/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

The streaming wars have moved beyond content to include advertising, live sports, amusement parks, and intellectual property (IP). While both Netflix (NFLX) and Disney (DIS) dominate the global entertainment industry, both offer two very different investment stories. Between Netflix’s focused streaming dominance and Disney's diversified media empire with multiple growth engines, let’s take a closer look at which is the better entertainment stock for investors today.

The Case for Netflix: Winning the Streaming Game

Netflix has spent the last few years cementing its position as an online streaming giant with its unmatched global scale. With more than 300 million paid memberships serving a huge audience worldwide, the platform enjoys an outstanding international footprint.

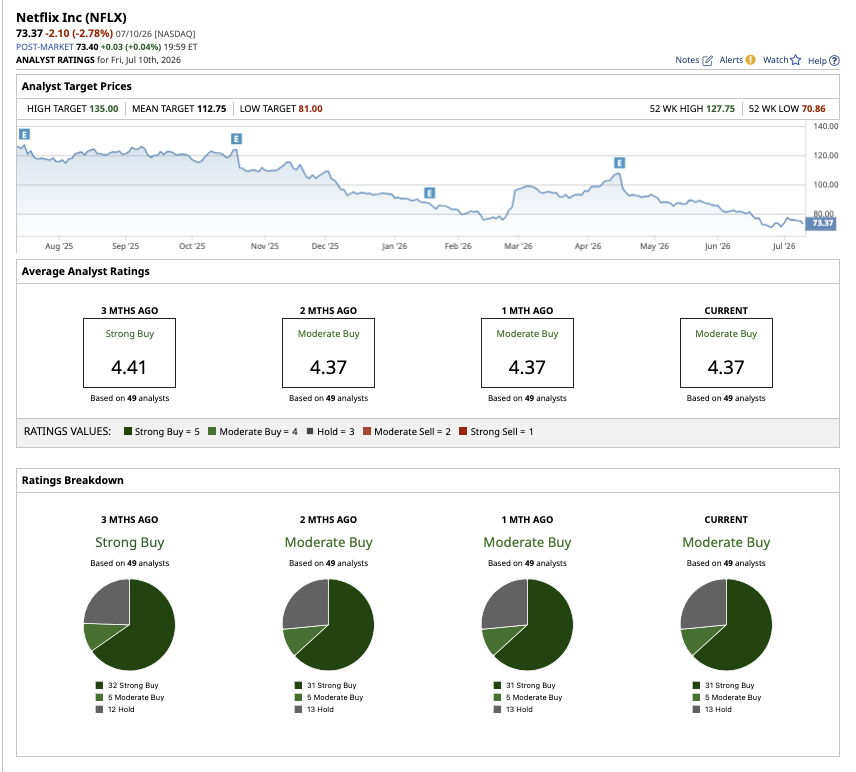

In the first quarter of fiscal 2026, Netflix’s revenue grew 16% year-over-year (YOY) to $12.2 billion, led by membership growth, increased pricing, and advertising revenue. Diluted earnings grew 86% YOY to $1.23 per share. Despite its massive scale, management believes the company has captured less than 45% of the addressable household market, or only about 7% of its estimated $670 billion addressable revenue opportunity. Furthermore, the company believes that by accounting for just 5% of global TV viewing share, it still has substantial room for expansion.

To capitalize on this opportunity, Netflix is now expanding its core entertainment offerings through original series, films, licensed programming, podcasts, regional live sports, and gaming. It is also strengthening monetization through a rapidly growing advertising business. The company even expects its advertising business to nearly double in fiscal 2026 to around $3 billion in revenue.

Pricing power remains Netflix’s competitive advantage. Despite an increase in subscription price last year, the company saw industry-leading retention and growing member value in the United States. Netflix is scheduled to report its Q2 2026 results on July 16. The company expects 13% revenue growth in Q2, slightly lower than the consensus estimate of 14% with earnings projections of $0.79 per share.

For fiscal 2026, analysts expect Netflix to report a 42% increase in earnings to $3.60 per share, followed by a 7% increase to $3.85 per share in fiscal 2027. At 20 times forward earnings, Netflix is valued at a premium, with investors expecting higher growth as it continues to extend its leadership in global entertainment

Overall, Wall Street gives NFLX stock a consensus “Moderate Buy” rating. Of the 49 analysts covering the stock, 31 recommend a "Strong Buy," five rate it as a "Moderate Buy," and 13 suggest a “Hold.” Although Netflix stock is down 21% year-to-date (YTD), Wall Street anticipates potential upside of around 53% over the next 12 months based on the average price target of $112.75. The high price estimate of $135 suggests potential upside of 83% from current levels.

The Case for Disney: Multiple Growth Engines Beyond Streaming

Disney is a global entertainment company that creates, owns, and distributes movies, television shows, sports programming, and streaming content. It is also renowned for its theme parks, resorts, cruise lines, and consumer products based on its iconic franchises such as Marvel, Star Wars, Pixar, and Disney Animation. Disney is now focused on building a more connected entertainment ecosystem.

