/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

Memory and storage giant Micron Technology (MU) has been one of the standout beneficiaries of the artificial intelligence (AI) boom, delivering massive triple-digit gains so far in 2026. Now, the red-hot chip stock is back in focus after the company announced a series of strategic customer agreements aimed at expanding its presence in the rapidly evolving automotive technology market. On Thursday, Micron revealed strategic customer agreements (SCAs) with several major automotive and technology players, including Qualcomm (QCOM), Visteon (VC), Harman, JOYNEXT, Denso, Astemo, and Hyundai Mobis.

The partnerships come as increasingly connected and intelligent vehicles require more advanced memory and storage solutions to power everything from sophisticated infotainment systems to AI-enabled features. Micron Chairman, President, and CEO Sanjay Mehrotra emphasized that memory and storage will play an increasingly important role as vehicles become smarter and more technologically advanced. He noted that the new agreements should help ensure next-generation automotive platforms have the capabilities needed to support richer, safer, and more intelligent in-vehicle experiences. With Micron already riding strong AI-driven demand and now deepening its ties across the automotive ecosystem, could this latest development add another catalyst to MU stock?

About Micron Stock

Micron Technology has been around for nearly five decades, but the AI boom has thrust the memory chipmaker into a new era of growth. Founded in 1978 and headquartered in Idaho, Micron is one of the world’s largest memory and storage companies, producing DRAM, NAND, and NOR products that sit inside everything from smartphones and personal computers to data centers, vehicles, and industrial equipment. At its core, Micron’s business revolves around one of the digital economy’s most basic needs: storing, processing, and moving enormous amounts of data.

That role has become increasingly important with the rapid adoption of AI, which requires vast computing resources and significantly more advanced memory infrastructure. Micron’s products support compute-intensive AI workloads, cloud infrastructure, and next-generation data centers, while its presence across PCs, mobile devices, and other connected systems extends its reach from centralized data centers all the way to the intelligent edge.

By focusing on technology development, advanced manufacturing, operational efficiency, and products designed around customer requirements, Micron has positioned itself as an important supplier to the expanding AI-driven data economy. And investors have certainly taken notice. Now valued at $963.59 billion, Micron has delivered one of the market’s most remarkable rallies over the past year. Surging demand for memory and storage products amid the global AI infrastructure buildout has helped propel MU stock an eye-popping 669.3% over the last 12 months.

The momentum carried into 2026, with the shares climbing another 205.3% year-to-date (YTD). Those gains have left the broader market far behind. By comparison, the S&P 500 Index ($SPX) has returned 18.5% over the past 12 months and 9% so far this year. Recently, however, Micron’s seemingly unstoppable rally has hit a rough patch. After soaring to an all-time high of $1,255 on June 25 following the company’s blockbuster fiscal third-quarter earnings report, MU shares have retreated 31.7%.

The selling has accelerated over the past five trading days, with the stock dropping 11% despite Micron announcing a series of strategic customer agreements designed to strengthen its position in the rapidly evolving automotive technology market. The pullback is not being driven by a single concern. A broader semiconductor sector sell-off has weighed on sentiment, while investors are also grappling with fears that the memory market could eventually face oversupply.

Add to that questions about a potential slowdown in AI infrastructure spending and intensifying competition from Chinese memory manufacturers such as ChangXin Memory Technologies, and traders suddenly have several risks to consider. That leaves investors facing a familiar dilemma after MU’s spectacular run. For some, the recent slide may be a reason to remain cautious and wait for greater clarity around the memory cycle and AI spending. For others, a near 32% retreat from record highs could make one of the AI sector’s strongest-performing stocks look considerably more interesting at its reduced valuation.

Inside Micron’s Q3 Earnings Report

Micron’s latest quarterly results offered a clear indication that the AI-driven memory boom still has plenty of momentum. Demand for memory and storage products used in AI infrastructure continues to run well ahead of available supply, keeping pricing conditions favorable and providing a powerful tailwind for the company. Micron’s fiscal third-quarter 2026 results, released on June 24, put the scale of that demand into perspective, with record-breaking figures that easily surpassed Wall Street’s forecasts. Investors responded enthusiastically, sending MU shares 15.74% higher in the next trading session.

At the center of the report was another revenue milestone. Micron generated a record $41.46 billion in quarterly sales, extending its streak of record revenue to five consecutive quarters. That represented a remarkable 74% increase from the previous quarter and a 346% surge from the $9.30 billion reported in the year-ago period. The figure also came in comfortably ahead of analysts’ consensus estimate of $36.72 billion, underscoring the extraordinary impact that rising AI-related demand is having on Micron’s business.

