/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

Alphabet (GOOG) (GOOGL) has spent years building its own AI chips just to power its own products. Now the company wants to rent and sell its custom chip capacity to other businesses.

That shift could unlock a new revenue stream while allowing the tech giant to gain traction in the AI race over the upcoming decade.

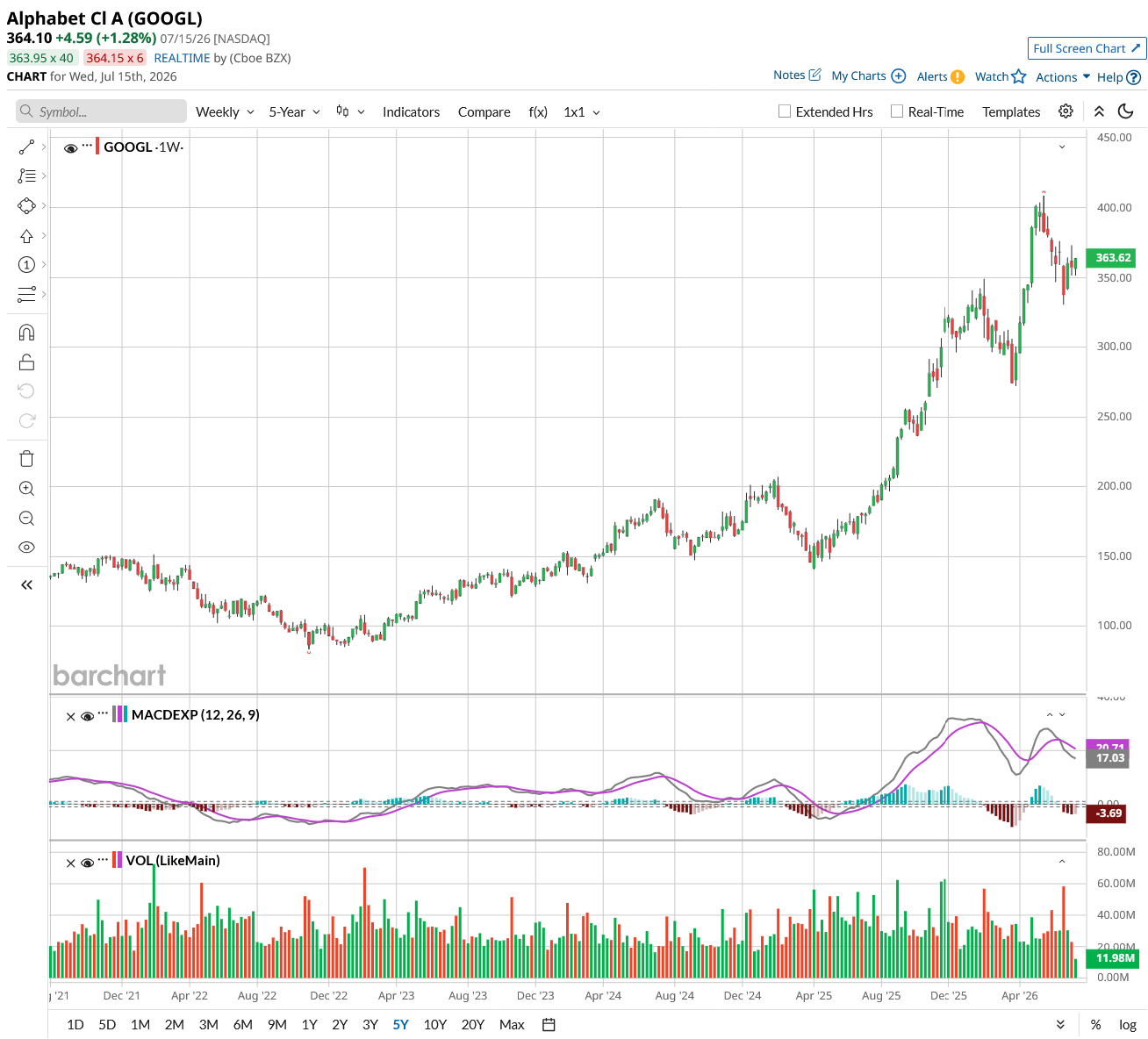

Alphabet’s Spending Is Already at Record Levels

Alphabet has been pouring money into AI infrastructure, and that spending continues to climb. CEO Sundar Pichai told investors on a June 3 special call that Alphabet spent about $31 billion on capital expenses in 2022.

