/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

SpaceX Corporation (SPCX) investors have a major date circled on the calendar right now. On July 16, the company is scheduled to launch Starship Flight 13, a mission that could become the stock's biggest catalyst since its blockbuster IPO just over a month ago.

The launch isn't just another test. For the first time, Starship will attempt to deploy 20 commercial Starlink V3 satellites, marking an important step toward regular commercial operations. A successful mission could help restore investor confidence after weeks of heavy selling, while another setback may add to the pressure on shares.

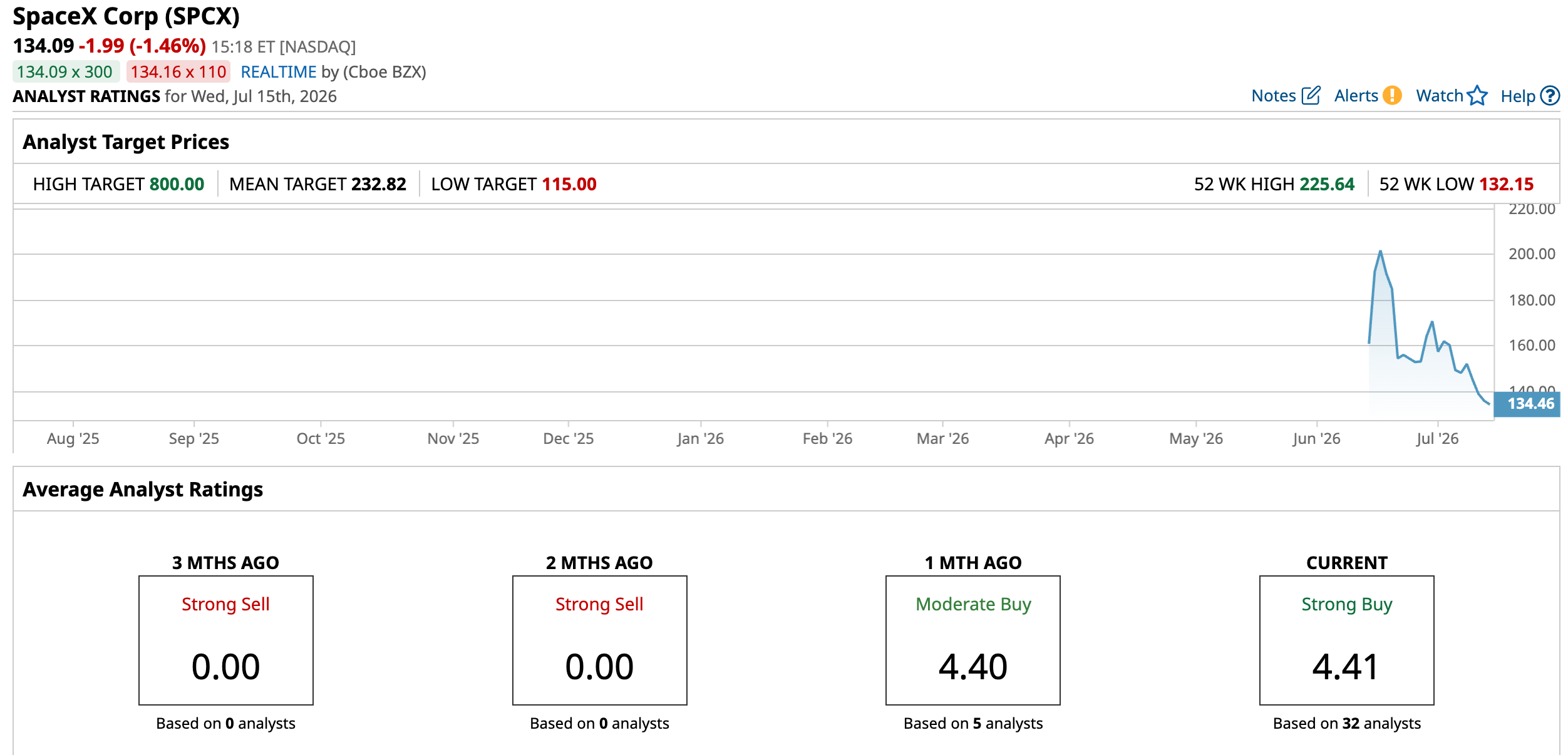

SpaceX stock has been extremely volatile since going public. Shares debuted at $150 after pricing at $135 in June, surged above $225 during the first week, and have since retreated 29.5%, sinking to its lowest price today since its IPO Debut. This is happening as investors shift their focus from IPO excitement to the company's steep losses, aggressive spending, and premium valuation.

The stock currently trades at roughly 110 times expected trailing 2025 revenue of $18.7 billion, far above the aerospace and defense industry's average of 2.5 times to 3 times sales. Even after losing hundreds of billions of dollars in market value, investors are still paying a premium for the company's long-term growth story rather than its current financial performance.

Starship Flight 13 Could Be a Defining Moment

The July 16 mission is particularly important because it represents the second test of the new Starship V3 design after the first V3 launch ended with an explosion following splashdown in May.

SpaceX says Flight 13 includes software upgrades designed to address issues from the previous mission. Beyond testing the vehicle itself, the company will deploy 20 next-generation Starlink satellites, including six equipped with cameras to monitor the spacecraft's heat shield during reentry.

If the mission succeeds, investors may gain confidence that Starship is moving closer to commercial service, unlocking new revenue opportunities across satellite deployment, lunar missions, and eventually Mars exploration. Another failure, however, could reinforce concerns about execution risks at a time when investor sentiment is already fragile.

