Terawulf (WULF) stock suffered a significant decline on July 14 driven by the convergence of two major developments:

- The company’s ambitious plan to raise about $3.5 billion in debt to finance a new Kentucky data center campus

- New York Governor Kathy Hochul’s executive order imposing a one-year moratorium on state environmental permits for new hyperscale data centers

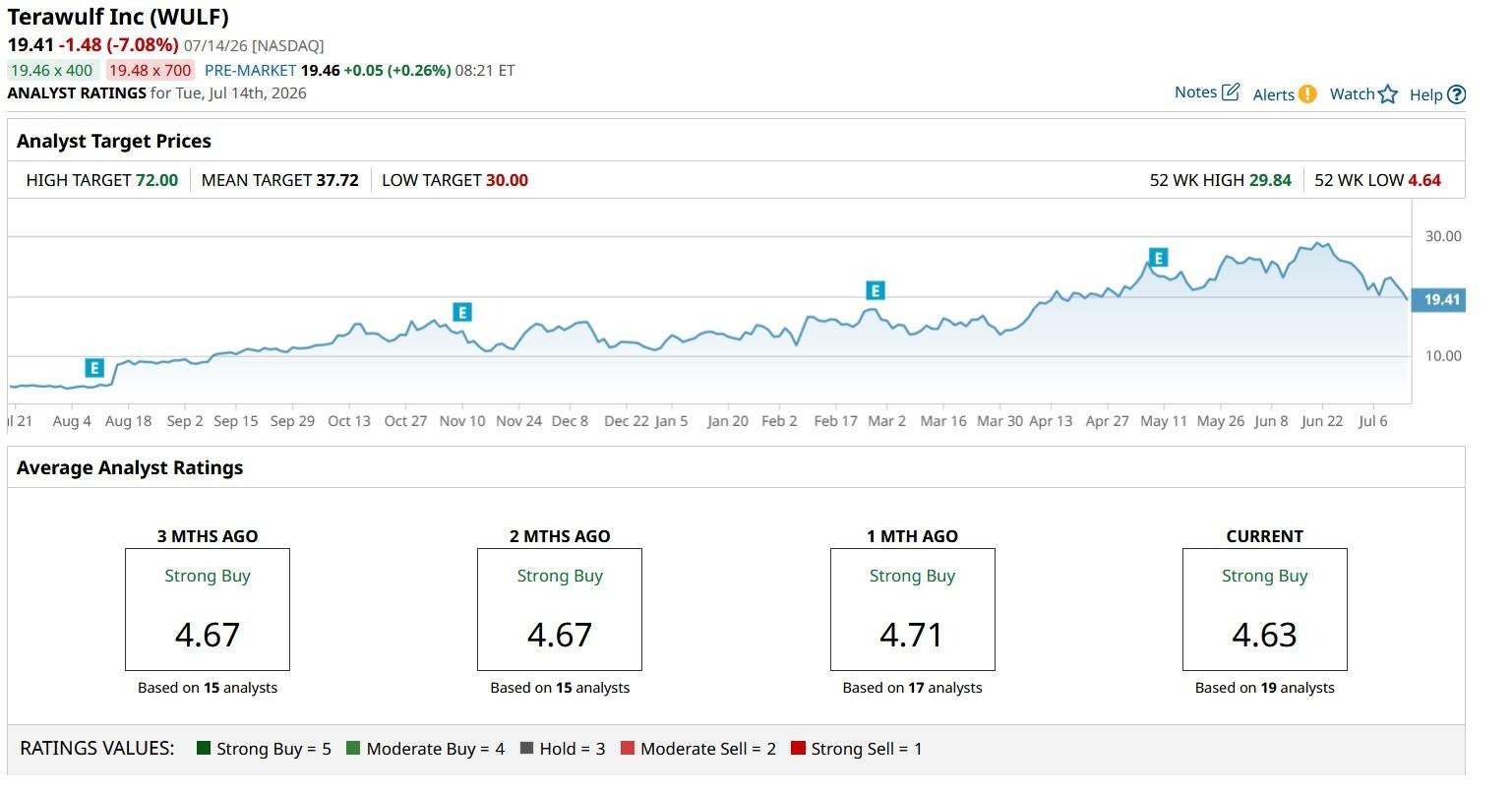

Terawulf shares closed at $19.41, reflecting “investor anxiety” over both the scale of the proposed leverage and the regulatory uncertainty suddenly injected into the firm’s operating environment. Today, it has rebounded slightly, up about 2% at the time of writing.

