Bank earnings season is back, and JPMorgan Chase & Co. (JPM) just set the tone. The bank reported its Q2 2026 results on July 14, and the numbers were stronger than most expected a month ago.

JPMorgan Chase & Co. posted GAAP EPS of $7.70, beating estimates by 31.7% and well above the $5.24 from a year ago. Still, the stock fell about 2% in pre-market trading after the bank raised its 2026 expense outlook to $107.5 billion from $105 billion.

The stock had already been running up into the report, trading close to its 52-week high of $343.45. As the first major bank to report each quarter, JPM often sets the tone for the sector. It also continues to offer a solid dividend, with a $6.00 annual payout and a yield around 1.75%, backed by strong earnings and capital.

Now that earnings are out, where does JPMorgan Chase & Co. go next, and is the dividend enough reason to stay invested if upside looks limited?

Inside JPMorgan’s Latest Financials

JPMorgan Chase & Co. is a broad financial services company with businesses across consumer banking, investment banking, trading, asset management, and payments. It makes money from both interest income and fees, which helps keep things balanced.

The stock has been steady, up 21% over the past year and 7.57% year-to-date (YTD).

It is not cheap though, trading at a forward price-to-earnings ratio of 14,66 times versus the sector average of 11.34 times, showing investors are willing to pay a premium for its size and consistency.

For income investors, the appeal is clear. JPMorgan Chase & Co. pays a $6.00 annual dividend with a 1.75% yield, and the payout ratio is just 26.36%, leaving plenty of room for coverage. The bank has raised its dividend for 15 straight years and last paid $1.50 per share on July 6. It also approved a new $50 billion buyback program in late June and lifted its dividend by 10% after clearing the Federal Reserve stress test.

The latest quarter backs all of this up. Revenue came in at $58.02 billion, up 27% year-over-year (YOY) and 13% above estimates, helped by strong equities trading. EPS was $7.70, beating expectations by 31.7%, while net income rose 41% to $21.2 billion, supported by gains from Visa shares and other investments.

Net interest income grew 9.9% to $25.6 billion but came in slightly below estimates as lower rates weighed on margins. Noninterest revenue jumped 45% on stronger investment banking and asset management fees. Expenses rose 15% to $27.3 billion due to higher pay, tech spending, and expansion, while credit costs stayed under control, with provisions at $2.5 billion and only a modest reserve build.

What’s Driving JPMorgan’s Growth Engine?

JPMorgan Chase & Co. is pushing its brand onto a bigger global stage through a new partnership with the International Olympic Committee. It is now the first-ever Global Banking Partner of the Olympic Games, covering Los Angeles 2028 and the French Alps 2030. The deal also makes it the official bank of Team USA and a founding partner of the LA28 Games, putting the company at the center of large global events tied to payments and cross-border activity.

At the same time, JPMorgan Chase & Co. is moving deeper into crypto through its partnership with Coinbase (COIN). Chase customers will be able to link their bank accounts directly to Coinbase wallets using the bank’s API. They can also transfer Ultimate Rewards points into Coinbase at a 1:1 value and, starting this fall, use Chase credit cards to fund crypto accounts. This gives the bank a clearer role in helping customers move money into digital assets.

At the same time, the bank is still investing in its physical network. It plans to open more than 160 new branches across over 30 states in 2026 and renovate nearly 600 locations. The focus is on expanding into underserved and fast-growing areas, including rural and lower-income communities, which supports deposit growth and brings in new customers across the largest branch network in the U.S.

In summary, this mix gives JPMorgan a real shot at a stronger future.

Wall Street’s Take on JPM Now

Wall Street still leans positive on JPMorgan Chase & Co. Analysts expect EPS of $5.50 for the September 2026 quarter, up from $5.07 a year ago, which is 8.48% growth. For the full year, earnings are seen at $22.82, up 12.19% from $20.34, pointing to solid but steady growth.