The improvement was not limited to revenue as Micron reached new levels of profitability, supported by favorable pricing and a growing contribution from its next-generation memory products. Non-GAAP gross margin climbed to a company-record 84.9%, the highest level in Micron’s history. That helped drive non-GAAP net income to $28.86 billion, while adjusted earnings per share (EPS) reached $25.11, an increase of more than 1,000% from the prior-year period. The result once again sailed past Wall Street’s expectations, with analysts forecasting EPS of $21.39.

Much of that growth is coming from the data center, where the rapid expansion of AI workloads is creating enormous demand for high-performance memory and storage. Micron’s combined Cloud Memory and Core Data Center business units generated more than $25 billion in revenue during the quarter, translating into an annualized revenue run rate exceeding $100 billion. Meanwhile, quarterly Data Center SSD revenue topped $5 billion and more than doubled sequentially, as hyperscalers and enterprise customers continued ramping up investments in AI infrastructure.

The strength extended across Micron’s broader product portfolio as well. DRAM revenue climbed 67% from the previous quarter to $31.3 billion and represented 76% of the company’s total revenue. NAND delivered an even sharper sequential increase, with revenue jumping 99% to $9.9 billion. More importantly for Micron’s longer-term outlook, management indicated that industry demand for both DRAM and NAND remains significantly higher than available supply.

The company expects these tight supply-demand conditions to continue well beyond calendar 2027, supported by accelerating AI adoption across industries and by structural constraints that limit the availability of new memory supply. Micron’s guidance suggests management sees little reason to expect the momentum to fade in the immediate future. For the fiscal fourth quarter of 2026, the company is forecasting revenue of $50 billion, plus or minus $1 billion, along with a non-GAAP gross margin of approximately 86%. This quarter's adjusted EPS is expected to come in at $31.17, pointing to another quarter of exceptionally strong profitability as it climbs 990%.

What Do Analysts Think About Micron Stock?

