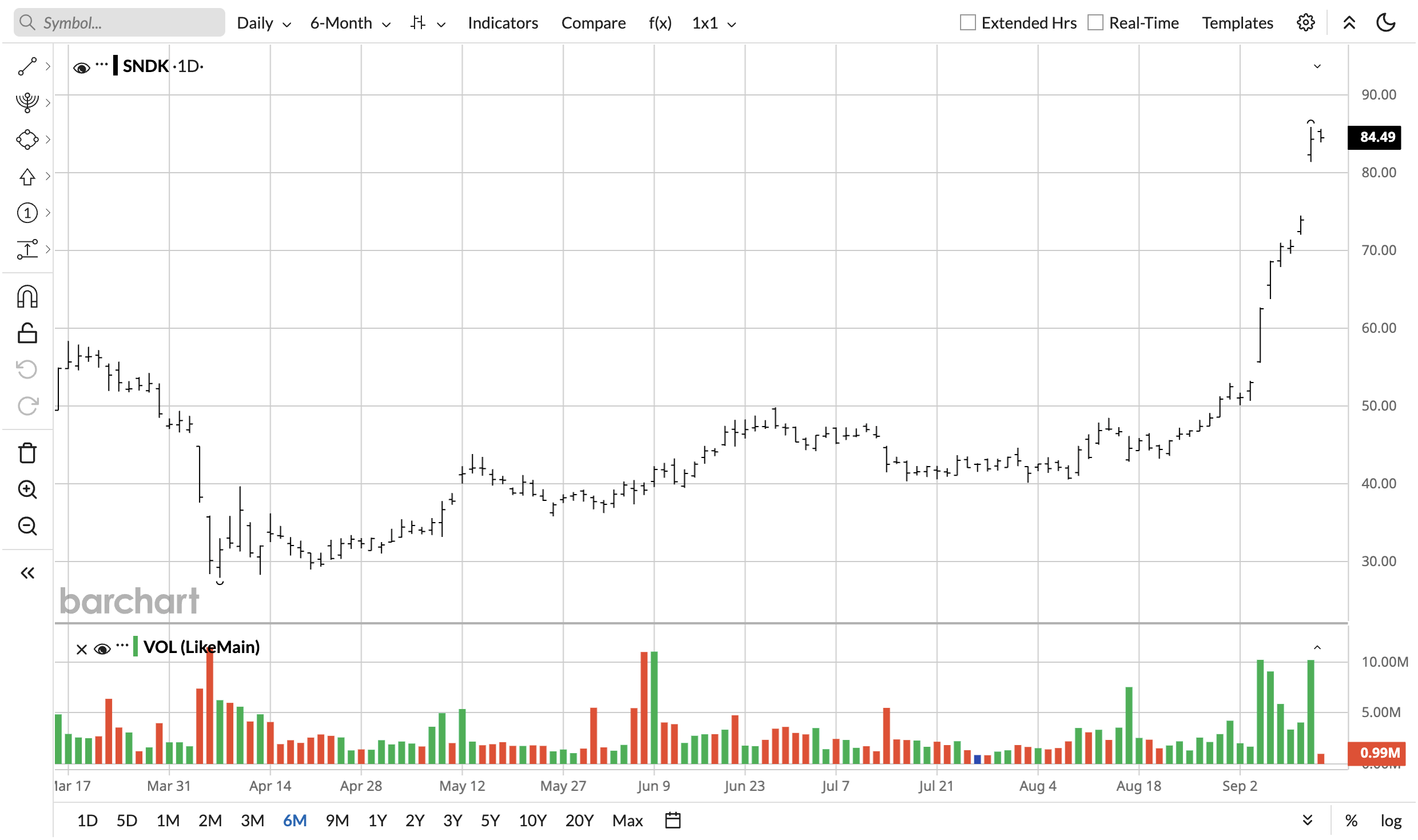

SanDisk (SNDK)

SanDisk (SNDK) recently separated from Western Digital (WDC) earlier this year. SNDK stock is now a pure-play NAND flash company. The entire focus is on growing its market share over this segment, and with the tide rising, SanDisk could be one of the first to be lifted. The stock is up 20.5% in the past five days.

Q4 FY 2025 revenue grew 12% sequentially and "above the guidance range," though revenue was up 8% YoY. Gross margin and operating income declined due to severe pricing pressure from market oversupply. Plus, a "mini-NAND glut" also contributed to the decline, along with a goodwill impairment charge of $1.83 billion.

Regardless, with AI companies shifting to inferencing and hyperscalers increasing CapEx, these trends are expected to be reversed.

Morgan Stanley now projects that AI inference will create an incremental $29 billion addressable market by 2029. It also named SanDisk a “Top Pick” and hiked the price target to $96. Citi has named it one of the leading potential beneficiaries of a NAND shortage. Its price target is at $80.

On the date of publication, Omor Ibne Ehsan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)