Evercore ISI raised its price target to $340 from $320 on April 20 and kept an “Outperform” rating, pointing to strong trading as the main driver. On June 26, Truist Securities’ John McDonald increased his target to $344 from $332 but kept a “Hold,” saying the stock has already earned its premium thanks to strong returns and fee income, even if upside looks limited near term.

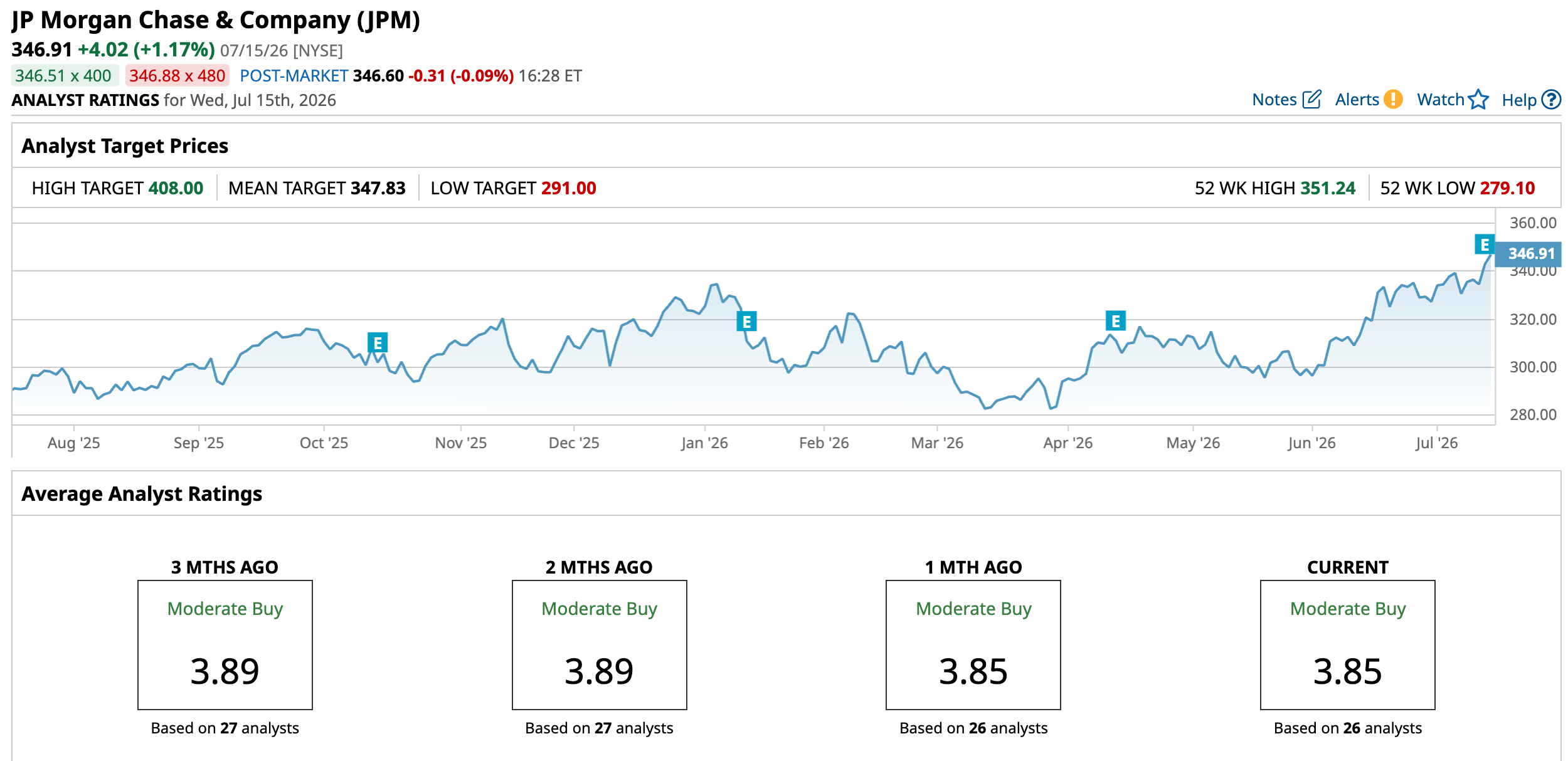

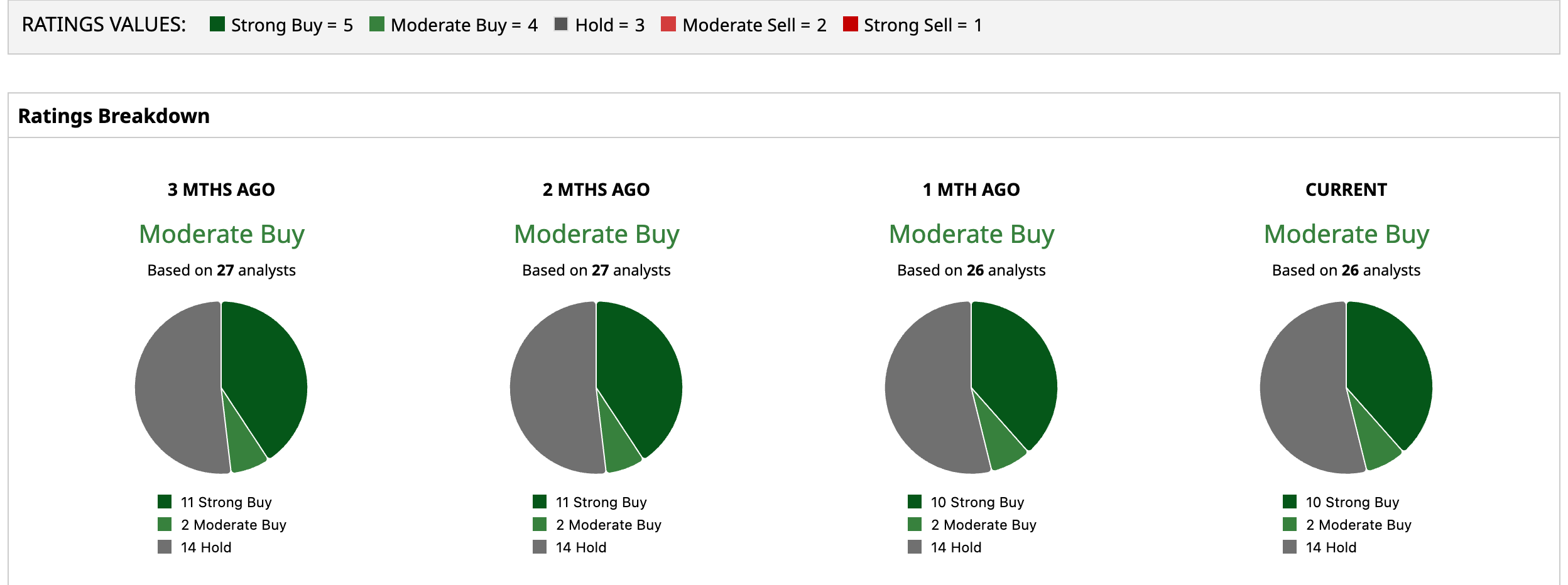

Overall, sentiment is still supportive. Of 26 analysts covering the stock, a consensus gives a rating of “Moderate Buy,” with an average price target of $347.83. From current levels, that suggests a marginal upside of 0.27%. But the Street-high price target of $408 suggests that JPM stock could rally 17.6% over the following 12 months.

Conclusion

JPMorgan still looks like a hold rather than a chase at these levels. The dividend is clearly secure, backed by strong earnings, a low payout ratio, and ongoing buybacks, which makes it appealing for income-focused investors. But with the stock already near highs and showing very little implied upside, most of the near-term good news appears priced in. The most likely path from here is a period of consolidation, with modest gains tied to earnings growth rather than multiple expansion, unless a new catalyst meaningfully shifts expectations.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)