Goldman Sachs upgraded Nio (NIO) from “Neutral” to “Buy” on July 13, setting a $7 price target for the U.S.-listed shares, implying about 42% upside from the current share price of $4.93.

The upgrade was triggered directly by NIO’s strong June and second-quarter 2026 delivery results, with the firm reporting 40,597 vehicles delivered in June and 107,658 for the full quarter, bringing cumulative deliveries to about 1.19 million vehicles.

At the time of writing, NIO stock is hovering roughly around the same price at which it started the year 2026.

Why Goldman Sachs Upgraded Nio Stock

In its research note, Goldman Sachs cited what it called a “successful turnaround” driven primarily by the ES8 and ES9 premium SUV models, which have reinforced NIO’s leading brand power in China’s premium new-energy vehicle market.

The investment firm expects Nio to deliver “one of the fastest volume growth rates” across its coverage universe, projecting 43% vehicle volume growth and 60% revenue growth in 2026, vastly outpacing about 1% growth expected in China’s broader domestic auto market.

Goldman also forecasts a premium margin profile and anticipates that the EV maker will swing to a non-GAAP net profit of 1.6 billion yuan (approximately $236 million) from a 12.4-billion-yuan loss in 2025.

Fundamentals Warrant Buying NIO Shares

The financial transformation underlying the upgrade is substantial.

Nio's gross margin nearly tripled to 19% year-over-year in Q1, vehicle margin reached 18.8% with four consecutive quarters of improvement, R&D expenses fell over 40%, and SG&A declined more than 20%.

The EV company achieved a brief GAAP net profit of 282.7 million yuan in Q4 before slipping to a minimal loss of 48.1 million yuan in Q, with CEO William Li targeting positive non-GAAP operating profit for full-year 2026.

Free cash flow is projected by Goldman Sachs to improve dramatically to 12.1 billion yuan from an outflow of 3.1 billion yuan.

Goldman’s trajectory with NIO has been notable, having placed the EV stock on its “Sell” list in late 2024 before moving it to “Neutral” in June 2025 as the cost structure improved, and now upgrading to Buy as delivery acceleration validates the turnaround thesis.

The bank believes NIO has demonstrated a consistent capability to launch competitive models and could apply the same successful strategy to its 5-series and 6-series vehicles, supporting continued market-share gains.

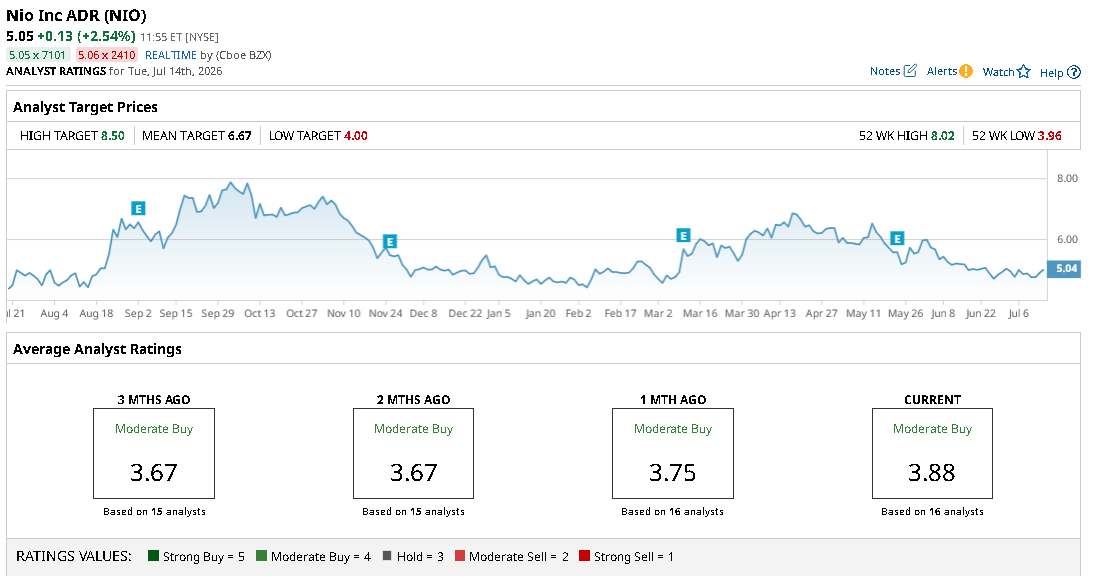

What’s the Consensus Rating on Nio?

Investors should also note that other Wall Street analysts agree with Goldman Sachs’ positive view on NIO shares.

The consensus rating on the EV maker also currently sits at “Moderate Buy,” with the mean price target of about $6.67 indicating potential upside of more than 30% from here.

However, risks remain significant despite the bullish thesis. NIO is still down 89% over five years, shareholders’ equity stands at a thin $626 million, European expansion through the Firefly sub-brand faces headwinds from tariffs and weak demand, and the intensely competitive Chinese EV market with ongoing price wars could cap margins even as volumes grow.

The key question for investors is whether NIO can sustain the conversion of rapid delivery growth into durable profitability in an environment where excess EV capacity continues to pressure the entire sector.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)