IBM (IBM) stock suffered one of its worst single-day declines in years on July 14, with shares plunging 25.2% after the company released preliminary second-quarter results that missed Wall Street's expectations.

At first glance, the selloff may seem overdone. Revenue and earnings came in only modestly below expectations, and investors could see the sharp drop as a buying opportunity.

However, the market's reaction wasn't driven by the headline numbers alone. Investors were far more concerned about slowing growth in IBM's Software and Infrastructure businesses, which are its primary engines for AI-driven expansion.

Earnings Miss Across Key Metrics

IBM generated $17.2 billion in second-quarter revenue, up 1% year-over-year (YoY), while adjusted earnings per share rose 5% to $2.93. Both figures, however, fell short of analysts' expectations. The bigger disappointment came from the company's operating segments.

Software revenue increased 5%, a noticeable slowdown from the 8% growth reported in the first quarter. Infrastructure revenue declined 7%, with both businesses missing Wall Street's forecasts.

There was a bright spot within the Software business. Red Hat revenue climbed 11%, accelerating from the previous quarter. However, that strength wasn't enough to offset broader weakness across IBM's software portfolio.

The slowdown is particularly concerning because management has guided for more than 10% Software revenue growth for the full year. The Q2 miss raises concerns about whether IBM could achieve its growth targets.

Why Did IBM Miss Expectations?

IBM's weaker-than-expected quarter highlights a broader trend playing out across enterprise IT budgets.

CEO Arvind Krishna said one of the key reasons behind the disappointing results was an unexpected change in customer purchasing behavior.

Instead of moving ahead with planned investments, many enterprise clients redirected their budgets toward critical AI infrastructure, including servers, storage systems, and memory, as they rushed to secure supply-constrained hardware before anticipated price increases.

For IBM, the timing mattered. The company had anticipated some disruption from supply chain constraints, but it underestimated how aggressively customers’ IT budgets would shift toward AI infrastructure. That shift disrupted IBM's normal sales cycle, delaying deals that the company had expected to close during the quarter.

Moreover, the shortfall was not solely the result of external factors. IBM failed to quickly address changes in customer buying patterns. This led to several high-value transactions that were expected to close during the quarter slipping into future periods.

Should Investors Buy the Dip in IBM Stock?

IBM's recent share price weakness may look like an attractive buying opportunity, especially with the stock trading near its 52-week low. However, caution is warranted. While the latest weakness does not suggest any structural deterioration in IBM's business, it does reflect the broader trend of enterprise IT budgets being redirected toward AI, a shift from which IBM is not entirely insulated.

That said, IBM's long-term fundamentals remain intact. The company's diversified software portfolio, expanding generative AI offerings, and growing exposure to higher-growth markets provide a solid foundation for future growth. Demand for AI-driven data products should continue to support the Software business, while Red Hat remains a bright spot. Its growth has accelerated alongside the stabilization of consumption-based services revenue, strengthening its role as one of IBM's strongest growth engines. Further, strength in the IBM Z platform continues to support its mainframe business.

The biggest uncertainty is the pace of recovery in enterprise software spending. If AI-related investments continue to crowd out broader software budgets, IBM could struggle to meet its current growth targets, potentially prompting management to lower its full-year guidance for the Software business.

Until IBM shows that delayed software deals are converting into revenue, Software growth is reaccelerating, and management can consistently deliver on its financial guidance, investors shouldn’t rush to buy the stock.

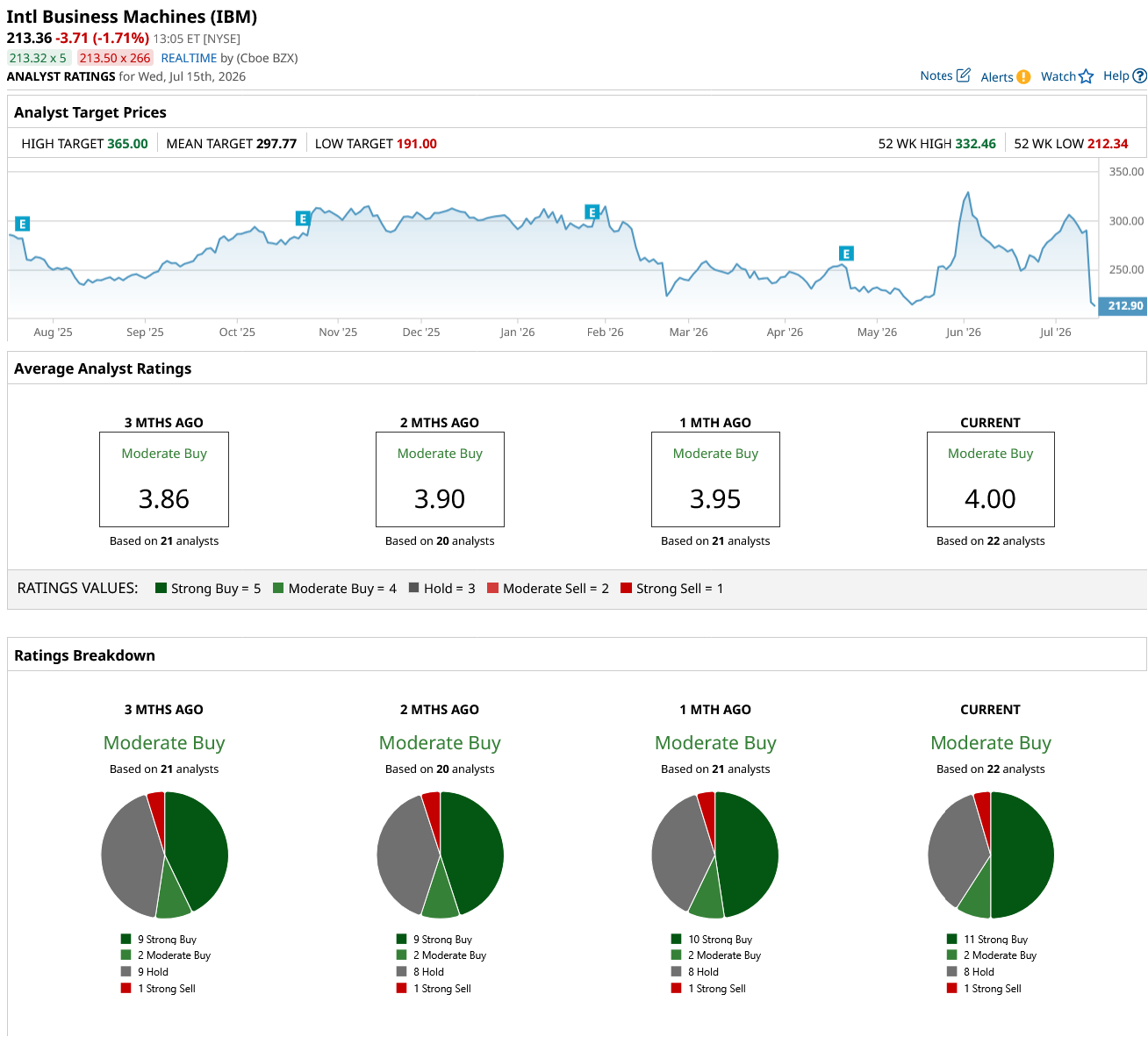

Wall Street analysts currently maintain a “Moderate Buy” consensus rating on IBM stock. However, with the company scheduled to report second-quarter earnings on July 22, a wait-and-see approach appears prudent. Management's commentary on software demand, enterprise spending trends, and the outlook for the mainframe business will provide important clues as to whether the recent pullback represents a buying opportunity.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.