/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

Intel Corporation (INTC) is making another bold bet on its manufacturing future. The chipmaker has announced a €5 billion ($5.7 billion) investment to significantly expand and upgrade its semiconductor manufacturing campus in Leixlip, Ireland, reinforcing its commitment to meeting surging demand for artificial intelligence (AI) and high-performance computing chips. The move not only strengthens Intel’s European production footprint but also signals management’s confidence in the company’s long-term turnaround strategy.

The investment will modernize existing fabrication facilities, install leading-edge manufacturing equipment, expand research and development capabilities, and increase production capacity for Intel’s advanced Intel 3 process technology, which powers current and next-generation Xeon processors. According to Intel, the project represents around 30% of its planned $17 billion capital expenditure for 2026, with most of the spending scheduled to be completed by the end of 2027.

Additionally, the announcement highlights Intel’s continued push to rebuild its manufacturing leadership and capitalize on the rapidly growing AI infrastructure market. As demand for AI servers and high-performance computing accelerates worldwide, expanding advanced chip production could position Intel to capture a larger share of this fast-growing opportunity while strengthening supply chain resilience.

About Intel Corporation Stock

Intel Corporation is a leading technology company specializing in the design, development, manufacture and marketing of semiconductor products, including microprocessors, chipsets, graphics processing units (GPUs), memory and related hardware for consumer, enterprise and industrial markets. Headquartered in Santa Clara, California, Intel remains a key player in data center, PC and emerging AI, and networking segments. Intel’s market cap is $518.3 billion, reflecting its valuation among the world’s largest semiconductor companies.

Intel has been one of the market’s strongest-performing semiconductor stocks in 2026 despite a recent pullback. The shares have delivered solid triple-digit gains of 193.2% year-to-date (YTD) and have surged 364.3% over the past 52 weeks, fueled by renewed optimism surrounding the company’s AI foundry ambitions, manufacturing turnaround, and major customer wins.

However, after hitting a fresh 52-week high of $142.35 on June 30, the stock has entered a period of heightened volatility and has retreated 24.3% from the peak. Plus, on July 13, Intel shares fell as much as 6.12% intraday, joining a broad semiconductor selloff triggered by geopolitical tensions in the Middle East and profit-taking across AI-related stocks.

Nevertheless, even with the recent weakness, Intel remains one of the top-performing large-cap chip stocks in 2026, underscoring investors’ continued confidence in its long-term turnaround story.

The stock is currently trading at a premium to its sector median at 171.94 times forward price-to-earnings.

Better-than-Expected Q1 Performance

Intel’s first-quarter 2026 earnings were released on April 23. The company reported revenue of $13.58 billion, up 7% year-over-year (YOY), while non-GAAP earnings per share (EPS) reached $0.29 versus $0.13 in the prior-year period, representing a 123% YOY increase and exceeding expectations. On a non-GAAP basis, net income rose to $1.5 billion, up 156% YOY.

The most important feature of the quarter was the acceleration in Intel’s data center and AI business, which is increasingly defined by CPU demand tied to AI workloads. Segment revenue reached $5.1 billion, up 22% YOY, materially outpacing the rest of the portfolio and well ahead of expectations. This growth was driven primarily by server CPUs, particularly Xeon processors, as hyperscalers and enterprises scale infrastructure for inference and emerging agentic AI systems. Management explicitly framed CPUs as the “essential role” in the AI era, reflecting a shift from GPU-centric training workloads toward CPU-heavy orchestration, inference, and real-time processing.

This CPU-led demand is not merely cyclical but structural. Industry data indicates that AI server architectures are evolving toward significantly higher CPU-to-GPU ratios, which is materially increasing unit demand and pricing power for server-grade processors. As a result, Intel is actively prioritizing production capacity toward data center CPUs, underscoring the centrality of this segment to near-term growth.

Outside of the data center, performance was more mixed but still constructive. The Client Computing Group generated $7.7 billion in revenue, up about 1% YOY, while the foundry business experienced around 16% growth.

Furthermore, Intel’s guidance reinforced the improving trajectory. For Q2 2026, the company expects revenue of $13.8 billion to $14.8 billion and non-GAAP EPS of $0.20.