This year, that number is expected to be between $180 billion and $190 billion, roughly six times 2022 levels and double what the company spent last year. Pichai also said 2027 spending will increase "significantly" compared to 2026.

Alphabet generated $174 billion in operating cash flow over the past 12 months and ended the first quarter with $127 billion in cash and marketable securities. The company also added roughly $20 billion in new debt since the quarter ended, pushing total debt above $100 billion.

That is the financial muscle behind Alphabet's hardware ambitions. And it explains why the company feels comfortable making a move that could reshape its cloud business.

Alphabet Wants to Sell Its AI Chips to Everyone Else

According to a Simply Wall St report:

- Alphabet is trying to turn its in-house AI chips, known as Tensor Processing Units (TPUs), into a business line that serves other companies.

- Alphabet built these chips to run its own AI models faster and cheaper.

- Now it wants to rent out that same chip power to other companies, including AI labs and financial firms, giving them an alternative to Nvidia's (NVDA) graphics processors.

- The move plugs Alphabet directly into a market currently dominated by Nvidia (NVDA) and AMD (AMD), with Intel (INTC) playing a smaller role.

- Alphabet's shift from using TPUs internally to renting them out could give Google Cloud a new identity as a seller of AI computing power rather than just a buyer.

- It opens a revenue stream tied to outside demand for AI workloads and, if the economics work out, could support profit margins across Google Cloud over time.

Pichai's comments support that direction too. He said on the call that Alphabet's eighth-generation TPUs, called 8i and 8t, use a new dual-chip design built specifically for the heavy training and inference needs of AI agents.

He also said Gemini serving costs dropped 78% in 2025, a sign that the chips are getting more efficient every year.

Why This Matters for Google Cloud and Investors

The chip business is a capital-intensive bet layered atop an already massive spending plan.

Google Cloud delivered a record $20 billion in revenue during the first quarter, with margins expanding to 33% and operating income more than tripling to $7 billion from a year earlier. Cloud's backlog nearly doubled from the previous quarter to $462 billion, driven largely by demand for enterprise AI tools.

Alphabet expects to recognize just over half of that backlog as revenue over the next 24 months. That is a long runway of committed spending from customers who are betting on Alphabet's AI roadmap, not just buying a service for one quarter.

Turning TPUs into a product for outside buyers adds risk too. Building chip clusters for other companies costs money upfront, and if demand does not materialize quickly enough, it could squeeze free cash flow.

Pushing into a market Nvidia has dominated for years is not simple either. Technical missteps or slow adoption could leave Alphabet with expensive hardware nobody wants to rent. If Alphabet can run more of its own workloads on TPUs rather than relying on GPUs from other companies, it could lower costs and boost margins for years to come.

What Next for GOOGL Stock?

