Aehr Test Systems (AEHR) stock pushed higher after the semiconductor equipment manufacturer delivered a remarkable Q4 earnings report on Tuesday evening.

The company reported adjusted earnings of $0.11 per share, dramatically surpassing the consensus estimate for a loss of $0.01, while revenue of $18.84 million exceeded the $18.69 million forecast and represented a 34% year-over-year increase from $14.09 million.

Including the post-earnings rally, AEHR shares are trading at more than 4x their price at the start of this year.

Aehr Stock Soars on Solid Backlog

The most compelling aspect of the report was not the quarterly beat itself but the extraordinary forward guidance.

Management issued fiscal 2027 revenue guidance of $140 million, representing growth of about 180% over last year’s revenue of $50 million and crushing the consensus estimate of roughly $85 million.

The company also projected non-GAAP pretax net income margins of 18% to 22% of total revenue for fiscal 2027.

Record quarterly bookings of $60.7 million — up more than 500% from $11.1 million in the prior-year quarter — underpinned the bullish outlook. The backlog hit a record $80.6 million as of May 29, and the effective backlog, including bookings received after that date, climbed to $100.6 million.

This level of visibility into future revenue provides substantial credibility to what otherwise might appear to be an overly ambitious guidance range.

What Has Driven AEHR Shares Higher in 2026?

Aehr Test Systems has undergone a dramatic transformation in its revenue mix.

Two years ago, over 95% of the company’s business was tied to silicon carbide testing for electric vehicles (EVs), whereas nearly 95% of fiscal 2026 revenue came from markets outside EV silicon carbide.

Artificial intelligence (AI) processors, CPUs, and network processors now represent roughly 71% of annual revenue, with silicon photonics and data center infrastructure applications accounting for about 20%.

AI and silicon photonics burn-in made up more than 80% of fourth-quarter revenue specifically.

Management highlighted that its lead AI wafer-level customer has moved all production burn-in screening to wafer level on Aehr systems and is forecasting higher capacity needs.

AEHR also completed a benchmark test with a key supplier of AI accelerators, CPUs, and network processors, producing results that exceeded customer expectations. In package-level burn-in, the lead hyperscale customer is expanding Sonoma system purchases for a second device with twice the power of the first.

How Wall Street Recommends Playing Aehr Test Systems

From a financial health perspective, Aehr Test Systems ended Q4 with $116.5 million in cash and equivalents, up sharply from $37.1 million at the end of the previous quarter and $26.5 million at the end of fiscal 2025.

Non-GAAP gross margin improved to 45% in the fourth quarter — up 1,000 basis points from 35% in the year-ago period — suggesting strong operating leverage as volumes scale.

The full fiscal year was more modest, with revenue of $50 million representing a 15% decline year-over-year and full-year non-GAAP net income of just $0.9 million.

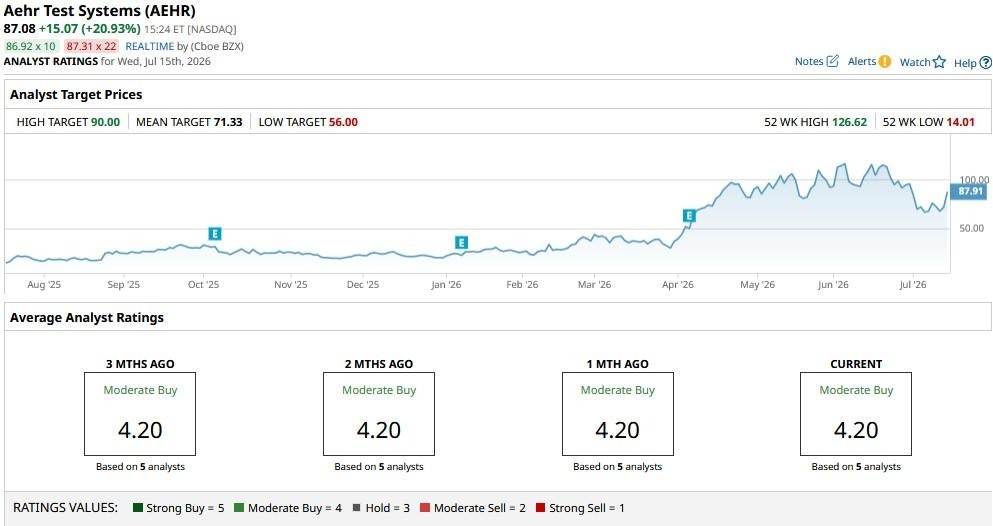

That said, Wall Street currently sees AEHR stock as overvalued. While the consensus rating on the firm remains at “Moderate Buy,” the mean price objective of about $71 signals significant downside from here.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)