Quarterly Results Show Strong Growth but Massive Losses

SpaceX's first earnings report as a public company highlighted both the opportunity and the risks facing investors.

For the first quarter of 2026, the company generated $4.69 billion in revenue, an increase of 15% year-over-year (YOY). Starlink remained the primary growth engine, producing $3.26 billion in quarterly revenue and reaching 10.3 million subscribers worldwide.

The real challenge is profitability.

SpaceX reported a net loss of $4.3 billion during the quarter after investing heavily in artificial intelligence infrastructure following its acquisition of xAI. The AI segment alone generated billions of dollars in operating losses, while capital expenditures reached $7.7 billion during the quarter.

Currently, Wall Street expects revenue to climb to about $38.2 billion in 2026 and nearly $69.2 billion in 2027, although earnings are still projected to remain negative as the company continues investing aggressively.

SpaceX Is Building Far Beyond Rockets

While Starship dominates the headlines, SpaceX is expanding across several high-growth businesses.

The company continues to grow Starlink, now serving more than 10 million subscribers globally, while investing in next-generation satellite technology. Also, it is developing additional Starship launch facilities in Florida to support a higher launch cadence later this decade.

Meanwhile, the company's AI ambitions continue to expand through xAI. SpaceX has secured long-term AI infrastructure agreements with companies including Anthropic and Alphabet's (GOOG) (GOOGL) Google, creating another potential multibillion-dollar revenue stream even as those investments weigh heavily on current earnings.

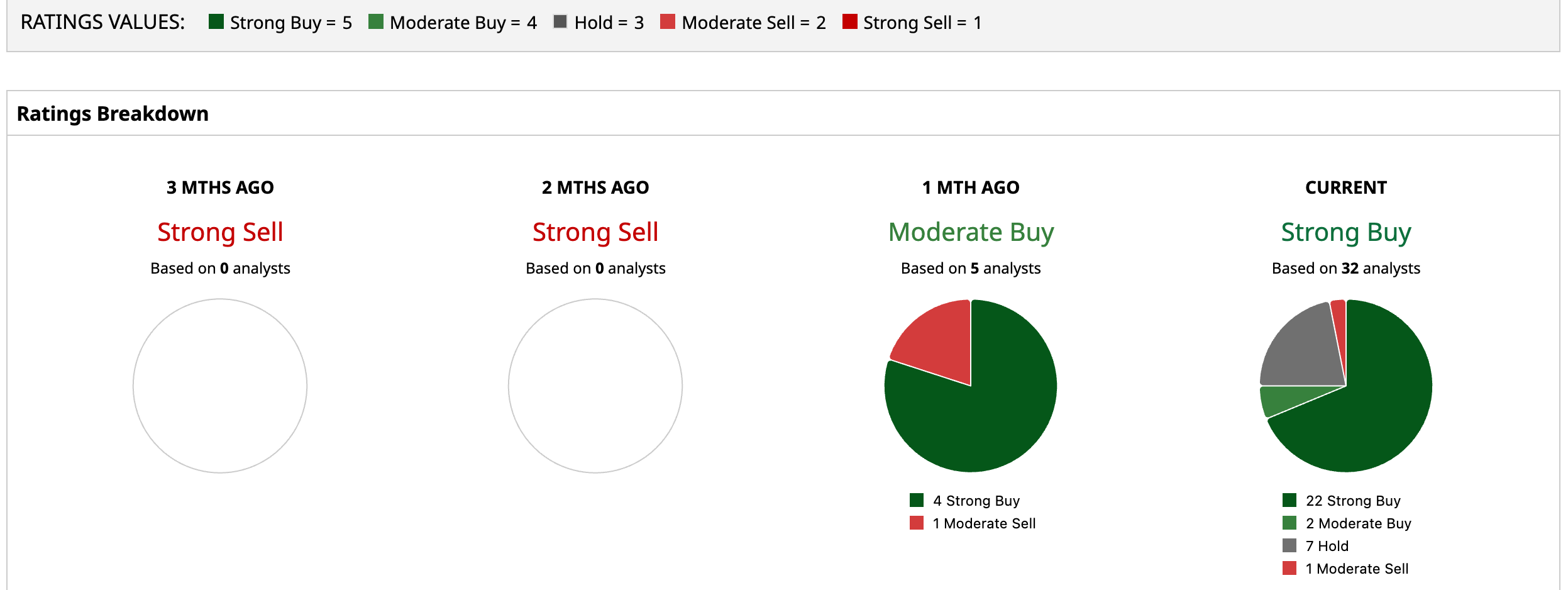

Wall Street Still Sees Significant Upside

Despite the recent sell-off, analysts remain overwhelmingly bullish on SpaceX shares.

Evercore ISI recently initiated coverage with an “Outperform” rating and a $230 price target, while Bank of America also started coverage with a “Buy” rating and a $235 target. Goldman Sachs sees the stock reaching $205, Morgan Stanley has one of the Street's highest targets at $300, and firms including Wells Fargo, Citigroup, and Canaccord Genuity maintain bullish outlooks.

According to a consensus of 32 analysts, the average price target sits at $232.82, implying substantial upside of 73.6% from current levels. Still, the wide gap between bullish Wall Street targets and much lower independent valuation estimates shows just how divided investors remain.

For now, all eyes are on July 16. Starship Flight 13 won't settle the long-term valuation debate, but it could become the next major catalyst that determines where SpaceX stock heads next.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)