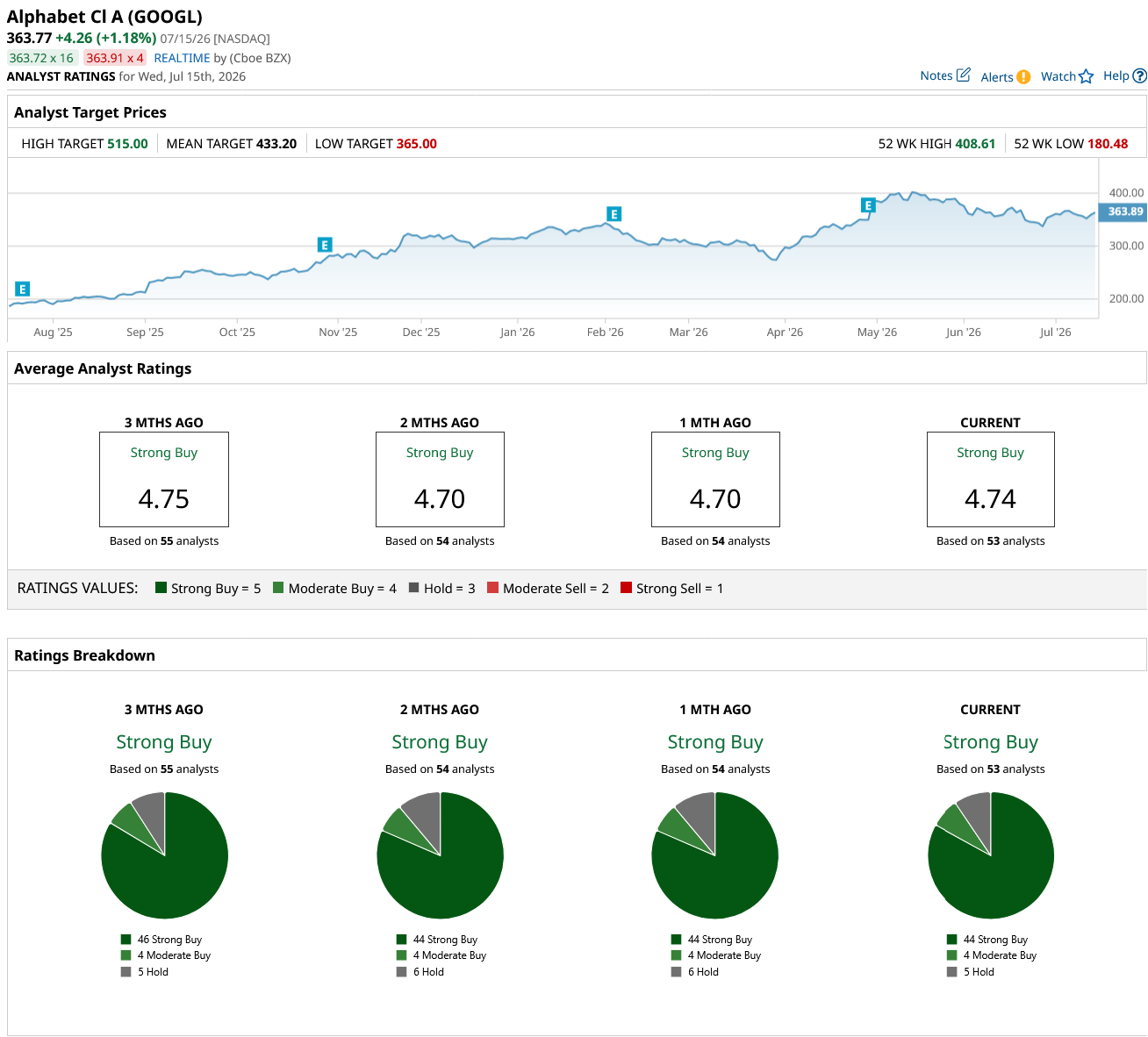

Analysts tracking GOOGL stock forecast revenue to increase from $402.84 billion in 2025 to $870 billion in 2030. In this period, adjusted earnings are projected to expand from $10.81 per share to $24.12 per share. If the stock is priced at 24x forward earnings, which is in line with its 10-year average, it could deliver over 60% returns over the next four years.

Of the 53 analysts covering GOOGL stock, 44 recommend “Strong Buy,” four recommend “Moderate Buy,” and five recommend “Hold.” The average GOOGL price target is $433.20, above the current price of $364.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)