In addition, analysts predict EPS to be $0.64 for fiscal 2026, an improvement of 633.3% YOY, before surging by 54.7% annually to an EPS of $0.99 in fiscal 2027. Moreover, its EPS is expected to rise 138.5% in the upcoming reported quarter (Q2) to $0.10. The company is set to report its Q2 2026 financial results on Thursday, July 23, after the close of the market.

What Do Analysts Expect for Intel Stock?

Most recently, KeyBanc raised its price target on Intel to $155 from $110 while reiterating an “Overweight” rating, citing robust demand for server CPUs fueled by agentic AI.

Also, Stifel raised its price target on Intel to $120 from $75 but maintained a “Hold” rating, while citing continued progress in the company’s multiyear turnaround.

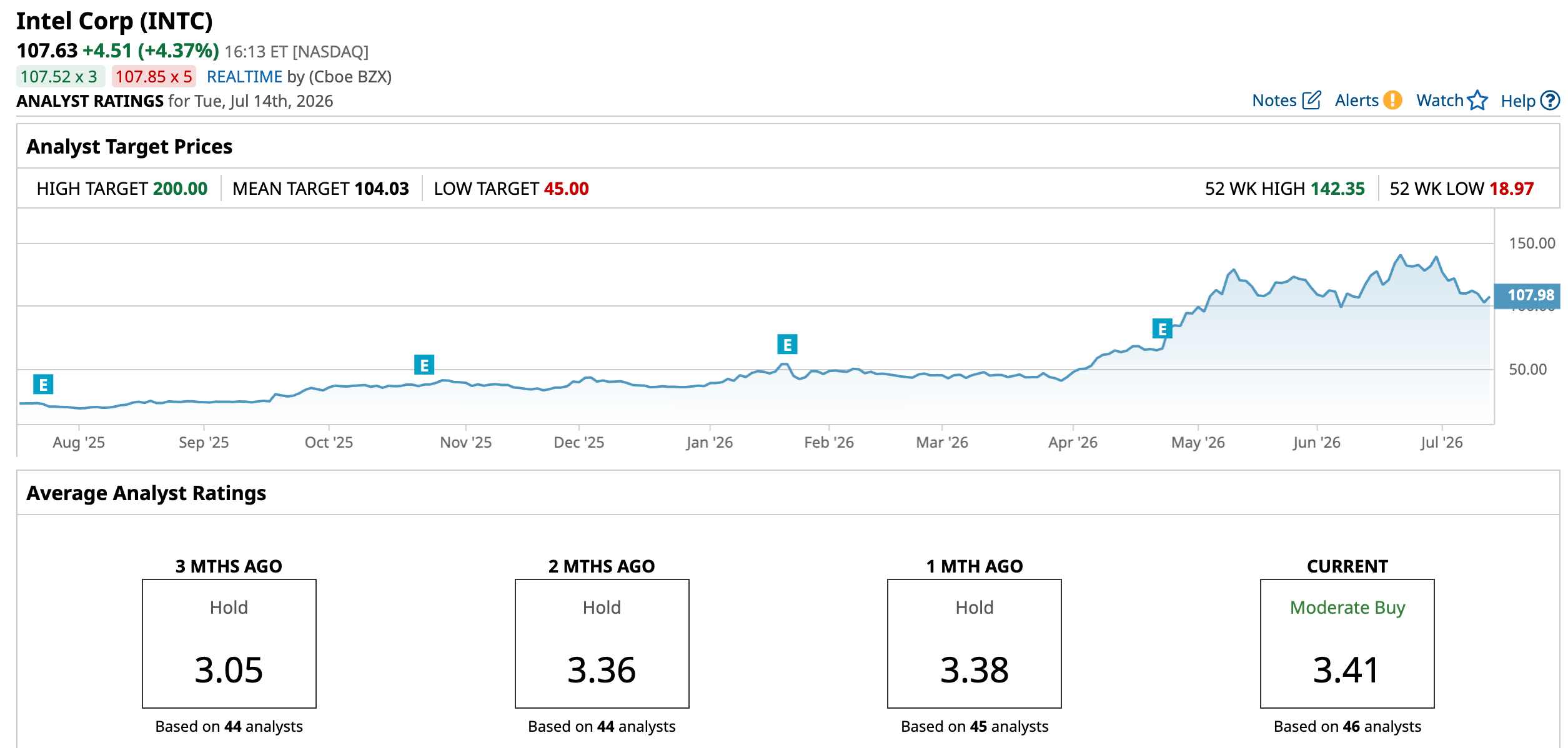

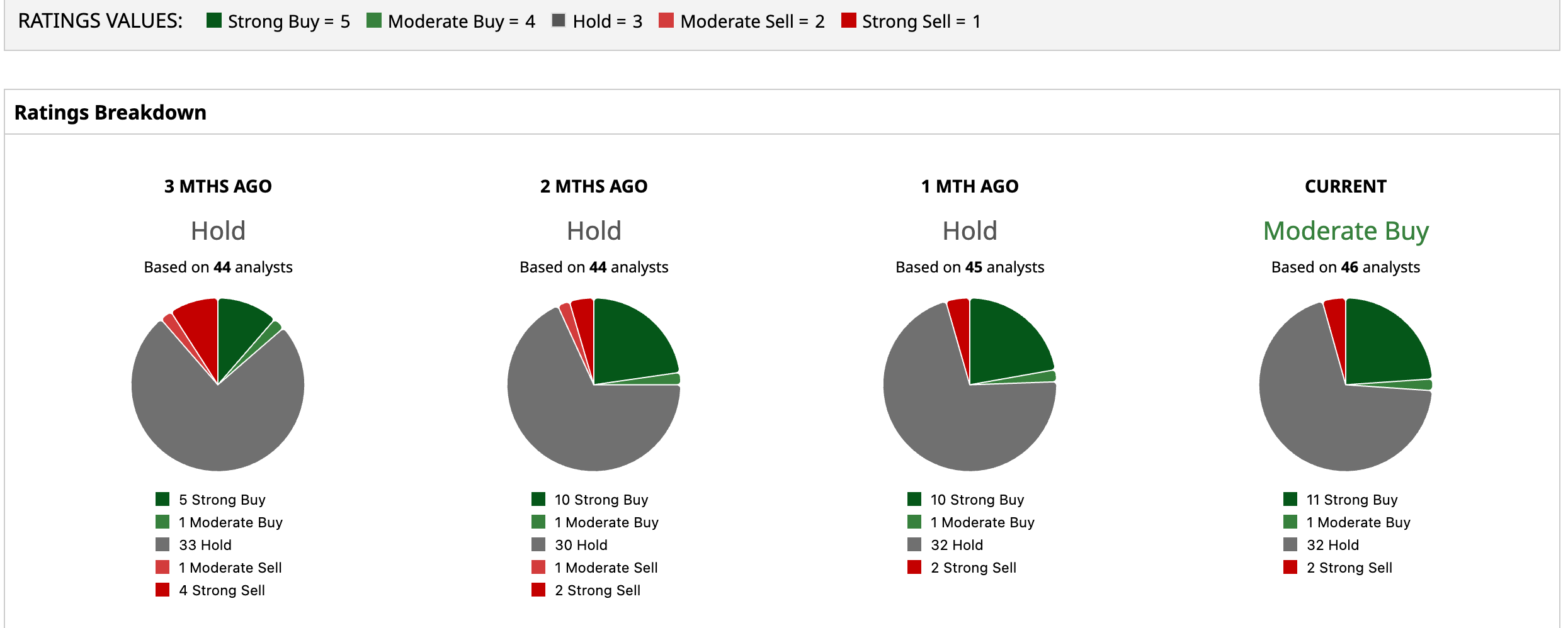

INTC has a consensus “Moderate Buy” rating overall. Of the 46 analysts covering the stock, 11 advise a “Strong Buy,” one recommends a “Moderate Buy,” 32 analysts are on the sidelines, giving it a “Hold” rating, and two suggest a “Strong Sell.”

INTC has surged past the average analyst price target of $104.03, while the Street-high target price of $200 suggests that the stock could rally 85.8%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)