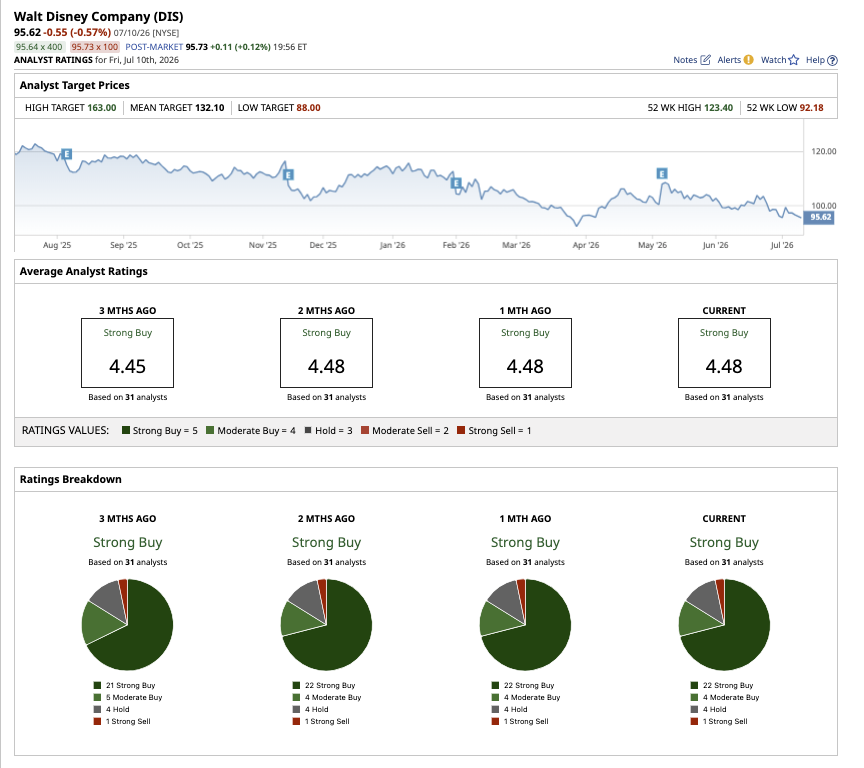

In Q2 2026, revenue grew by 7% YOY to $25.2 billion, while adjusted earnings increased 8% YOY to $1.57 per share. Both higher pricing and subscriber growth led to an 11% sequential revenue increase for the Entertainment Subscription Video on Demand (SVOD) segment.

Disney's greatest competitive advantage remains its unmatched library of IP. The company holds decades of beloved franchises that can be monetized repeatedly through sequels, television series, merchandise, attractions, and licensing deals. For example, according to the company, Zootopia 2 has now crossed 1 billion streamed hours on Disney+. Additionally, its recent and upcoming releases — including The Mandalorian and Grogu, Toy Story 5, the live-action Moana, and Avengers: Doomsday — are expected to create long-term value across films, streaming, consumer products, and experiences. The company is strengthening its streaming platforms through product and technology innovation, expanding ESPN's direct-to-consumer business, and accelerating growth across Disney Experiences.

While this diversification is a plus, it also makes Disney’s business more complex. For instance, movie performances can fluctuate while theme parks are sensitive to economic slowdowns and consumer spending trends. Analysts expect Disney’s earnings to increase by 16% in fiscal 2026, followed by 9% growth in fiscal 2027. Trading at nearly 14 times forward earnings, DIS stock is valued cheaper than NFLX stock right now.

On Wall Street, DIS stock holds a consensus “Strong Buy” rating. Of the 32 analysts who cover shares, 23 recommend a "Strong Buy," four analysts suggest a "Moderate Buy," four rate the stock as a “Hold,” and one has a “Strong Sell" rating. Analysts have a mean price target of $131.53, which suggests potential upside of 36% from here, even though DIS stock is down 15% YTD. The high target price of $163 indicates potential upside of 69% over the next 12 months.

Which Stock Is the Better Buy Now?

Both of these companies are leaders in entertainment, but one has the better investment story.

Netflix has a simple business model with one dominant global platform focused primarily on subscriber engagement, pricing power, and profitability. It is showing strong revenue growth, expanding operating margins, a rapidly scaling advertising business, growing engagement, and new initiatives spanning live events, gaming, podcasts, and AI. Its premium valuation also suggests investors expect stronger earnings growth.

Disney, on the other hand, offers greater diversification and arguably more turnaround potential. The company generates revenue from multiple businesses beyond streaming. But this diversification creates both opportunity and uncertainty as investors have to track how each business continues to perform.

For investors prioritizing steady earnings growth, operational execution, and expanding profitability, Netflix stock appears to be the stronger buy today.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.