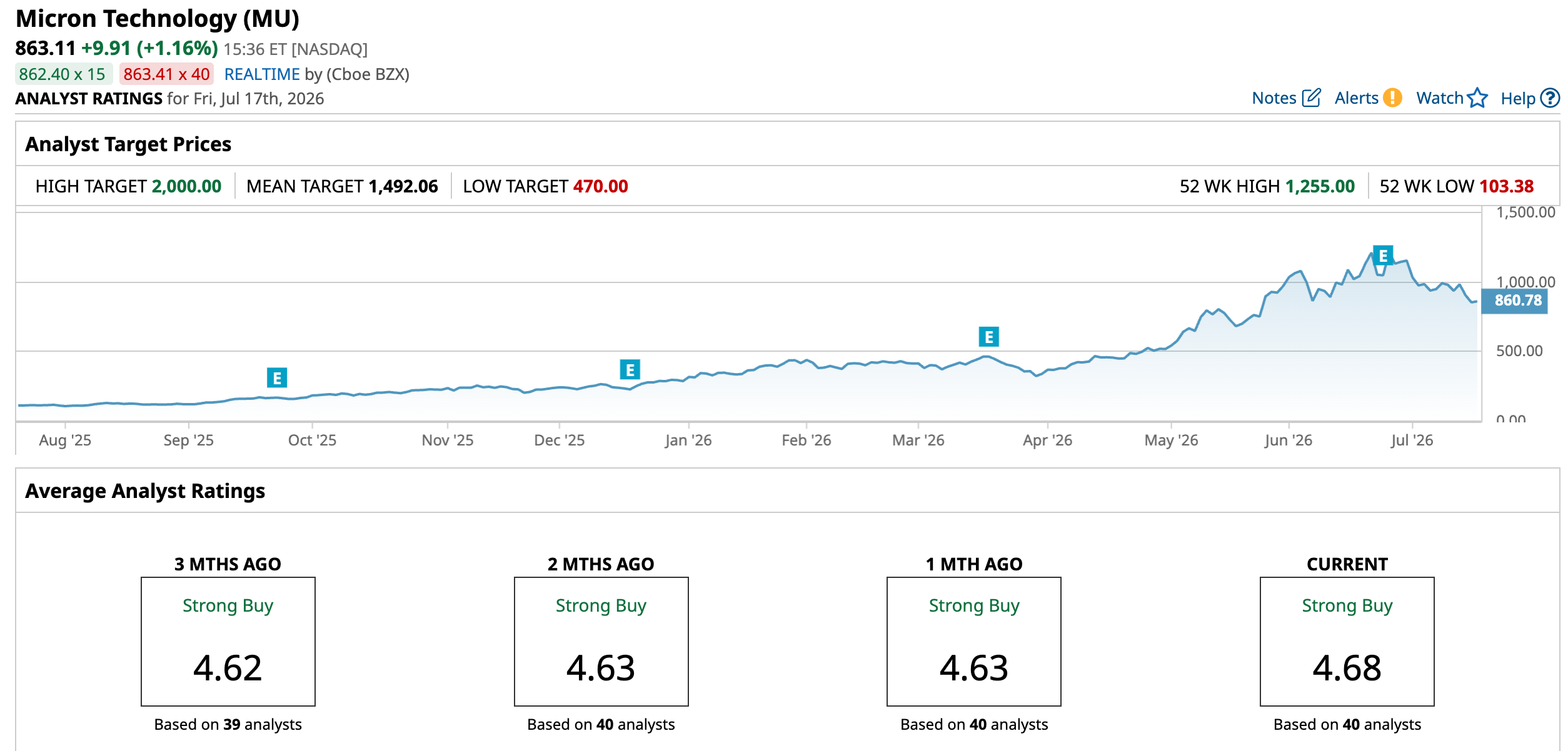

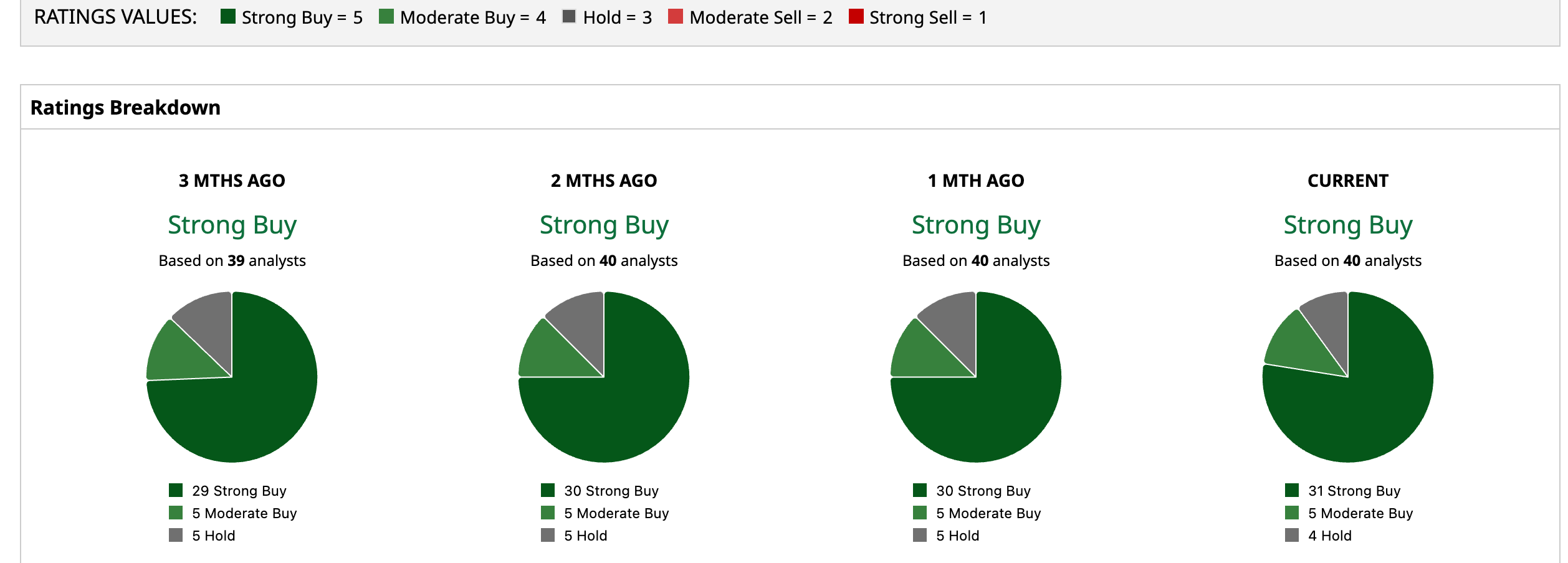

Despite Micron’s recent pullback, Wall Street remains firmly in the bull camp. MU carries a consensus “Strong Buy” rating, with 31 of the 40 analysts covering the stock recommending a “Strong Buy,” five assigning it a “Moderate Buy,” and four opting for a “Hold.” The price targets are even more striking. The average target of $1,492.06 points to 72.9% upside from current levels, while the Street-high forecast of $2,000 suggests MU could rally as much as 131.7%.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)