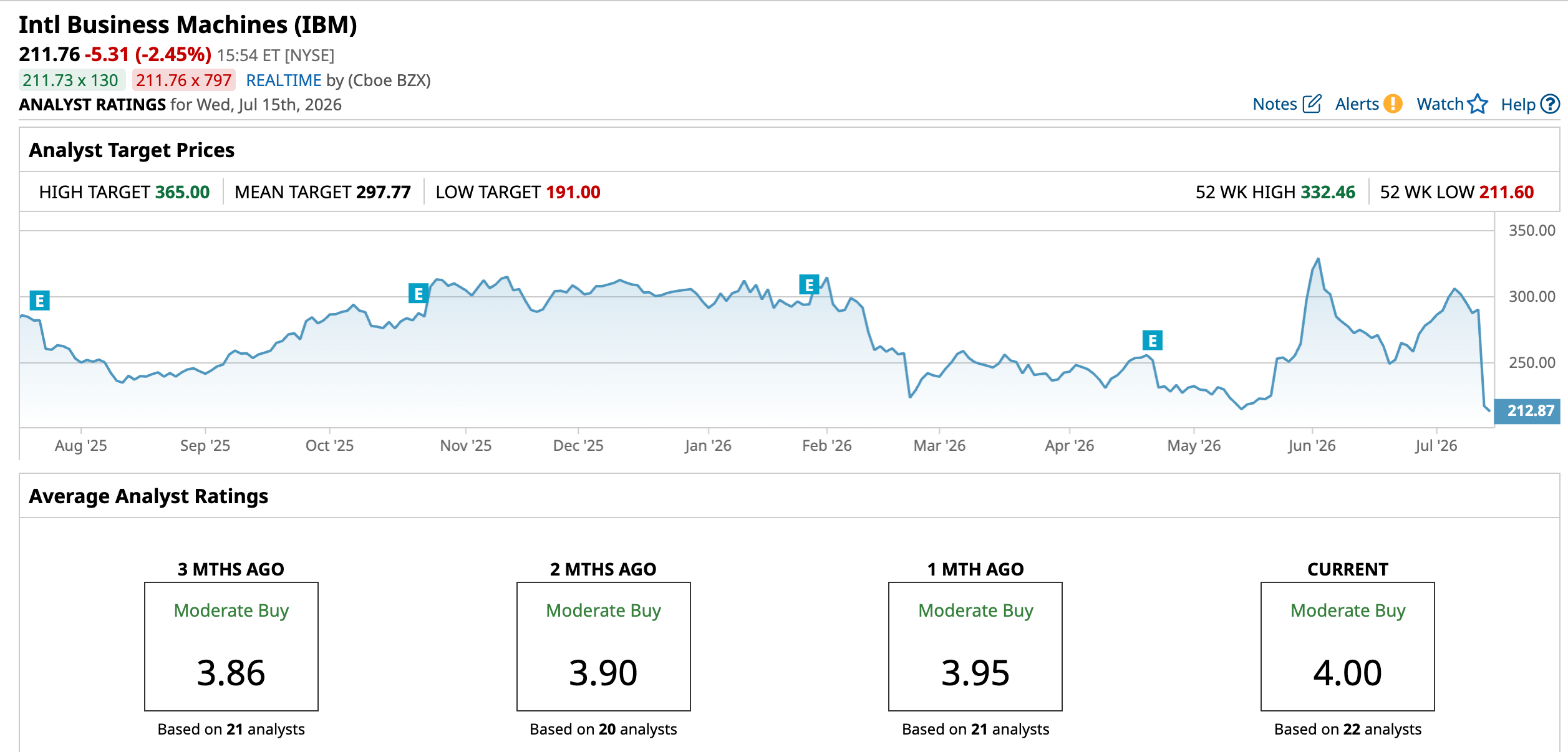

International Business Machines (IBM) delivered a real shock to the market on July 14, 2026. The stock sank more than 25% in a single day after the company warned that its preliminary Q2 results would come in weak. That kind of move is almost unheard of for a company this size and marks its worst one-day drop in decades, even worse than what investors saw around Black Monday in 1987.