Significance of the Debt Raise for Terawulf Stock

The announced $3.5 billion debt raise will include Terawulf’s first leveraged loan as well as high-yield bonds, with Morgan Stanley expected to lead the financing.

Management has earmarked the proceeds for construction of Justified Data campus in Hawesville, Kentucky, which is anchored by a 20-year lease agreement with Anthropic covering approximately 401 megawatts of critical IT load.

Terawulf expects this lease to generate some $19 billion in contracted revenue over its initial term, representing a transformative shift in its business model from BTC mining to artificial intelligence infrastructure.

The sheer magnitude of the capital raise underscores the execution risk embedded in this pivot.

Building 400-plus megawatts of AI-ready data center capacity demands enormous upfront capital expenditure, and the financing costs and terms will materially affect equity returns.

Investors must weigh the promise of long-duration sales against the reality that contracted revenue is not collected revenue: cash flows depend on successful construction, energization, tenant ramp, and stable operations across a multi-year delivery timeline.

Significance of NY Moratorium for WULF Shares

New York’s moratorium adds a distinct layer of uncertainty. The executive order halts discretionary environmental permits for facilities roughly 50 megawatts and above while regulators prepare a Generic Environmental Impact Statement addressing electricity demand, water use, and air quality.

Terawulf operates its Lake Mariner campus in New York and is developing the Lake Hawkeye site in Lansing, creating direct exposure to this regulatory action even though the Kentucky project sits outside the state’s jurisdiction.

TeraWulf management moved quickly to reassure investors.

CEO Paul Prager stated that Lake Mariner is operational and that expansions supporting Fluidstack and Alphabet are fully permitted, positioning the moratorium as beneficial to firms with already-secured infrastructure.

Needham confirmed that Lake Mariner’s 600 IT megawatts of signed capacity appear unaffected, though the brokerage cautioned that the Cayuga (Lake Hawkeye) expansion could face uncertainty, a view Prager disputed.

The divergence between management’s optimism and the market’s reaction highlights a familiar tension: policy signals move faster than build schedules, and investors price ambiguity quickly.

Even if the Kentucky campus is the primary growth vector, the optionality to expand further in New York has become harder to model over the next 12 months.

The moratorium could also inspire similar actions in other states, potentially complicating multi-site development roadmaps industry-wide.

Other Headwinds Facing Terawulf

Terawulf’s financial transformation is already visible in its results. During Q1, high-performance computing lease revenue reached $21 million, exceeding digital asset mining revenue of just under $13 million for the first time.

Total quarterly revenue stood at $34 million. This crossover marks a structural shift in the firm’s revenue composition, validating the strategic pivot but also confirming its growing dependence on successful infrastructure delivery.

Additional market headwinds include the timing of an insider sale — erawulf's chief executive sold 137,500 shares on June 29 for about $3.66 million — and elevated short interest at some 25% of publicly available shares.

While insider sales have many legitimate motivations, the optics of selling into a week of rising headline risk amplified negative sentiment.

What’s the Consensus Rating on WULF?

The combination of heavy leverage, regulatory uncertainty, insider selling, and high short interest creates a volatile setup heading into the August 7 earnings report, where analysts expect Terawulf to report a per-share loss and revenue near $48 million.

Heading into the quarterly print, the consensus rating on WULF shares sits at “Strong Buy,” with the mean price target of roughly $38 indicating potential upside nearly 100% from here.

The fundamental question facing Terawulf investors is whether the market should value the firm primarily as a commodity-linked Bitcoin miner, where multiples remain tied to BTC cycles and energy spreads, or as an infrastructure landlord with multi-decade contracted cash flows.

The Anthropic lease and the $3.5 billion financing represent a decisive bet on the latter identity, but the transition requires flawless execution across interconnection queues, equipment procurement, construction sequencing, and tenant ramp — all against a backdrop of tightening state-level regulation and industry-wide competition for the same scarce resources.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)