Their preliminary revenue for the quarter was $17.2 billion, up just 1% from a year earlier and about $660 million below what Wall Street was anticipating. That’s a sharp contrast to Q1 2026, when revenue grew about 9% year-over-year (YOY) to $15.92 billion and topped expectations.

CEO Arvind Krishna didn’t try to dress it up. He admitted the company had “faltered,” pointing to clients shifting spending, cybersecurity issues, and big deals slipping later than planned.

The nasty sell-off even sparked a new securities fraud investigation into whether management painted too rosy a picture of its deal pipeline.

After a hit like that, investors are left with a simple but tough question. How do you trade or invest in IBM from here?

IBM’s Financial Numbers

Intl Business Machines (IBM) is a long-standing tech company based in Armonk, New York. It sells hybrid cloud services, AI and automation software, consulting, and core systems that big companies and governments rely upon every day.

The stock is down 28.1% year-to-date (YTD) and 24.6% over the past 52 weeks.

IBM trades at a trailing price-to-earnings ratio of 18.27 times versus a sector median of 26.11 times, and a price‑to‑cash‑flow of 16.94 times versus 18.88 times for the sector, with a market cap of $204 billion and a forward annual dividend of $6.76, or a 2.33% yield.

Their Q1 earnings history showed numbers that were still holding up before the profit warning. This was the case in the quarter ending March 2026, when EPS came in at $1.91 versus a $1.81 forecast, a 5.52% beat.

The same period delivered sales of $15.9 billion, but that was actually a drop of 19.15% YOY, and net income was roughly $1.2 billion, down 78.29%.

Their cash flow tells a similar story. This March 2026 stretch saw operating cash flow of $5.17 billion, down 60.82%, and net cash flow of -$2.78 billion, a swing of -434.04%.

IBM’s second‑quarter preview just made that tension more obvious. Their Q2 2026 revenue is expected at $17.2 billion, up only 1% and below the $17.85 billion consensus, while operating non‑GAAP EPS is guided to $2.93 versus a $3.02 estimate. It shows that the momentum hinted at in March has already faded.

IBM’s Long-Term AI Story

IBM’s growth story right now is tied to four clear areas: AI, cloud, security, and chips. IBM has rolled out new Power systems and software aimed at large enterprises that need to manage risk better, improve productivity, and keep flexible IT setups that mix on-site and cloud. These systems use the newer Power11 processors, refreshed hardware, and updated virtualization tools, and they can run either in customer data centers or inside IBM’s own cloud.

In June, IBM also struck a strategic AI deal with Alphabet's (GOOGL) Google Cloud. A dedicated Google Cloud group inside IBM Consulting will help clients build and run AI agents using Google’s Gemini models, tied into IBM’s WatsonX data and AI platform.

On security, IBM has tightened its links with OpenAI. The company joined the OpenAI Daybreak Cyber Partner Program and launched new application security services that use OpenAI models to automatically find and confirm software vulnerabilities.

Chips are the last piece. IBM has unveiled what it calls the world’s first sub-1-nanometer chip at the 0.7-nanometer node. The design fits nearly 100 billion transistors onto a fingernail-sized chip using a new 3D nanostack layout, and it aims for up to 50% better performance or up to 70% lower power use than IBM’s older 2-nanometer technology.

Put simply, the near-term financials look bruised, but this mix still gives IBM a real shot at a stronger future.

Analysts Still See Upside Despite the Shock

IBM’s next big test is just around the corner. The company is set to report earnings on July 22 after the close, and the Street is looking for EPS of $3.02 for the June 2026 quarter, up from $2.80 a year earlier. That works out to 7.86% growth, and that is the hurdle IBM now has to meet or at least come close to.

Before the sell-off, some well-known tech analysts were clearly in IBM’s camp. Dan Ives, head of technology research at Wedbush, recently raised his price target from $320 to $350. At today’s levels, that target implies 65.7% upside.

That view has support elsewhere. Barclays analyst Raimo Lenschow started coverage on IBM with an “Overweight” rating and also suggested the shares could reach $350 by year-end.

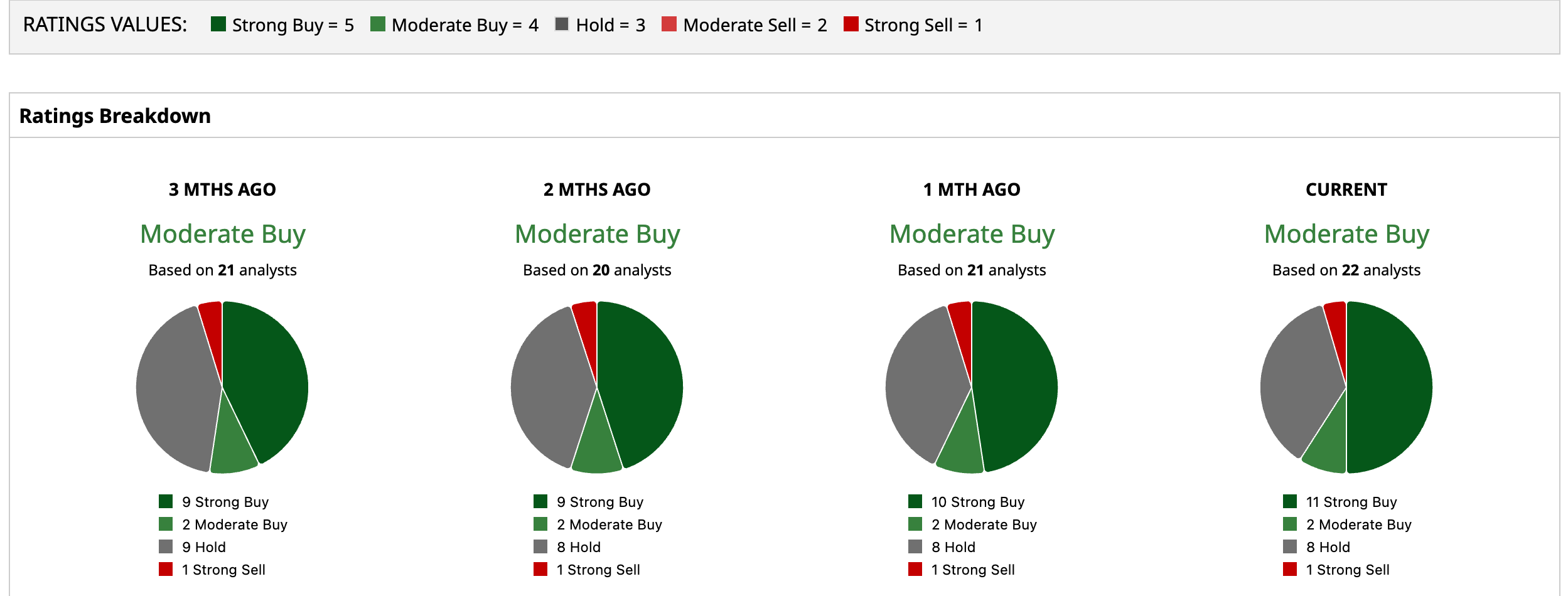

Across the broader analyst community, the tone is cautiously positive instead of outright bearish. A group of 22 analysts has settled on a consensus rating of “Moderate Buy.” Their average price target sits at $297.77, which implies 40.6% upside from here.

Conclusion

IBM just had one of its worst weeks in decades, and that alone tells you the market no longer gives it the benefit of the doubt after an earnings miss. Yet estimates still call for EPS growth, and the average analysts’ target is near $300. The smart move now is to treat IBM as a cautious buy on weakness for patient investors and a clear avoid for anyone who needs clean momentum or flawless execution in the next couple of quarters.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.